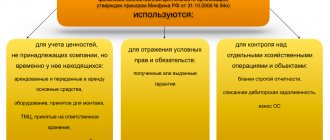

Why are off-balance sheet accounts of MC needed (MC.01, MC.02, MC.03, MC.04)

In the chart of accounts of the 1C: Accounting program there is a number of additional off-balance sheet accounts in addition to the 11 generally accepted ones.

This is done for more thorough and convenient accounting. Account MC.04 is a subaccount of the MC account “Material assets in operation” along with three more subaccounts:

- MC.01 “Fixed assets in operation”,

- MC.02 “Workwear in operation”,

- MTs.03 “Special equipment in operation.”

МЦ.02—an off-balance sheet account used to account for special clothing issued to an employee to perform his official duties. Account MTs.03 accumulates information on special tools and equipment transferred into operation. Account MTs.01 is often used if the fixed asset is reflected differently in tax and accounting.

The introduction of these accounts into accounting is due to the need to control property written off from the organization’s balance sheet, included in costs, but used in the organization’s economic activities. Their debit reflects the values to be accounted for, broken down by item items, financially responsible persons and storage locations. The loan reflects the write-off of assets. In this case, transactions are recorded only in debit or only in credit of such accounts - correspondence is not typical for off-balance sheet accounts.

You can familiarize yourself with the features of using off-balance sheet accounts in accounting in the article “Rules for maintaining accounting on off-balance sheet accounts.”

The procedure for off-balance sheet accounting of material assets

The movement of material assets behind the balance sheet of an enterprise is carried out by simple transactions and does not involve double entry into accounts; off-balance sheet accounts do not correspond either with balance sheet accounts or with each other. Off-balance sheet accounting of material assets is carried out on the basis of primary accounting documents: claims-invoices, acts of acceptance and transfer of fixed assets, material assets for storage.

Analytical accounting is carried out in the context of the type of valuables, counterparties of the enterprise (owners, suppliers, lessors), storage locations and, in the case of personal liability of specific persons who were entrusted with the storage of the relevant objects.

Reflection of business transactions by postings to off-balance sheet accounts

| Operation | Debit | Credit |

| Obtaining lease of fixed assets | 001 | — |

| Return of previously leased fixed assets to the owner | — | 001 |

| Acceptance of inventory items for safekeeping | 002 | — |

| Return of previously accepted inventory items to the legal owner | — | 002 |

| Receipt of customer-supplied raw materials for processing | 003 | — |

| Disposal of customer-supplied raw materials - manufacturing of products from them | — | 003 |

| Receiving goods on consignment | 004 | — |

| Goods sold under a commission agreement | — | 004 |

| Equipment has been accepted for installation to the customer | 005 | — |

| Completed installation and installation of equipment for the customer | — | 005 |

| Strict reporting forms received | 006 | — |

| Strict reporting forms were used | — | 006 |

| Strict reporting forms are damaged and unusable | — | 006 |

The basis for mandatory write-off from the off-balance sheet accounting of an enterprise is the placement of this property on the balance sheet upon transfer of ownership rights to the object to the organization itself:

- repurchase of leased property from the lessor,

- transfer of ownership rights to material assets previously transferred free of charge,

- payment under the contract for raw materials previously received for processing, etc.

Entries on the debit of account MTs.04

According to the Chart of Accounts (order of the Ministry of Finance of the Russian Federation dated October 31, 2000 No. 94n), the balance sheet account 10.09 is used to capitalize inventory and household supplies. To reflect this business operation in the 1C: Accounting program, the document “Receipt of goods and services” is provided.

When instruments and other inventory are accepted for accounting, a new document is created with the transaction type “Purchase, commission”. The document is filled out indicating:

- what has to happen

- from whom,

- in what quantity,

- at what price.

Account 10.09 “Inventory and household supplies” is selected as a debit accounting account.

An entry in the credit of account 10.09 occurs when inventory and other household property are transferred into operation. For this purpose, a document “Transfer of materials into operation” is created and carried out.

When transferring inventory, fill out the “Inventory and Household Supplies” tab:

- the nomenclature of transferred values is selected by position,

- the employee accepting them for use,

- the accounting account 10.09 and the method of reflecting costs are indicated.

When posting a document, values are written off from accounting account 10.09 to the cost account. At the same time, these values are debited to account MTs.04 in the context of nomenclature, quantity and financially responsible persons. In this way, proper control over the safety of the organization’s property can be organized.

The document “Transfer of materials into operation” allows you to print the issue record sheet (form MB-7) or the demand invoice (form M-11). If necessary, you can change the financially responsible person responsible for the safety of economic assets recorded on the balance sheet.

Off-balance sheet accounting of materials and equipment

In addition to fixed assets and goods, other material assets can be taken into account on the balance sheet.

Inventory in safekeeping

In some cases, buyers cannot account for material assets on balance sheet accounts. In this case, records should be kept.

Invoice 002 is needed if the buyer accepted inventory items for storage when:

- receiving goods and materials from suppliers for which the organization legally refused to accept invoices of payment requests and pay them;

- receiving from suppliers unpaid inventory items that cannot be used under the terms of the contract until they are paid;

- receipt of goods and materials, the ownership of which has not been transferred to the organization, etc.

Note! VAT deduction cannot be claimed while inventory items are taken into account on the balance sheet (letter of the Ministry of Finance of Russia dated August 22, 2016 No. 03-07-11/48963).

Suppliers can also take into account inventory items on account 002 if the goods are paid for, but not removed by the buyer for reasons beyond the control of the organizations.

Provided raw materials

If a company works with customer-supplied raw materials, then account 003 “Materials accepted for processing” is used for accounting. Most often, they work with customer-supplied raw materials during the construction of facilities. In this case, the customer’s building materials are used to complete the work. Also, customer-supplied raw materials are used in the production of products for the customer. While the manufacturing process is underway, customer-supplied materials are accounted for in account 003.

Reception of customer-supplied raw materials is reflected in the debit of account 003, disposal (return of remaining raw materials or manufactured products) is reflected in the credit of account 003. Analytical accounting in account 003 is carried out by customers, types, grades of raw materials and materials and their locations.

Installation equipment

When installing equipment owned by the customer, contractors keep records of the equipment in account 005 “Equipment accepted for installation.”

Acceptance of equipment for installation is reflected in the debit of account 005; write-off of equipment from accounting after installation and delivery of it to the customer is reflected in the credit of account 005. Analytical accounting is carried out for customers, objects, and components of the equipment being installed.

Recording property in off-balance sheet accounts will help control its safety. Also, such accounting will increase the vigilance of financially responsible persons and help the company avoid fines.

Transfer of materials into operation in 1C 8.3: method of reflecting expenses

When producing products, organizations use workwear, as well as various equipment and household equipment. As a rule, the service life of these auxiliary materials does not exceed 12 months. According to accounting rules, such assets, regardless of cost, are recognized as inventory and written off when transferred to production. How to reflect the transfer of materials into operation in 1C 8.3, and which method of reflecting expenses to choose in 1C 8.3, read this article.

Accounting for workwear, equipment and equipment is strictly regulated by law. The transfer of these materials into operation in 1C 8.3 is reflected in the debit of the production cost accounts. In this case, a special primary document is drawn up. For example, when writing off workwear, fill out the MB-7 statement “Registration of the issuance of workwear, safety shoes and safety devices.” When issuing inventory or special equipment, a demand invoice is drawn up in form M-11. The transfer of materials into operation in 1C is done using a special document “Transfer of materials into operation”. In it you need to configure the “Methods of reflecting expenses” directory. Read on to learn how to set up ways to reflect expenses in 1C when transferring materials into operation, and how to formalize the transfer of inventory into operation in 1C 8.3 in 6 steps.

Quick transfer of accounting to BukhSoft

Accounting for materials on off-balance sheet accounts - regulatory nuances

The most common use of off-balance sheet subsidiary accounts is to record low value items or materials. At the same time, analytics is organized in the context of counterparties (retailers, consignors, suppliers, etc.), types of inventory items, storage locations, materially responsible persons (MRP). The basis is primary documents - acts of transfer for storage, acts of write-off, invoices, claims, etc.

Off-balance sheet accounts for inventory accounting:

- 002 – values that are accepted by the company for safekeeping or become property only after fulfillment of contractual conditions are reflected here. For example, after full payment of the purchase price.

- 003 – materials received by the organization for further customer processing are reflected here.

- 004 – here the commission agent takes into account goods received from the principal for sale.

Transfer of special clothing into service

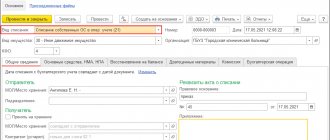

Step 1. Create in 1C 8.3 the document “Decommissioning of materials into operation”

Go to the “Warehouse” section (1) and click on the “Transfer of materials for operation” link (2). A window for generating a document will open.

In the window that opens, click the “Create” button (3). A document will open for you to fill out.

In the form to fill out, please indicate:

- your organization (4);

- transfer date (5);

- warehouse from which work clothes are written off (6);

- department to which special clothing is transferred (7).

MOVING FROM “1C” TO “BUKHSOFT” Transferring data from your “1C” is now easy! BukhSoft transfers all data without loss and checks it!

Step 2. Fill out the “Workwear” tab in the document “Decommissioning of materials”

In the “Workwear” tab (1), click the “Add” button (2). In the “Nomenclature” field (3), select the required workwear from the nomenclature directory. Next, fill in the fields:

- "Quantity" (4). Indicate the quantity of protective clothing to be transferred;

- "Individual" (5). Select the employee to whom the workwear is transferred;

- “Purpose of use” (6). Here, specify the accounting parameters for writing off workwear. Use the cost repayment method “Repay the cost upon transfer into operation.” In the method of recording expenses, indicate the write-off account, for example “01/20”.

The “Account Account” (7) and “Transfer Account” (8) fields will be filled in automatically. To complete the operation, click the “Record” (9) and “Pass” (10) buttons. Now in the accounting records there are entries for the transfer of special clothing into operation.

Click the “DtKt” button (11) to view the accounting entries for this operation.

The entries show that account 10.11.1 “Special clothing in use” reflects the transfer of special clothing (12) and the write-off of its cost as expenses (13). The write-off is reflected in the debit of account 20.01 “Main production” (14). On the special account MTs.02 “Workwear in use” (15) in 1C 8.3, records of workwear are kept for each employee to whom one was issued. If the workwear has become unusable, write it off from this account using the document “Write-off of materials from use.”

Write-off of materials to an off-balance sheet account

An organization can take into account not only other people's material assets on its balance sheet, but also its own. An example would be low-value property, household supplies and inventory that are used for more than 1 year, costing less than the limit for accepting an object for accounting as fixed assets (the organization sets this limit independently in its accounting policy, but it cannot be more than 40,000 rubles in accordance with p. 5 PBU 6/01).

Such materials are written off as expenses at a time. But due to the long period of use, it is necessary to organize control over their safety. For this purpose, you can create a record sheet for household supplies and equipment in use, or you can keep off-balance sheet accounting. In the Chart of Accounts, approved. By order No. 94n, there is no special account for these purposes, so the organization can develop an off-balance sheet account independently and approve the chosen procedure for writing off low-value materials in the accounting policy.

If you use the 1C:Enterprise computer program for accounting, then in the chart of accounts of this program, special off-balance sheet accounts are provided for accounting for low-value materials written off the balance sheet:

If the company decides to take into account the low value off the balance sheet, then the postings will be as follows:

20, 23, 25, 26, 29, 44

Released from inventory warehouse

Off-balance sheet account “Inventory and household supplies”

Inventory and materials transferred into operation are registered

Off-balance sheet account “Inventory and household supplies”

Such inventory items are written off from the off-balance sheet account:

- after they are completely worn out, an MB-8 act or another document is drawn up, developed taking into account the requirements for mandatory details (clause 2 of article 9 of law No. 402-FZ);

- sale, gratuitous transfer and other disposal.

Transfer of special equipment into operation

If the cost of special clothing is completely written off when issued to employees, then the cost of special equipment can be written off in three ways:

- proportional to production output;

- straight-line write-off method;

- once in full amount upon commissioning.

The write-off method is configured in the “Purpose of Use” directory. Read on to find out how to do this.

Step 1. Fill out the “Special Equipment” tab in the “Decommissioning of Materials” document

In 1C 8.3, special equipment, as well as special clothing, is transferred to production using the document “Writing off materials for use.” How to create a document and fill out its basic details is described in step 1 of the previous section. To transfer special equipment to production, the “Special equipment” tab (1) is provided. In this tab, click the “Add” button (2). In the “Nomenclature” field (3), select the equipment for commissioning from the nomenclature directory. In the “Quantity” field (4) indicate the quantity of equipment to be transferred.

Step 2. Set up the “Purpose of Use” directory to account for the write-off of special equipment

As we wrote earlier, there are three ways to write off the cost of special equipment. The write-off method is configured in the “Purpose of use” field (1). Click button (2) to configure the payment method. The “Use Purpose” settings window will open.

In this window, in the “Repayment method” field (3), select one of three methods, for example “Linear”. In the “Useful life (in months)” (4) field, indicate how many months the cost will be repaid with a straight-line write-off. In the method of recording expenses (5), indicate the write-off account, for example, 20.01. To save the setting, click “Save and close” (6).

Step 3. Reflect in accounting the transfer of special equipment into operation

The “Account Account” (1) and “Transfer Account” (2) fields in the “Special Equipment” tab will be filled in automatically. To complete the transfer of special equipment to production, click the “Record” (3) and “Pass” (4) buttons. Now in the accounting records there are entries for the transfer of special equipment into operation. Press the “DtKt” button (5) to check the wiring. The posting window will open.

The postings show that account 10.11.2 “Special equipment in operation” reflects its movement upon transfer to the workshop (6) and the write-off of its value as expenses (7). In our example, the linear cost repayment method is established. Therefore, in accounting, the amount is repaid through depreciation when the “Month Closing” operation is launched. In tax accounting, the amount is repaid immediately (8). The write-off is reflected in the debit of account 20.01 “Main production” (9). On a special account MTs.03 “Special equipment in operation” (10) in 1C 8.3, equipment records are kept for each department. If the equipment has become unusable, write it off from this account using the document “Write-off of materials from use.”

Transfer of equipment and household supplies into operation

Step 1. Fill out the “Inventory and Household Supplies” tab in the “Materials Write-off for Operation” document

In 1C 8.3, household equipment, as well as workwear, is transferred in the document “Writing off materials for use.” How to create a document and fill out its basic details is written in step 1 of the section “Transferring workwear into operation.” To transfer household equipment, the “Inventory and Household Supplies” tab (1) is provided. In this tab, click the “Add” button (2). Next, fill in the fields:

- "Nomenclature" (3). Select the required inventory from the item directory;

- "Quantity" (4). Indicate the quantity of transferred inventory;

- “Individual” (5). Select an employee responsible for storing inventory;

- “Method of recording expenses” (6). In this directory, choose a method for recording expenses, which indicates an account for writing off the cost of inventory as expenses, for example, account 25.

The “Account” field (7) will be filled in automatically. To complete the operation, click the “Record” (8) and “Pass” (9) buttons. Now in accounting there are entries for the transfer of inventory into operation.

Click the “DtKt” button (10) to view the accounting entries for this operation.

The entries show that the write-off of the cost of inventory is reflected in the debit of account 25 “General production expenses” (11). On a special account MTs.04 “Inventory and household supplies in operation” (12) in 1C 8.3, inventory is kept track of the employees to whom it is issued. If the inventory has become unusable, write it off from this account using the document “Write-off of materials from use.”

Types of off-balance sheet accounts

There are the following off-balance sheet accounts provided for in the Chart of Accounts.

To account for property that does not belong to the organization, off-balance sheet accounts are used:

- 001 “Leased fixed assets.” This account reflects the leased fixed assets at the valuation specified in the agreement;

- 002 “Inventory assets accepted for safekeeping.” If inventory items are received by the company, but under the terms of the contract, ownership of them is transferred to the organization after certain conditions are met (for example, after transfer of 100% of payment), then the company reflects such inventory items on off-balance sheet account 002;

- 003 “Materials accepted for processing.” This account reflects the customer's raw materials and materials accepted for processing (supplied raw materials), which are not paid for by the manufacturer;

- 004 “Materials accepted for commission” This account reflects goods accepted by the commission agent for sale;

- 005 “Equipment accepted for installation.” This account reflects the equipment received by the contractor from the customer for installation.

- To account for the organization's property written off as expenses, off-balance sheet accounts are used:

- 006 “Strict reporting forms.” This account reflects strict reporting forms - receipt books, forms of certificates, diplomas, various subscriptions, coupons, tickets, forms of shipping documents;

- 007 “Debt of insolvent debtors written off at a loss.” This account reflects the debt of insolvent debtors, taken into account on the balance sheet for five years after write-off in case of a change in the property status of the debtors.

To collect information for disclosure in notes to financial statements, off-balance sheet accounts are used:

- 001 “Leased fixed assets”;

- 011 “Fixed assets leased out.” If, under the terms of the lease agreement, the property is taken into account on the balance sheet of the tenant (tenant), then for the owner it is reflected in account 011 “Fixed assets leased”;

- 008 “Securities for obligations and payments received.” Account 008 “Securities for obligations and payments received” is intended to summarize information on the availability and movement of guarantees received to secure the fulfillment of obligations and payments, as well as security received for goods transferred to other organizations (individuals);

- 009 “Securities for obligations and payments issued.” Account 009 “Securities for obligations and payments issued” is intended to summarize information on the availability and movement of guarantees issued to secure the fulfillment of obligations and payments. If the guarantee does not specify the amount, then for accounting purposes it is determined based on the terms of the contract.

At the same time, the Organization can also open off-balance sheet accounts not provided for in the Chart of Accounts.

It should be noted that you should not neglect accounting for business transactions on off-balance sheet accounts, since during a tax audit, goods, fixed assets, etc., not accounted for anywhere, can be regarded as surpluses, which in accounting are classified as non-operating income and on which income tax must be paid .