Determining fixed assets according to FAS 6/2020 - comparison with PBU

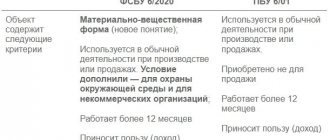

An asset can be defined as fixed assets in accordance with clause 4 of FSBU 6/2020 if it:

- exposed in a material form;

- involved in production or management purposes, used in environmental or statutory activities, intended for rental;

- will be in operation for more than 12 months or one operating cycle, if the latter exceeds the specified period;

- generates income or helps achieve goals.

What is new in the definition is the indication of a material form. However, initially the OS is not supposed to have a different form. Therefore, it cannot be said that the new definition is somehow strikingly different from the previous one.

PBU previously established the point that fixed assets are not acquired for sale. The FSB omitted this norm, so assets that will be resold in the future can be taken into account as part of the OS, but they will be regulated by PBU 16/02.

Paragraph 6 of FSBU 6/2020 leads us to the fact that its norms do not affect the accounting of capital investments and long-term assets for sale.

The procedure for determining inventory objects has been clarified

The traditional approach to determining inventory items of fixed assets is supplemented by recognition as an independent inventory item:

| AN OBJECT | EXPLANATION |

| Each part of one fixed asset, the cost and useful life of which differ significantly from the cost and useful life of the object as a whole | Earlier - with a significant difference only in the useful life |

| Significant expenses of the organization for repairs, technical inspection, maintenance of OS facilities with a frequency of more than 12 months or more than the usual operating cycle exceeding 12 months | Previously – included in period expenses |

What is the cost limit according to FSBU 6/2020

The previous accounting provision established the minimum value limit for recognizing an asset as a fixed asset at 40 thousand rubles. Accounting policy could reduce this limit, but it was not allowed to increase it. The federal standard does not in any way regulate the cost for inclusion in the OS. The most important thing is the duration of use for production and other specified purposes. Now business entities have the right to set the cost limit themselves (clause 5 of FSBU 6/2020), based solely on how long the asset will serve and generate income.

A ready-made solution from the ConsultantPlus legal reference system will help reclassify fixed assets in accordance with federal standard 6/2020. To view the material, get demo access to the system. It's free.

With the beginning of the application of the new FSBU 6/2020 “Fixed assets”, enterprises can raise the cost bar to 100 thousand rubles, defined by the Tax Code, and finally eliminate the differences between the two types of accounting.

One of the innovations is the ability to set a cost limit not for a unit of an OS object, but for a whole group of objects. In addition, such a limit may not have a monetary value: the criterion for classification as fixed assets is established, for example, as a percentage of the balance sheet item “Fixed assets”.

Thus, the standard gives complete freedom to classify assets as fixed assets. However, such freedom should not be abused. It is necessary to approach the establishment of indicators from the perspective of the level of materiality established by the accounting policy.

Checking the new book value as of 12/31/2021

Check the changed book value of fixed assets using the report Statement of depreciation of fixed assets for December 2021 through the section fixed assets and intangible assets .

At the end of the period, the data in the columns changed:

- Depreciation (wear and tear) - accumulated depreciation was recalculated according to FAS 6;

- Residual value is the changed book value due to adjustment of depreciation, according to which fixed assets will be reflected in the Balance Sheet as of 12/31/2022 in the form of an opening balance on line 1150 “Fixed Assets” in the column As of 12/31/2021 .

In tax accounting, the cost of fixed assets and accumulated depreciation have not changed.

On release 3.0.106.60, the indicators of the Asset Depreciation Statement for December 2021 are not generated correctly:

We are expecting a fix in future versions of the program.

Valuation and revaluation according to FAS 6/2020

Any fixed asset item in accounting comes at its original cost. Moreover, its definition is given by another regulatory act - FSBU 26/2020.

The initial cost is the amount of capital investment in the object. These include:

- the contractual value of the asset to be paid to the supplier;

- the cost of assets written off or depreciated in connection with their use in making capital investments;

- salary with deductions for compulsory social insurance accrued to employees participating in capital investments;

- estimated liability, including for future dismantling, disposal of property and environmental restoration.

After capitalization, the organization can continue to account for fixed assets at their original cost, or perhaps at a revalued cost. FSBU 6 reveals the nuances of revalued value.

Revaluation

Having chosen the valuation option at a revalued value, you need to understand that the revaluation of OS FSBU 6/2020 requires constant revaluation. The frequency of its implementation for various groups of fixed assets (with the exception of investment real estate) should be specified in the accounting policy. The revalued value should be as close as possible to the fair value, the essence of which is revealed by IFRS 13. This is the price at which market participants would conduct a normal transaction to sell the asset on the valuation date in current market conditions.

You can revaluate the original cost, or you can revaluate the book value. In the second case, there will be no entries for increases and decreases in accumulated depreciation.

The procedure for reflecting the revaluation of fixed assets according to FAS 6/2020 in accounting is similar to what was in effect previously:

- The revaluation amounts increase the additional capital: Dt 01 Kt 83, while for depreciation the entry is given: Dt 83 Kt 02.

- The markdown amounts are included in expenses: Dt 91/2 Dt 01, for depreciation - Dt 02 Kt 91/2 (83).

- If in previous periods the object was revalued upward, but in the current period it had to be revalued downward, then the cost of the markdown will reduce the amount of additional capital - Dt 83 Kt 01, for depreciation - Dt 02 Kt 91/2 (83).

Impairment

Starting next year, companies are required to check for impairment of fixed assets in accordance with FAS 6/2020. Thus, assets cannot be accounted for at an inflated value in the financial statements. In paragraph 38, the standard makes reference to the next international standard in force in our country - IFRS 16. Testing for impairment, as well as accounting for the changed book value will be carried out within the framework of the specified IFRS.

FSBU 6/2020 for small enterprises under this standard has approved small relaxations, which we will discuss below.

Valuation of fixed assets

Fixed assets are accepted for accounting at historical cost. It includes the entire amount of capital investments associated with the object.

Related article: Estimated liabilities in the balance sheet Read more

The initial cost of a fixed asset is also formed by estimated liabilities. This is a special category of expenses. For example, these may include expenses for future dismantling of property or for environmental restoration after the liquidation of a fixed asset.

Estimated liabilities may change during the operation of the asset. The following options are possible.

- The commitment itself has changed. In this situation, the original cost of the fixed asset is subject to adjustment.

- The value of the estimated liability has changed. The difference in this case is attributed to income or expenses of the period.

After accepting a fixed asset on its balance sheet, an organization has the right to account for it in one of two ways.

- At original cost. When choosing this option, the original cost of the object, as well as the amount of accumulated depreciation, remain unchanged. But there are a number of exceptions provided for by the new FSBU 6\2020 “Fixed Assets”. These include, for example, cases where an asset is being restored or upgraded through capital investment. The initial cost of the object increases accordingly by the amount of these injections.

- At an overvalued price. This option is more consistent with international standards and requires regular re-evaluation of the OS. The purpose of the event is to bring the value of objects to their fair value, which is determined in accordance with the rules of IFRS 13 “Fair value measurement”.

There are several options for revaluing fixed assets. For investment real estate, FSBU 6\2020 establishes special rules. This is real estate intended for rental or further resale at a premium. Such objects should be allocated to a separate group.

Paragraph 25 of FSBU 6\2020 defines the book value of fixed assets. This is the original cost minus depreciation and impairment. Thus, in accordance with the rules of the new standard, entities are now required to test assets for impairment. The procedure itself is regulated by IAS 36 “Impairment of Assets”.

Impairment is the condition of property in which its value on the balance sheet is greater than the amount that can be received from the use or sale of this object. Signs of impairment, for example, include depreciation (both moral and physical), unfavorable market conditions, or the liquidation of the line of business for which the asset was acquired.

Important: small enterprises on the simplified market have the right not to adjust the cost of fixed assets due to changes in estimated liabilities. Also, these business entities are allowed not to check fixed assets for impairment.

How FSBU 6/2020 regulates depreciation of fixed assets

The repayment of the cost of fixed assets in accounting according to FAS 6/2020, as before, is carried out through depreciation, which is accumulated in a separate account 02. There have been no changes in reflecting the amounts of accrued depreciation in accounting, the entries remain the same:

Dt 20, 25, 26, 44, ... Kt 02.

Changes have occurred in the calculation of the base for calculating depreciation; now the latter is calculated not from the original or replacement cost, but from the difference between the book value and liquidation value. The last indicator is another innovation introduced by the standard.

According to FAS 6/2020, liquidation value is the estimated value of assets that will remain after the liquidation of an asset, minus the costs of dismantling, disposal and other disposal.

EXAMPLE:

According to the report of an appraiser, an asset can be sold for 300 thousand rubles. The organization paid 50 thousand rubles for the dismantling of this asset, and another 30 thousand rubles for the removal and disposal of faulty parts. The liquidation value of the fixed asset is 220 thousand rubles. (300 thousand rubles - 50 thousand rubles - 30 thousand rubles)

As soon as the book value equals the liquidation value, depreciation stops accruing. The residual value must be reviewed regularly.

In some situations it may turn out to be zero. These include situations when:

- no proceeds are expected from the disposal of a fixed asset item (including from the sale of material assets remaining from its disposal) at the end of its useful life;

- the amount expected to be received from the disposal of a fixed asset item is not significant;

- the amount expected to be received from the disposal of a fixed asset cannot be determined.

In order to use the zero cost rule without any adverse consequences, it is advisable to obtain an opinion from the competent services. Liquidation value is an estimate, and it can only be given by specialists who use fixed assets in the organization’s activities. In this regard, if the liquidation value of fixed assets or their individual groups is reflected in the accounting records as equal to zero, it is better to support the accounting calculations with certificates or opinions from technical specialists.

To calculate depreciation according to FAS 6/2020, there are three methods instead of the four previously proposed by PBU 6/01. The new standard abandoned write-off based on the sum of the number of years of useful life.

Depreciation

The transition to FAS 6\2020 “Fixed Assets” involves significant changes in depreciation rules.

First of all, now depreciation is accrued constantly, even during periods of long downtime or mothballing of the facility, and is not suspended for this time, as before.

Non-depreciable property still includes land plots. The new standard also added investment properties accounted for at revalued amounts to this category.

By default, depreciation begins to accrue from the date the asset is accepted for accounting, and ends, accordingly, at the time of its disposal. However, another option is also possible: depreciation charges appear from the first day of the month following the month the object was put into operation, and cease from the first day of the month following the date of its disposal. The choice of this alternative must be fixed in the accounting policy.

The new rules allow for a situation in which depreciation is calculated not monthly, but immediately for the reporting period.

FSBU 6\2020 introduces definitions of the following elements of depreciation:

- liquidation value - income from the disposal of an object that a company can receive upon completion of its useful life;

- useful life – a period determined by organizations independently; in this case, such points as wear and tear, obsolescence, plans for replacing fixed assets, etc. are taken into account;

- method of calculating depreciation charges - the new standard offers several options: linear method, decreasing balance method, method of calculation proportional to the number of products or volume of work. The organization selects the most suitable one for each group of fixed assets. At the same time, the rules for calculating depreciation charges using the methods presented in FAS 6\2020 and PBU 6\01 differ in many respects.

Important: the amount of depreciation for the reporting period must be calculated so that by the end of the asset’s life, its book value and liquidation value are equal.

Sometimes the liquidation value is recognized as zero. This happens if:

- it is not planned to receive economic benefits after disposal of the fixed asset;

- the estimated amount that may be received upon disposal of the asset is immaterial;

- the amount of funds received from the disposal of the object cannot be determined.

Investment property - new standard

The standard identifies a separate group of fixed assets - investment property (IN). There was no such allocation in PBU 6\01. This group is formed from real estate acquired specifically to generate income from rental or increase in value.

Individual valuation and revaluation rules apply for individual assets.

Thus, the initial cost of an individual investment, as well as its revalued value, must always be equal to its fair value.

If the accounting policy stipulates that an individual asset is valued at a revalued value, then the revaluation will have to be carried out at each reporting date. Additional valuation and discounting of investment real estate in accordance with FSBU 6/2020 will increase or decrease the financial result:

- Dt 03 Kt 91/1 - additional assessment of the ID;

- Dt 91/2Kt 03 — markdown of ID was made.

We wrote above that the revaluation or depreciation of other fixed assets will affect the amount of additional capital (except for those cases when the previous revaluation amounts do not cover the amount of the current depreciation).

If, in accordance with the accounting policy, an individual asset is valued at a revalued cost, then depreciation will not be accrued on such objects.

Revaluation rules changed

After recognition, an item of fixed assets can be reflected in accounting at a revalued cost. At the same time, the value of such an object is regularly revalued so that it is equal to or does not differ significantly from its fair value ( previously , the object was revalued at its current (replacement) cost).

Fair value is determined in the manner prescribed by IFRS 13 “Fair Value Measurement”, put into effect in Russia by Order of the Ministry of Finance dated December 28, 2015 No. 217n.

All have the right to revaluate their assets ( previously only commercial organizations).

Revaluation is carried out as the fair value of fixed assets changes ( previously - no more than once a year at the end of the reporting period). At the same time, it is permissible to decide to conduct a revaluation no more than once a year (as of the end of the reporting year).

When carrying out a revaluation, along with a proportional recalculation of the original cost and accumulated depreciation of an asset, a method is acceptable in which the initial cost is first reduced by the amount of depreciation accumulated on it on the date of revaluation, and then the resulting amount is recalculated so that it becomes equal to the fair value of this object ( previously - only proportional recalculation).

The amount of accumulated revaluation can be written off to the organization’s retained earnings in one of two ways :

- One-time when writing off an overvalued asset.

- As depreciation accrues on such an object.

Previously - only at a time when an object is written off.

Revaluation of investment real estate is carried out in a manner different from the procedure for revaluation of other fixed assets. Main differences:

- revaluation is carried out at each reporting date;

- the initial cost of the object (including previously revalued) is recalculated so that it becomes equal to its fair value;

- revaluation or depreciation of an object is included in the financial result of the organization’s activities as income or expense of the period in which the revaluation of this object was carried out;

- revalued objects are not subject to depreciation.

An entity that decides to value investment property at a revalued value must apply this valuation method to all investment properties.

How to switch to FSBU 6/2020

Before switching to the new standard, you will need to complete several steps:

- conduct an inventory of fixed assets and other assets that, in accordance with FAS 6, could be classified as fixed assets;

- set a limit on the value of fixed assets - according to this criterion, the subsequent assignment of assets to a separate object or group of fixed assets will occur;

- determine the liquidation value of fixed assets listed on the balance sheet of the enterprise;

- adjust the rules for subsequent accounting, i.e. how fixed assets will be further accounted for - at original or revalued cost.

After all these issues are resolved, you can begin the transition to the new standard. Lawmakers have provided several transition options.

Promising way

A promising method - available only to those entities that have the right to keep records in a simplified way and prepare reports in a simplified form, i.e., in fact, only to small enterprises (clause 51 of FSBU 6/2020). The promising option is that it is possible not to recalculate accounting and reporting indicators before the date of transition to FAS 6/2020, and the standard is applied to those facts of the enterprise’s life that arose after the date of transition. With the prospective method of recording in accounting, only depreciation of fixed assets will be affected:

- Dt 84 Kt 02 - increased depreciation during transition;

- Dt 02 Kt 84 - reduction in depreciation.

Full retrospective method

This is a method in which all accounting records are adjusted as if the standard had been applied from the very beginning of the economic activity. The method comes down to a complete recalculation of balance sheet and financial results statements for previous periods. The postings will include account 84, with the help of which the book value of fixed assets and accumulated depreciation on existing objects will be adjusted.

Simplified retrospective method

It consists of recalculating the book value of fixed assets as of the date of transition (clause 49 of FSBU 6/2020). That is, if an organization switches to the standard from January 1, 2022, then it will make all adjusting entries on December 31, 2022. In this case, the balance sheet compiled for 2022 as of December 31, 2022 should be compiled without taking into account adjustments, and the balance sheet for 2022 as of December 31, 2022 will already be compiled taking into account adjustments. The difference will have to be explained.

The ready-made solution from K+ will tell you what accounting entries will appear in accounting during a retrospective transition to the federal standard. To familiarize yourself with all the transactions, sign up for a free trial access to the system.

Transitional provisions

As the Ministry of Finance notes, the consequences of changes in the accounting policies of an organization in connection with the start of application of FAS 6/2020 are reflected retrospectively - that is, as if this standard had been applied from the moment the facts of economic life affected by it arose.

To facilitate the transition to the new procedure for accounting for fixed assets in the financial statements, starting from which FAS 6/2020 is applied, the organization may not recalculate comparative indicators related to fixed assets for periods preceding the reporting period. To do this, you need to make a one-time adjustment to their book value at the beginning of the reporting period (the end of the period preceding the reporting period). For the purposes of such an adjustment, the carrying value of fixed assets should be considered their original cost (taking into account revaluations), recognized before the application of FAS 6/2020 in accordance with the previously applied accounting policy, less accumulated depreciation.

In this case, accumulated depreciation is calculated in accordance with FAS 6/2020 based on the specified initial cost, liquidation value and the ratio of the expired and remaining useful life, determined in accordance with FAS 6/2020.

The chosen method of reflecting the consequences of changes in accounting policies is disclosed in the first financial statements prepared using FAS 6/2020.

Source: information message of the Ministry of Finance dated November 3, 2020 No. IS-accounting-29.

Who is allowed to refuse to apply FSBU 6/2020 “Fixed Assets”

The norms of the federal standard do not apply only to organizations in the public sector. Even micro-enterprises will not be able to refuse it. However, for those who have the right to keep records in a simplified way and prepare reports in a simplified form, certain relaxations have been introduced. These business entities have the right not to apply certain points of the standards in accounting (clause 3 of FSBU 6). For example, they may not adjust the estimated liability for dismantling, disposal and restoration of the environment (clause 23), or not check the value of fixed assets for impairment (clause 38).

Thus, almost all companies must comply with the new provisions.

Results

So, we compared PBU 6 and FSBU 6. The provisions of the new standard are quite different from the provisions of its predecessor. New elements have emerged, such as investment properties and salvage values. The rules for calculating depreciation have changed: the standard has eliminated the cumulative method and clarified the basis for calculating depreciation. Business entities now independently set a value limit at which an asset is included in the fixed assets, and this limit may not have a monetary value.

The mandatory application of the new standard begins on January 1, 2022; at the request of the company, they had the right to make an early transition to FSBU 6/2020.

You can download FSBU 6/2020 “Fixed Assets” from various government portals. One of the official sites is cited by us as a source and is located at the end of our article.

Sources:

- Order of the Ministry of Finance of Russia dated September 17, 2020 No. 204n “On approval of Federal Accounting Standards FSBU 6/2020 “Fixed Assets” and FSBU 26/2020 “Capital Investments””

- Accounting Regulations “Accounting for Fixed Assets” (PBU 6/01)

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

What are fixed assets?

FSBU 6/2020 “Fixed assets” was approved by Order of the Ministry of Finance of Russia dated September 17, 2020 No. 204n.

It must be applied to both commercial and non-commercial enterprises. In this case, the size of the legal entity does not matter. Representatives of small businesses have the right not to follow only certain provisions of the document, but in general must keep records of fixed assets in accordance with FAS 6\2020. A comparison of the standard with the previously existing PBU 6\01 shows that the new act is more consistent with IAS 16 than its predecessor. Many adjustments were made to it, designed to bring the accounting of fixed assets in the Russian Federation closer to international templates. FSBU 6/2020 slightly modifies the very concept of “fixed asset”. Now this property includes assets that meet the following conditions:

- The presence of a material form. Previously, this criterion was not specified in the standard, although it was implied in practice.

- Intended for use in the normal activities of the company: production of products, performance of work and provision of services, sale of goods, rental of any objects for temporary use for a fee, implementation of management functions. The new standard adds environmental protection measures to this list.

- Long expected service life. We are talking about a minimum of 12 months. If the operating cycle of a legal entity exceeds a year, then the duration of this turnover is taken as the limit.

- Specific purposes for using the asset:

- for commercial legal entities – obtaining economic benefits;

- for non-profit associations - performing the tasks for which the society was created (usually they are enshrined in the charter of such organizations).

In accordance with clause 5 of FAS 6\2020, a business entity has the right to set a cost limit as a criterion for classifying a property as a “Fixed Assets” category. Anything that costs less than this amount will be considered “low value.” And the new standard no longer applies to such assets.

It is permissible to set the cost limit not only as a fixed amount, but also as a percentage of the total cost of the company’s fixed assets. For example, a legal entity can establish a similar provision in its accounting policy: groups of assets are considered insignificant until their value reaches 4% of the total value of fixed assets.

Expenses on low-value property are written off as period expenses. However, each company is required to properly account for such assets. The most popular options are the use of off-balance sheet accounts or special statements.

The value of the cost limit for classifying objects as fixed assets and the features of accounting for “low value” must be reflected in the accounting policy.

So, accounting for fixed assets is now regulated by FSBU 6\2020. Clause 6 of the document clarifies that the act does not apply to the following types of assets:

- capital investments;

- long-term assets intended for sale.

Separate standards are provided for these categories of property.

ConsultantPlus experts explained in detail how to disclose information in reporting when applying FAS 6/2020 “Fixed Assets” and FAS 26/2020 “Capital Investments”. Go to the Ready-made solution, get a trial demo access, and find out the answer to this question for free.