How often an inventory of fixed assets is carried out at an enterprise and why it is needed (in detail) are questions that we will examine in the article. The procedure for this procedure is strictly regulated and cannot be deviated from. Moreover, if during the inspection unaccounted for objects are identified, this may result in fines and punishments from the inspection authorities. The process itself is not as simple as it seems, because you need to formalize it correctly, identify discrepancies between actual and planned quantities, and record these changes. Let's look at all the details in order.

What is it - an inventory of fixed assets (fixed assets) at an enterprise

First of all, this is a recalculation of the assets that the company has. With this action, it becomes possible to keep the company's property unharmed. Its main task is to compare real and virtual balances by checking the data specified in the accounting records. This is how money, equipment, buildings, debt obligations and much more are considered.

Using the census, you can monitor the correctness of information reflected in the organization’s accounts. Corrections are made as necessary to keep the reporting current.

During the inventory, determine:

- are there actually objects that are indicated on paper and in the program;

- How correctly are inventory numbers assigned?

- Are accounting records maintained correctly?

- volumes of shortages/surpluses.

Terms, rules, frequency of inventory of fixed assets

According to the law, an inspection should be carried out at least once every 3 years at the enterprise. Library collections will not have to be counted and checked so often - once every five years. This is established on the basis of the Methodological Instructions.

Each company determines specific data for itself. This is usually done before the start of the annual report. But according to the law, there are cases when this should be done more often:

- as a result of an emergency;

- if reorganization or liquidation has begun;

- the property is going to be rented out or completely sold;

- The MOL or manager will change soon;

- annual reporting will be prepared soon;

- facts of theft, damage to property or abuse of authority were identified.

It is worth noting that if team members demand, then such a reconciliation is also carried out in the case when more than half of all participants in the contract leave.

By order of the owner or director of the organization, this can happen suddenly, at any time. There is a continuous inventory, when everything that is in the company is counted, and a selective inventory, when they count the assets in one division, branch or even office.

What is inventory?

Inventory is one of the procedures for monitoring the safety of company property.

Its essence is in comparing the actual availability of valuables (money, equipment, buildings, as well as liabilities) with accounting data. The procedure for conducting an inventory of fixed assets is regulated by the following legislative acts:

- methodological guidelines for inventory of property and financial obligations (Order of the Ministry of Finance dated June 13, 1995 No. 49);

- regulations on accounting and accounting in the Russian Federation (Order of the Ministry of Finance dated July 29, 1998 No. 34n);

- Law “On Accounting” dated December 6, 2011 No. 402-FZ.

The company must conduct an inventory not only of its own property, but also of stored or leased property. The inventory is carried out at the location of the property and in the presence of the financially responsible person or the team leader, if we are talking about collective financial responsibility.

What is an inventory of fixed assets

This is a count of objects that are constantly used during production or for administration needs. This may include machines, equipment, equipment, including computers, various household equipment, livestock and plants.

The recount can be natural - when inspectors or authorities walk around the company and check the actual presence of assets. Another option is documentary, when they are reconciled only using accounting registers.

Legally, all this is formalized depending on what supporting documents were developed within the enterprise and secured by accounting policies through an order. A statement is a document that will be drawn up in 2 identical forms, because one is sent to the accountant, and the second remains with the MOL.

Ready-made solutions for all areas

Stores

Mobility, accuracy and speed of counting goods on the sales floor and in the warehouse will allow you not to lose days of sales during inventory and when receiving goods.

To learn more

Warehouses

Speed up your warehouse employees' work with mobile automation. Eliminate errors in receiving, shipping, inventory and movement of goods forever.

To learn more

Marking

Mandatory labeling of goods is an opportunity for each organization to 100% exclude the acceptance of counterfeit goods into its warehouse and track the supply chain from the manufacturer.

To learn more

E-commerce

Speed, accuracy of acceptance and shipment of goods in the warehouse is the cornerstone in the E-commerce business. Start using modern, more efficient mobile tools.

To learn more

Institutions

Increase the accuracy of accounting for the organization’s property, the level of control over the safety and movement of each item. Mobile accounting will reduce the likelihood of theft and natural losses.

To learn more

Production

Increase the efficiency of your manufacturing enterprise by introducing mobile automation for inventory accounting.

To learn more

RFID

The first ready-made solution in Russia for tracking goods using RFID tags at each stage of the supply chain.

To learn more

EGAIS

Eliminate errors in comparing and reading excise duty stamps for alcoholic beverages using mobile accounting tools.

To learn more

Certification for partners

Obtaining certified Cleverence partner status will allow your company to reach a new level of problem solving at your clients’ enterprises.

To learn more

Inventory

Use modern mobile tools to carry out product inventory. Increase the speed and accuracy of your business process.

To learn more

Mobile automation

Use modern mobile tools to account for goods and fixed assets in your enterprise. Completely abandon accounting “on paper”.

Learn more Show all automation solutions

Commission for Inventory of Fixed Assets

The tasks of these people include inspection and verification of the correspondence of virtual balances to real ones. They record all the differences in the statement they have, write down inventory numbers, and monitor the characteristics.

They receive all relevant documents before starting their study. Who will be part of the inspectors fits into IVN-22. Financially responsible persons must mark that they hand over everything accountable.

Not only accounting sheets are subject to study and reconciliation, but also:

- information according to which it is possible to determine ownership of objects;

- technical passports;

- availability of documentation for natural resources owned by the company.

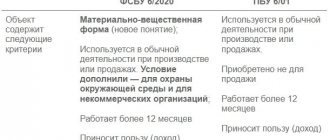

What applies to fixed assets under the new standard

An object can be classified as fixed assets if it satisfies clause 4 of the standard:

- It has a material form. Previously, this criterion did not exist, although in practice it was implied.

- Intended for use by an organization in its normal activities, both commercial and non-commercial. In this case, the object may not actually be used. The new standard has added environmental protection to the list of possible areas for using fixed assets.

- The company expects to use the facility in the future for a long time:

- receive income with its help if we are talking about a commercial company;

- achieve the goals defined by the charter of the non-profit organization.

In general, the period of use of the object must be more than 12 months. If the business's operating cycle exceeds 12 months, then the organization must plan to use the facility for a period of time exceeding the operating cycle.

The new standard does not apply to the following accounting items, even if they have the listed characteristics (clause 6 of FSBU 6/2020):

1. Capital investments - a separate standard FSBU 26/2020 has been developed for them.

2. Long-term assets intended for resale. Such assets are accounted for in accordance with PBU 16/02.

Purpose and reasons for conducting an inventory of fixed assets

There are several reasons to perform such a study of warehouses and operating systems:

- it is possible to speak with certainty about the presence or absence of certain objects on the territory;

- it becomes easy to compare the actual data with those indicated in the accounting registers;

- it is allowed to correct the accounting document in accordance with the information revealed in fact.

When an inspection is carried out unscheduled, this usually happens due to discovered theft, the consequences of an emergency, or a change in management.

Nowadays it is allowed not to use strict reporting forms, but to develop your own accounting documentation. The main thing is to have all the details and positions. If you don’t have time to develop such templates, you can use standard examples in the program.

It is important that the software completely covers all tasks that arise in the enterprise. If this does not happen, then you can seek help from professionals, for example, at.

Thus, you can effectively check an enterprise’s OS using the “OS Inventory” software product.

This software allows you to use an information collection terminal with a built-in barcode reader to reconcile company fixed assets.

Each OS comes with a unique barcode label that can be printed using the driver. A standards-compliant, 100% readable barcode is automatically generated by the software based on the accession number.

The software allows you to upload information about the availability of a particular material from the 1C database, and then use the device to collect barcodes of real positions of fixed assets and balances and then load the received real information into “Inventory of fixed assets” or into “Entering balances of fixed assets and intangible assets” and for receiving availability and discrepancy reports.

The software also supports accounting by materially responsible persons (MRO) and departments.

The program supports the simultaneous existence of multiple records on one TSD. In this way, you can conduct a check in several rooms/departments of the organization and then get several results at once in 1C.

Body carrying out inspection and accounting

Since inventory is recognized by law as a mandatory and regular action, it is advisable to have a permanent inventory commission at the enterprise, which has the following responsibilities:

- preventive measures aimed at preserving material assets;

- participation in resolving problems related to the management of storage issues and possible damage to property funds;

- control of documentary support of the dynamics of material assets;

- ensuring the inventory process in all its aspects (instructing commission members, carrying out the inspection itself, preparing relevant documentation);

- registration of inventory results.

The composition of the commission is approved by the management of the organization, registered in accordance with the order and recorded in the Logbook for monitoring the implementation of orders (decrees, instructions) to conduct an inventory (form No. INV-23). It can include:

- administrative workers;

- accounting employees;

- internal auditors or independent experts;

- representatives of any specialty working at the enterprise.

If the volume of property assets is small, then the function of the inventory commission can be assigned to the audit commission in cases where it operates at the enterprise.

IMPORTANT! If during the actual inspection the absence of even one member of the commission is recorded, then the inventory is not considered valid.

Required accounting documents

The most relevant papers, without which an inventory of fixed assets (FA) cannot be carried out:

- inventory - INV-1 - here everything that matches or differs in the actual balances from the planned ones is written down, including inventory numbers and violation of operational features;

- INV-22 - an order that is drawn up before the start of the census;

- INV-18 – matching statement;

- INV-23 is a journal in which all recalculations must be reflected.

It is worth remembering that INV-18 must be drawn up in 2 copies, because one is given to the MOL, and the second goes to the accounting department.

Conservation of fixed assets

If the equipment is not used for any reason, the manager may decide to mothball fixed assets. A commission is created that draws up a protocol on the conservation of fixed assets, indicating the reasons and deadlines. An act on the transfer of fixed assets to conservation is drawn up. An inventory of objects subject to conservation is required.

If the facility is closed for a period of more than three months, depreciation is not charged on the fixed asset. Mothballed properties are not excluded from the tax base; we continue to pay taxes on them.

Expenses for the conservation of fixed assets are taken into account by the following posting: D91/2 K20 (23, 26, 10, 70) .

Read more about conservation in the article: → Conservation of fixed assets in 2022

Next, we’ll talk about ways to dispose of fixed assets from an enterprise.

Download

sample forms for inventory at the enterprise: INV-1 Inventory listINV-1a Inventory list of intangible assets INV-3 Entering data into the inventory list INV-4 Inventory of shipped ]INV-5 Inventory of goods and materials accepted for storage[/anchor] INV-6 Inventory of goods and materials on the wayINV-15 Inventory of cash availabilityINV-17 Inventory of settlements with buyers and suppliersINV-18 Comparison sheet of inventory resultsINV-19 Comparison sheet of inventory items INV-22 Order for inventory INV-26 Accounting for inventory resultsHow is an inventory of materials carried out?

What is the documentation of inventory accounting for unusual fixed assets (FPE)?

There are several situations in which actions will be slightly different from usual:

- if the inventory was under repair at the time of repair, then an INV-10 should be drawn up, which will reflect the total cost along with the costs of correction;

- for those objects that were leased, you will have to draw up your own documentation with confirmation from the counterparty;

- separate papers are needed for those materials that cannot be used further in business activities, and it is impossible to restore them - they are written off with an indication of the reasons.

In addition, if the material has changed its purpose after repair, it is important to enter updated, current data. This is especially true in cases where, after such reconstruction, the book value changes, which has not yet been reflected in accounting.

OS Inventory Rules

The main point of inventory is to determine the actual presence and condition of an object in order to adjust the existing accounting data if necessary. This is indicated by the rules for conducting OS inventory (pr. No. 49):

- An object not accepted for accounting, as well as in cases where incorrect data is indicated on it or data is missing, the commission must describe on the spot correctly and completely, include all technical indicators and other indicators for it in the inventory. Example: for buildings, indicate the materials of construction, purpose, measurements, area, number of floors (except for basements), date of construction.

- Market valuation must be applied to any unaccounted for items discovered. Wear is determined based on actual condition. To register such objects, a corresponding act is drawn up.

- In case of actual re-equipment (expansion, reconstruction, restoration), as a result of which the object is used for a different purpose, updated information is entered into the inventory.

- If the commission established that major work was carried out at the facility: premises were added, floors were completed; or a part has been scrapped or liquidated, pay attention to how the object is reflected in accounting. If the changes are not reflected, it is necessary to adjust the book value of the fixed assets based on the data from the primary documentation of the work. The inventory provides information about the changes.

As a general rule, machines, equipment, and transport are entered individually, indicating technical characteristics, manufacturer and other significant data. In some cases, the same type of inventory, machines and tools that have the same cost and are used in one division of the organization are taken into account in the inventory card of the appropriate form as a group. In the inventory they are reflected in one line indicating the actual number of objects.

Objects that have been temporarily removed from their parking areas, are in use, or are located outside the organization’s territory (for example, railway rolling stock, machinery, vehicles undergoing major repairs) must be inventoried in advance, prior to disposal. At the same time, it is advisable to inventory assets that are under repair by entering data into a separate form INV-10 (act). The commission inspects the facility under repair and compares the actual costs of repairs with the planned ones. The act reflects data on savings or overexpenditures, which are subsequently used for analysis and identification of economic reserves. The percentage of technical readiness of the object is indicated.

Separate inventories are compiled on the OS:

- unsuitable for use – completely worn out, damaged (the reason for unsuitability is indicated);

- rented and in safe custody (details of documents confirming rent, safe storage are indicated).

Postings for displaying the OS inventory: example

Below we offer a sample of exactly what write-offs that occur due to the fault of employees and as a result of breakdown should look like.

- table

| Dt | CT | Amount, thousand rubles | Rationale | Documentation |

| When there are no guilty parties | ||||

| 01 (select) | 01 | 53 | The original price of the machine is written off | Write-off act |

| 02 | 01 (select) | 15 | Depreciation costs | Buh. certificates |

| 94 | 01 (select) | 38 | Remainder price | |

| 91 | 94 | 30 | Losses after write-off | |

| When there are culprits | ||||

| 01 (select) | 01 | 350 | The original price of the car is written off | Write-off act |

| 02 | 01 | 250 | Depreciation costs | Buh. certificates |

| 94 | 01 (select) | 100 | Remainder price | |

| 73 | 94 | 100 | The shortages were attributed to the culprit E.S. Erokhin. | |

| 73 | 98,4 | 25 | Difference between residual and market price | |

| 70 | 73 | 125 | The cost of the car was withheld from the salaries of E.S. Erokhin. | |

Reflection in accounting of the results of inventory of fixed assets when unnecessary objects are detected

Unaccounted for fixed assets must be capitalized to account 01 in correspondence with the account for other income and expenses - 91. The cost of the object is assessed at current market prices at the time the surplus is identified. In these cases, inclusion in the OS is carried out in the same way as when purchasing property:

| Operations | D/t | K/t |

| Excess OS detected | 08 | 91/1 |

| Unaccounted for objects are included in the company's operating system | 01 | 08 |

Example:

As a result of checking the availability of OS at Ritm LLC, as of December 31, 2022, an unaccounted object was discovered - a leiter used for carrying out repair work on the contact network. The identified asset must be assessed at market value and accepted for accounting.

Leiter was made in the construction shop of the enterprise. At the time of the inspection, the cost of similar goods at current market prices (according to price lists of various manufacturing companies) amounted to 120,000 rubles. The service life of the facility is determined and approved by the protocol - 48 months. The accountant made the following entries in the accounting documents for December 2022:

| Operations | D/t | K/t | Sum |

| Income from capitalization of surplus fixed assets is taken into account | 08 | 91/1 | 120 000 |

| The object is included in the OS (basis - commissioning act, object assessment act) | 01 | 08 | 120 000 |

| From January 2022, monthly depreciation begins (120,000 / 48 months) | 02 | 01 | 2500 |

In tax accounting, the value of capitalized property is reflected in non-operating income.

Upon the fact of capitalization of surplus, VAT is not charged, since the object of taxation does not arise in this case, but the subsequent sale of the object by the enterprise - the tax payer is subject to VAT.

How to conduct an inventory of fixed assets: draw up an order

Each census begins with this document, which is prepared by the head of the organization. You can use the INV-22 form or create your own standard template for these purposes.

Certain points must be specified:

- Business name;

- the date on which the process will begin and end;

- who will be the chairman and members of the commission;

- how comprehensive the inspection will be (selective or complete);

- for what reason is it initiated;

- When should the documentation be submitted to the accounting department?

The executed order must be registered in the INV-23 journal, and then handed over to the chief inspector.

Before you start, you should check if you have:

- technical certificates for all objects;

- accounting cards;

- documents if the OS is leased.

The procedure for issuing an order to conduct an inventory of OS

Inventory begins with the manager issuing an order to conduct an inventory of fixed assets. To do this, you can use the INV-22 form, approved by Decree of the State Statistics Committee of Russia dated August 18, 1998 No. 88.

Download the order form in form INV-22.

The order specifies:

- location of the inventory;

- its start and end dates;

- chairman and members of the commission;

- degree of coverage of inventory objects;

- the reason for the inventory;

- deadlines for submitting documents to the accounting department.

The commission may include a chief or other responsible accountant, a person responsible for the safety of fixed assets, shop workers, administration employees, etc. The

order is registered in the inventory order register INV-23, approved by Resolution 88 and is handed over to the chairman of the commission for signature .

Download a sample order for inventory of fixed assets.

Before checking the actual availability and condition of fixed assets, it is necessary to review the availability of:

- OS inventory cards (form OS-6), other accounting registers for OS objects and the correctness of the data entered in them;

- technical passports;

- documents for receiving or leasing OS.

If necessary, accounting documents can be supplemented or adjusted.

Ready-made solutions for all areas

Stores

Mobility, accuracy and speed of counting goods on the sales floor and in the warehouse will allow you not to lose days of sales during inventory and when receiving goods.

To learn more

Warehouses

Speed up your warehouse employees' work with mobile automation. Eliminate errors in receiving, shipping, inventory and movement of goods forever.

To learn more

Marking

Mandatory labeling of goods is an opportunity for each organization to 100% exclude the acceptance of counterfeit goods into its warehouse and track the supply chain from the manufacturer.

To learn more

E-commerce

Speed, accuracy of acceptance and shipment of goods in the warehouse is the cornerstone in the E-commerce business. Start using modern, more efficient mobile tools.

To learn more

Institutions

Increase the accuracy of accounting for the organization’s property, the level of control over the safety and movement of each item. Mobile accounting will reduce the likelihood of theft and natural losses.

To learn more

Production

Increase the efficiency of your manufacturing enterprise by introducing mobile automation for inventory accounting.

To learn more

RFID

The first ready-made solution in Russia for tracking goods using RFID tags at each stage of the supply chain.

To learn more

EGAIS

Eliminate errors in comparing and reading excise duty stamps for alcoholic beverages using mobile accounting tools.

To learn more

Certification for partners

Obtaining certified Cleverence partner status will allow your company to reach a new level of problem solving at your clients’ enterprises.

To learn more

Inventory

Use modern mobile tools to carry out product inventory. Increase the speed and accuracy of your business process.

To learn more

Mobile automation

Use modern mobile tools to account for goods and fixed assets in your enterprise. Completely abandon accounting “on paper”.

Learn more Show all automation solutions

How to fill out a statement

How to make an inventory of fixed assets - count them and record all the different parameters. It is worth remembering that this is necessary not only to establish the correspondence of the number of units actually and according to plan. Other characteristics that must match the data on the card are also compared:

- performance;

- inventory numbers;

- what is it intended for;

- what it looks like externally, level of depreciation;

- presence/absence of defects.

When inspecting buildings, it is important to pay attention to:

- number of floors;

- year of construction;

- the material from which the room was built;

- total area and the share of useful space from it.

If a natural deposit is being studied, then its depth and probable length are of interest. For existing plants and trees, age and their presence on the site matter.

Why do you need a matching statement?

All this is recorded on a sheet, compared and approved. All detected deviations will be entered into accounting. This allows you to understand how much the enterprise in its reporting corresponds to what it actually is. You can work with up-to-date data and plan the further development of the organization.

Drawing up a statement of inventory

When conducting an inventory of fixed assets, not only their availability is checked, but also other important characteristics, such as:

- appointment,

- performance,

- inventory numbers,

- external condition,

- absence of any visible defects.

During the inspection of buildings, structures and other real estate objects, the following are checked:

- main building material,

- number of storeys,

- total and usable area,

- year of construction, etc.

Natural objects are checked: length, depth, extent.

By plantings - presence and age.

OSes of the same type received at the same time are indicated in the statement taking into account quantitative indicators.

All identified data is entered by members of the commission into the INV-1 inventory sheet, approved by Resolution 88, or an independently developed form.

How to draw up an act based on the results

We have discussed in what cases an inventory of fixed assets is carried out. It is important to decide in what cases the document is drawn up. It is issued when it is discovered that a certain object no longer meets the required characteristics or does not work properly. In some cases, a write-off is made because the material is not available due to mis-sorting, theft or damage.

You must specify:

- MOL;

- the composition of the commission that revealed the inaccuracy;

- dates of statements, their numbers, comparative inventory data;

- when the census was started and completed.

All papers are attached to it, which reflect the discrepancy between accounting and the real picture.

How to draw up the minutes that are drawn up at the final meeting

After the inventory is completed and all documents are filled out, the last council is assembled to sum up the results. A report on the work done is brought to the manager. This is not a mandatory process, but the record of its maintenance can become real evidence in court if a claim is filed for damage to the enterprise.

During the meeting, all changes, shortages, surpluses are read out, explanations from the MOL and expert opinions are listened to.

Finally, documentation is prepared that includes:

- results of the procedure performed;

- reasons why incorrect data was indicated in accounting;

- conclusions adopted by the commission;

- suggestions - how to eliminate all shortcomings and correct errors.

Everyone present signs it, then it is handed over to the manager so that he can make a final decision on all inaccuracies and inconsistencies.

Basic mistakes during inventory

There are several typical violations that many companies commit:

- an order appointing a commission is not drawn up;

- the UP did not specify the timing and order in which the inventory should be completed;

- hired an independent auditor who made errors in reporting;

- the order was filled out incorrectly - incorrect details, wrong full name;

- one of the inspectors was not present at the recount;

- everything was done only on paper, no actual calculations were carried out;

- violations were committed during weighing, measuring, etc.;

- the warehouse became accessible to everyone, and there was a risk of loss;

- A new MOT was chosen, but a census was not carried out before the old one left.

Results

We examined the procedure for conducting and organizing an inventory of fixed assets (FPE), studied the sequence of its stages and documentation. With the help of recalculation, it becomes possible to understand which assets are reflected correctly in the accounts and which ones are not. We recommend that you carry out timely monitoring and complete postings. This is important for any enterprise, since without inspections it is impossible to determine the actual availability and shortage of objects, and this can result in problems, including with the tax service.

Documents for download:

Number of impressions: 9356