Assets listed on the balance sheet of an enterprise and used in production processes have a limited service life. Every year the functional condition gradually deteriorates, which is caused by natural depreciation. In addition, there is the concept of “obsolescence” - when inventory items are still suitable for use, but the feasibility of their use is reduced due to the emergence of alternative solutions with greater efficiency. Thus, for any organization, sooner or later there comes a time when it is necessary to issue an act of write-off of a fixed asset item. What grounds and orders are required for this, who determines the need for the procedure, and how exactly is it implemented from the point of view of document flow rules? Let's figure it out.

General overview

First, some basic terminology. The category under consideration includes inventory items that are on the company’s balance sheet and are involved in production and management processes for at least one year. Given the broadness of the formulation, not only complex technical equipment - machines and devices, but also transport, various types of mechanisms and devices, inventory, materials, buildings and premises, and even plantings and roads located on the territory owned by the organization can be defined in this capacity . The specifics influence the determination of its current state, therefore, before proceeding with the execution of the act of disposal of fixed assets and documentation in general, it is necessary to study in detail the features of the object in question.

Reasons for write-off

From an accounting point of view, the procedure for removing assets from the balance sheet of an enterprise seems to be very complex, since it requires the implementation of a number of standard activities. It is problematic to unify the process, at least due to the diversity of forms and types of property that formally belong to one category. The algorithm, defined by the provisions of clause 29 of PBU 6/01, as well as the content of methodological instructions published within the framework of the Decree of the Ministry of Finance of the Russian Federation No. 91n of 2003, provides for the following mandatory stages:

- Formation of a commission or working group that assesses the condition of inventory items and makes a decision on the advisability of restoration or refusal of further operation.

- Drawing up an act for write-off of fixed assets according to the OS 4 form.

- Reflection of the operation in the accounting program, in compliance with the transactions and data registration rules.

Physical wear and tear, like obsolescence, is a natural process caused by the regular use of goods and materials, as well as the development of technology. In most cases, expensive objects are subject to restoration, allowing them to preserve key functional properties. If investments in renovation turn out to be unjustified, a situation arises in which a more profitable solution from an economic point of view is refusal from further use.

Some operating systems are multi-component mechanisms, with different wear rates of individual components. Examples include motor vehicles, non-residential premises with several buildings, or large production lines. In this case, it is not necessary to abandon the entire object - it is enough to replace an obsolete part, or organize local repairs, that is, carry out partial liquidation.

Reasons sufficient for making a decision to withdraw from the balance sheet include:

- Inappropriateness of operation due to depreciation or obsolescence.

- Critical changes associated with an emergency or emergency situation.

- Identification of shortages during inventory, including as a result of theft.

- Unusable condition caused by intentional or accidental damage to property.

- Carrying out reconstruction, which involves removing part of the object.

The specified list is also regulated by regulations enshrined within the framework of methodological recommendations and accounting rules. An example of filling out an act of write-off of fixed assets can be freely downloaded from the Internet, however, before starting the procedure, it is necessary to study the key points, eliminating the possibility of registration and posting errors.

Order form

An order to write off property is considered a form indicating the need to carry out certain measures, in this case the write-off of fixed assets.

The order is formed in written free form, according to the rules established in office work, since there is no template approved by the legislation of the Russian Federation.

At the same time, when drawing up such an order, the following must be observed:

- The form is issued in one copy, with registration in the order book.

- The order must indicate the period of its validity. In the absence of such a clause, the order is valid for one year.

- To form an order in the state. The institution requires preliminary approval for write-off from higher federal departments, for which they are sent a commission act with a list of fixed assets to be written off.

- Employees who are related to the work of the commission and are noted on the form must be familiar with the order.

- The order must be endorsed by the director.

- It is not necessary to affix the director’s signature with a seal, since the document is internal to the department.

- During the period of validity of the administrative document, it is kept by the secretary or by the official responsible for this area, with subsequent transfer to the archive for preservation, in accordance with the legislative norms of the Russian Federation.

What are the main assets?

According to the general classification in the legislation of the Russian Federation, operating systems include:

- Buildings and constructions.

- Residential Properties.

- Equipment, tools and other equipment.

- Measuring equipment.

- Transport.

- Computer and office equipment.

- Productive and working animals.

- Perennial plants.

- Earth.

Note : OS also includes capital investments in the modernization of facilities.

Reasons for drawing up

The write-off of property, as a rule, is carried out after summing up the activities of the inventory commission appointed by the director of the company.

The basis for publishing an order to write off an asset may be:

- The property is unsuitable for continued use.

- Sales to third parties.

- Transfer free of charge.

- Leasing.

- Crediting to the authorized capital of another company.

Before filling out the form for the order to write off the OS, the appointed commission must meet to inspect the object and make a final conclusion indicating the unsuitability of the OS or the inappropriateness of their use.

Therefore, the basis for an order to write off an asset is usually an act signed by all members of the commission, with a detailed display of the condition of the property and data from technical documentation.

The procedure for writing off fixed assets is regulated by clauses 75–86 of the Methodological Regulations on Accounting for fixed assets, approved by the Ministry of Finance of the Russian Federation No. 91n dated October 13, 2003.

The OS write-off algorithm is:

- Analysis of the technical condition of the OS.

- Preparation of the necessary documentation.

- Publication of an order to liquidate the facility.

- Dismantling of property.

- Disposal or sale of property.

- Write-off of fixed assets from the balance sheet and accounting of the enterprise.

Ready-made solutions for all areas

Stores

Mobility, accuracy and speed of counting goods on the sales floor and in the warehouse will allow you not to lose days of sales during inventory and when receiving goods.

To learn more

Warehouses

Speed up your warehouse employees' work with mobile automation. Eliminate errors in receiving, shipping, inventory and movement of goods forever.

To learn more

Marking

Mandatory labeling of goods is an opportunity for each organization to 100% exclude the acceptance of counterfeit goods into its warehouse and track the supply chain from the manufacturer.

To learn more

E-commerce

Speed, accuracy of acceptance and shipment of goods in the warehouse is the cornerstone in the E-commerce business. Start using modern, more efficient mobile tools.

To learn more

Institutions

Increase the accuracy of accounting for the organization’s property, the level of control over the safety and movement of each item. Mobile accounting will reduce the likelihood of theft and natural losses.

To learn more

Production

Increase the efficiency of your manufacturing enterprise by introducing mobile automation for inventory accounting.

To learn more

RFID

The first ready-made solution in Russia for tracking goods using RFID tags at each stage of the supply chain.

To learn more

EGAIS

Eliminate errors in comparing and reading excise duty stamps for alcoholic beverages using mobile accounting tools.

To learn more

Certification for partners

Obtaining certified Cleverence partner status will allow your company to reach a new level of problem solving at your clients’ enterprises.

To learn more

Inventory

Use modern mobile tools to carry out product inventory. Increase the speed and accuracy of your business process.

To learn more

Mobile automation

Use modern mobile tools to account for goods and fixed assets in your enterprise. Completely abandon accounting “on paper”.

Learn more Show all automation solutions

Order of conduct

In order to remove unusable assets from an organization’s balance sheet, it will first be necessary to determine whether their further exploitation has no real basis. This task is assigned to a special commission, approved in a special manner, which is tasked with confirming the presence of facts of wear, defects, or the absence of material assets due to shortages.

The verdict of a malfunction is the basis for drawing up an act for writing off the OS, a sample of which we will consider later. This document, properly executed, allows you to draw up an order, which contains an order from the management of the enterprise to remove assets from the general balance sheet. After this, the results of joint work are transferred to the accounting department, which carries out the procedure for reducing the value of fixed assets, and the object itself is disposed of, given away on a voluntary basis, or sold on the secondary market - if there is appropriate demand.

When can you do without a write-off order?

To a certain extent, the need to issue an order to write off fixed assets is determined by the way the business entity operates, the peculiarities of its document flow and the way in which the enterprise gets rid of equipment that has become unusable.

That is, the type of order in question is not mandatory and its issuance, in fact, expresses management’s consent to write-off to a greater extent than an order to write-off.

Moreover, write-offs may occur on other grounds. The fact is that fixed assets, even if they have fallen into disrepair, are, in most cases, still some kind of material value that can be alienated or exchanged, for example, as scrap metal or components, or transferred under a disposal agreement.

The basis for writing off alienated or disposed of fixed assets, as well as the basis for drawing up primary documentation, will therefore not be an order, but a corresponding agreement.

Whose responsibilities include filling out the act?

Before starting the partial or complete liquidation procedure, it is necessary to determine the composition of the commission responsible for assessing the state of the OS.

In accordance with the regulations, the working group must consist of three or more people, which must include an employee of the enterprise who is the financially responsible person, as well as the organization’s accountant. The final list is determined by order of the manager. It is also possible to involve third-party specialists who have expert knowledge in the required area and have sufficient qualifications to certify the criticality of the identified failure. This practice is relevant when solving issues related to complex technical equipment.

Making a final decision on writing off fixed assets according to the form is possible only after the authorized commission has implemented all the planned activities. These include:

- Conducting a visual inspection (except for cases where the reason for removal from the balance sheet is the identified shortage or theft of inventory items).

- Assessment of the functional state, potential and feasibility of restoring the facility, as well as the economic aspects of further operation.

- Establishing the root cause of deterioration - depreciation, obsolescence, intentional or accidental damage.

- Identification of persons responsible for premature loss of performance characteristics - in situations where the standard service life has not yet expired.

- Determining the possibility of partial use of individual components, elements or materials, as well as the prospects for their implementation in order to generate income and compensate for losses of the enterprise.

The results of the overall assessment are recorded in the commission’s conclusion. The absence of a standard form allows you to choose a template yourself, subject to entering the mandatory details of the primary documentation and approval by order of the manager within the framework of the organization’s accounting policy. Responsibility for filling out lies with a full-time employee, usually representing the accounting department.

How to draw up an act correctly

Completion of the first stage, in which the newly created working group is involved, allows us to move on to the next stage. The document flow regulations allow the use of various types of forms for writing off fixed assets, the choice between which is determined by the specifics of a particular situation. Current forms include:

- OS-4 is a standard template used when deregistering one object, with the exception of situations when it comes to road transport.

- OS-4a is a modification developed specifically for the above exceptions.

- OS-4b is a type of standard document filled out when disposing of several inventory items at once.

The regulation approving the procedure for preparing these forms is Goskomstat Resolution No. 7, published in 2003.

The generated documentation confirming the decision to write off implies the need to promptly reflect the operation in inventory books and cards, as well as accounting programs used to control the storage and movement of fixed assets. This recommendation is mentioned in paragraph 80 of the Methodological Instructions of the Ministry of Finance, which determines the significance of the procedure. As a rule, when maintaining document flow, standard documents are filled out in the following format:

- Inventory cards No. OS-6 for separate accounting of inventory and property assets.

- Forms corresponding to sample No. OS-6a are relevant in cases where assets belong to group categories.

- Inventory books of small enterprises - No. OS-6b.

The specified accounting documentation is also regulated by the already mentioned resolution of the State Statistics Committee.

Preparation for write-off

As a rule, the issuance of an order to write off fixed assets is associated with the write-off of a material object due to its wear and tear, be it moral or physical wear.

The beginning of the write-off procedure is the preparation of the appropriate act or defective statement for write-off. By drawing up these documents, a kind of recommendation is given on how to decide the future fate of worn-out fixed assets.

An act or defective statement is drawn up by a specially created commission of at least three participants who have the knowledge that allows them to assess both the technical and functional condition of fixed assets. If necessary, employees or experts specializing in specific types of equipment may be involved in the work of the commission.

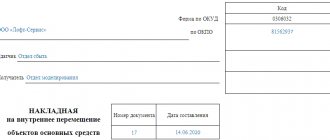

Example of filling out OS 4 form for write-off

The procedure for completing the standard form provides for sequential entry of data, eliminating possible errors and discrepancies with basic recommendations. On the front side of the document, at the top, the following information is indicated:

- name of the enterprise;

- TIN and checkpoint;

- structural subdivision.

The last point is determined by the need to clarify the department or branch on whose balance sheet the fixed asset to be withdrawn is listed.

Next, information is entered on the grounds that served as a factor for making the decision on partial or complete liquidation. As a rule, a link is provided to one of the related acts or orders of the management team, supplemented by the data of the full-time employee who is financially responsible for the goods and materials in question (only the last name, first name and patronymic are indicated).

On the right side of the standard form, fill out the following sections:

- Code according to the All-Russian Classifier of Enterprises and Organizations.

- The date of drawing up the act on writing off the asset from accounting.

- Details of the document that served as the basis for the implementation of the procedure.

- Personnel number of the employee assigned to be responsible for the property.

Below is information about the serial numeric code assigned to the form, the actual reasons for the disposal of the fixed asset, as well as standard details. A separate free space is allocated for the approval and signature of the head of the organization.

After this, you need to move on to the next tabular part of the form, the content of which is directly related to the material assets to be written off. The procedure for specifying information looks like this.

| Column no. | Content |

| 1 | Nomenclature name of the object |

| 2-3 | Inventory and factory registration number, respectively |

| 4-5 | Dates of actual issue and crediting to the balance sheet of the enterprise |

| 6 | The actual duration of operation, that is, all periods during which inventories were actually used in production and management processes |

| 7 | Monetary value determined at the time of registration |

| 8 | Amount of depreciation charges during use |

| 9 | Residual value, defined as the difference between the values from points 7 and 8 |

Sample of filling out the reverse side

When printing forms, it is important to take into account that the template form of the act of write-off of fixed assets is two-sided. The second part is characterized by the presence of two tables, the first of which contains information about individual object characteristics, including the presence of elements belonging to groups of precious metals.

The space below is reserved for recording the conclusion of the commission responsible for making the decision on deregistration, and is filled in in accordance with the verdict made based on the results of the expert analysis. If necessary, a list of related documentation is also provided, serving as an annex to the act. The signatures of the commission members are placed opposite the lines indicating their positions and full names.

The second table of the standard OS-4 form should contain the following data:

- The amount of associated costs arising as a result of partial or complete liquidation of fixed assets of the enterprise.

- List of surviving inventory items, the condition of which is recognized as meeting operational requirements.

- The amount of revenue received from the sale of disposed objects or their individual parts.

The final stage is the signing of the document by the chief accountant of the enterprise.

An example of drawing up an order

Making a hat

In the “header” of the document, in the middle of the line, the full name of the organization is written, then below after the word “order” its number is written (in accordance with the internal document flow), and also in the required line the locality in which the company operates is noted and the date the order was drawn up is indicated .

Main part of the order

The main part of the document describes

- reason for writing off the fixed asset,

- his name,

- inventory number,

- number according to the technical passport (if necessary),

- and also indicates the employee who is directly responsible for liquidating the object.

If parts, elements, assemblies and parts of a fixed asset can still serve the enterprise, they must be sent to the warehouse, which is also recorded in the order (with the appointment of a materially responsible employee).

The order must indicate the employee who must write off the object from accounting (indicating the position, surname, first name, patronymic of the specialist).

Document approval

Finally, the order must be signed by the head of the enterprise, as well as by all employees who participate in the write-off of fixed assets at its various stages and who are named in this document.

How to correctly draw up a write-off act in form OS-4

The current document flow procedure allows filling out the form both manually and electronically, so here the decision is made directly by the responsible employee. The main condition is the presence of original personal signatures of the head of the organization, as well as each member of the evaluation commission. But certification using a seal is not a mandatory requirement, since since 2016 the legislation has left the use of stamps and cliches as an optional right of legal entities.

The document is drawn up in two copies: the first of them is transferred for further work to the accounting department of the enterprise, serving as the basis for reflecting entries in the accounting program, the second is retained by the employee financially responsible for the property being written off, until the moment of transfer to the warehouse and subsequent disposal or sale. If necessary, it is also possible to increase the number of copies, each of which must be properly executed and certified.

How and for how long to store the document

The storage procedure involves placing the forms first in the general catalog of current documentation, using a separate identifying folder, and then in the archive - after the expiration date. The duration, determined by regulations as well as internal rules of the organization, may vary, but must be at least three years, after which destruction is permitted.

So, now you know what to write in the OS 4 form, and what results of write-off of fixed assets are recorded in the reporting.

It's time to simplify the accounting of enterprise property by taking advantage of practical mobile automation solutions from. Number of impressions: 3419

conclusions

Several conclusions can be drawn on this topic:

- To write off fixed assets, it is not necessary to draw up an order in the organization. However, it is recommended to do this, as it confirms the manager’s consent to the procedure.

- The law does not approve a special form of the document. Therefore, it can be compiled in free form. However, there are mandatory items that must be present on the form.

- The document is drawn up in one copy. You can make copies if necessary.

- The order can be typed on a computer or written by hand. In this case, errors and corrections are not allowed.

- The document must comply with all document flow rules approved by the head of the company.

- Stamps are not affixed to such documentation unless otherwise specified in the company’s internal documentation.

- The order has a period of execution of one year, and a period of storage in the archive of five years.

- Without an executive visa, it cannot be considered valid.