A standard operation for every accountant, repeated monthly, is summing up financial results for the past period. However, in the process of aggregating income and expenses, difficulties often arise due to both the specifics of the 1C software product and the lack of skills that allow both to avoid technical errors and to eliminate them when identified. At first glance, the algorithm seems simple and understandable, but in order to implement it efficiently and effectively, you need to clearly understand how accounts are closed at the end of the month. Let's look at clear examples of how exactly this process occurs, what the nuances are, and what needs to be taken into account when performing standard operations.

General idea of what it's for

From a technical point of view, closure is a specific algorithm implemented by the user using program tools. The goal is to combine costs and income, and the result obtained is used to assess the organization’s performance in the reporting time interval. Throughout the month, the accountant uses 1C to record individual events related to the conduct of administrative, economic and commercial activities, while at the end of the period it is necessary to generate a list of settlement entries reflected in the accounting registers:

- Depreciation charges for fixed assets and intangible assets.

- Compensation for the costs of purchasing workwear and equipment.

- Write-off of upcoming and distribution of indirect expenses.

- Calculation and change of the actual cost of goods or services produced.

- Summing up financial results, as well as other operations.

Which accounts are closed in accounting when closing at the end of the month, and how exactly? First of all, it is important to take into account that in the case of each individual enterprise, the list is formed individually. Thus, for organizations that do not use the simplified taxation system, there is no need to implement standard regulations that determine the procedure for calculating expenses that meet the goals of the simplified tax system. If there is no retail sale of products, there is no reason to calculate trade margins.

According to generally accepted practice, the list of operations is determined based on factors such as:

- Accounting parameters settings used by a legal entity.

- Features of the accounting policy relevant for the reporting period.

- A set of information entered into the program before the start of the procedure.

Speaking about why you need to close the month in trading, and what to pay attention to when preparing transactions, it should be noted that experts recommend adhering to the standard algorithm before filling out each significant report. It doesn’t matter whether data is submitted on insurance premiums, personal income taxes, or a simplified taxation system declaration - by “counting” the period, the accountant gets the opportunity to identify key errors that can distort the indicators.

Closing the month in accounting. A good example

Greetings! Today we will look at the process of “closing the month” for a real company providing services.

We'll see how our accounting theory works in practice.

At the same time, let’s once again learn to “look at the turns.” According to the basics of accounting theory and our new knowledge, let's try to predict what we should see after the “closing of the month.”

For clarity, let’s take as a basis the Turnover Balance Sheet (TSV) of our enterprise. Here is an example of OSV. Is this not what we expect to see?

- Some amounts should appear in the Turnovers for the period for account 99

- Accounts 90 and 91 must be without balance

- Account 26 should have no balance at the end of the month. those. BalanceEndingDebit(SKD) = 0

Let's see how our turnover has changed.

I'll comment a little. Look, account 26 at the end of the month was “closed” - it became 0. This is good. Here's a log of the wiring showing how it happened.

As we can see, expense accounts “transfer” their accumulated amounts from their Credit to Debit account to the financial result account. Remember the financial result formula?

What accounts are involved? So, Debit 90 and 91 accounts collect the expenses of our company for the current month. Now we can calculate the financial result for each of them. Calculating the financial result is some kind of action on 90, 91 accounts.

As you remember, accounts 90 and 91 after summing up the financial result should be equal to 0. And the final result of financial activity will be on account 99.

Zero balances for accounts 90 and 91 should be for the account as a whole. Sub-accounts of these accounts will have balances until December 31, pending the procedure - balance reformation. But more on that later. This is how the situation looks in our SALT for accounts 90, 91 and 99. This situation arises after the “transfer” of expenses to account 90, BUT before closing 90, 91.

Look, I have highlighted key accounts from the entire SALT to show the intermediate stage of “closing the month”. We see that account 26 has been closed: its balances are zero.

And, in our case, the amount of account 26 was displayed in the Debit of account 90. In our example, the company has only account 26.

Main stages

The summing up algorithm includes the following stages:

- Calculating costs and writing them off to cost.

- Carrying out sales positions and determining financial results;

- Posting income and expense items with subsequent calculation of the tax base.

These actions are implemented sequentially and make it possible to cover the entire list of operations performed by the organization during the reporting time period.

Step 1: Identify your monthly expenses

When determining which expense accounts should be closed at the end of the month, when closing the period, you should take into account all active categories that are in one way or another related to the activities of the enterprise. As a rule, the list includes main and auxiliary production expenses, general business expenses, payment of wages to employees, payment for supplies necessary to maintain the carryover balance, etc.

As a clear example of accounting, the following procedure for recording transactions can be given. Thus, the performance indicators of FCSM LLC for December 2022 were:

- depreciation charges - 125,000 rubles;

- staff salaries - 930 thousand;

- payments to management - 330,000 rubles;

- electricity costs - 35,000 excluding VAT;

- sales of products - 1.062 million rubles, including tax of 162,000.

Accordingly, to close accounting accounts at the end of the month, the following entries are made manually:

| D | TO | Description | Amount, thousand rubles | Document |

| 20 | 02 | Depreciation | 125 | Accounting information |

| 20 | 70 | Salary | 930 | |

| 26 | 70 | Management payments | 330 | |

| 20 | 60 | Payment to the electricity supplier | 35 | Invoice |

When reflecting revenue, the structure looks like this:

| D | TO | Operation | Sum., t.r. | Document |

| 62 | 90.1 | Revenue | 1062 | Invoice, act of sale |

| 90 | 68 | Value added tax | 162 | Invoice |

| 90.2 | 41 | Product cost | 350 | Invoice |

Step 2: Determine production costs

In this case, one of two methods can be used:

- Classic write-off of costs - provides for the optional use of debit and credit 40 at accounting prices.

- Direct costing excludes general business expenses from the final structure, writing them off as the organization’s revenue.

The choice of methodology depends on the independent decision of the enterprise, and is enshrined in the basic rules.

Let's look at how to close cost accounts in accounting, based on the data from the example given earlier. Within the traditional method, entries reflecting the closure of cost items by actually writing them off as direct expenses look like this:

| D | TO | Operation | Sum, thousand rubles | Document |

| 20 | 26 | Production costs | 330 | B/s |

| 90.2 | 20 | Closing at cost (330+125+930+35) | 1420 |

When writing off through direct costing:

| D | TO | Expenses | Amount, t.r. | Document |

| 90.8 | 26 | General economic | 330 | B/s |

| 90.2 | 20 | Production (125+930+35) | 1090 |

Closing account 90:

| D | TO | Description | Sum, thousand rubles | Document |

| 90.9 | 90.2 | Expenses (1420+1090+350+162) | 3022 | B/s |

| 90.1 | 90.9 | Receipts | 1 062 |

Step 3. Determining the financial result

The final assessment for the reporting period involves comparing the turnover values for the sales and income-expense accounts (90 and 91, respectively), as well as the subsequent transfer of the balance to Profit and Loss (account 99).

The resulting indicator is formed based on:

- Results of the main and related activities.

- Costs associated with emergency situations.

- Tax payments.

The active-passive specificity of the article determines the fact that it corresponds with several accounts at once:

- 90 - when determining the basic financial result;

- 91 — for generating results for other activities;

- 68 - when calculating income tax.

In the case of reporting on emergency expenses, a comparison is made with accounting sections used to reflect monetary assets, material assets, mutual settlements with employees, etc.

Closing transactions on accounts 90, 91, 99 at the end of the month

Within the subaccounts of the first two specified items, which belong to both the active and passive categories, by the end of the period a resulting indicator is accumulated, which is a consequence of the economic activities of the organization.

To calculate the total, a method is used to compare debit and credit turnovers - in situations where the first value is higher than the second, K90.9 is used for reflection, since at the time of completion there should be no balances on account 90. Returning to the above example, the following structure would be used for the design:

| D | TO | Description | Amount, t.r. | Document |

| 99 | 90.9 | Reflection of loss (3022—1062) | 1 960 | Accounting information |

The results for 91 are calculated in a similar way. After this, the balances for both items should be reflected in account 99, used to demonstrate the cumulative total, and subject to annual closure, which is carried out on the last day of the reporting time interval.

| D | TO | Operation |

| 90.9 | 99 | Profit main |

| 99 | 90.9 | Loss main |

| 91.9 | 99 | Profit etc. |

| 99 | 91.9 | Loss, etc. |

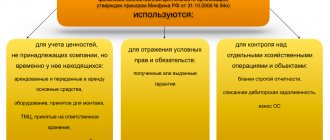

Which accounts should be closed at the end of the month?

» Content without using subaccounts.

I did this to make it easier to understand.

When the meaning of the “closing the month” process is clear, then it will be possible to look at SALT with subaccounts.

First, collect the Expenses of the current month on the corresponding accounts (20, 25, 26, 44) and “transfer” them to the “Expense subaccounts” 90 and 91 accounts. Secondly, as a result of transferring amounts from expense accounts (20, 25, 26, 44), the ending balances on these expense accounts will become equal to 0. There are exceptions here. For example, for production, especially for agricultural producers whose products grow and affect several months, account 20 will not close completely, i.e.

the balance will not be 0. Another example would be trading organizations that, in account 44, take into account transportation costs for delivering goods to them. We'll talk about these small exceptions later.

Now the main thing is to understand the essence - expense accounts when “closing the month” are closed to zero, i.e. there should be no balances on them at the end of the month. (unless there are exceptions) Thirdly, after transferring amounts from expense accounts to account 90, we calculate the ending balances for each account: accounts 90 and 91.

In other words, we find the difference between Debit and Credit for accounts 90 and 91 and transfer the resulting amount for each account to account 99.

As a result, accounts 90 and 91, their final balances, will also become equal to 0. When closing the month, there should be no balances on the Expense accounts (20, 25, 26, 44).

And 90 and 91 accounts, in general, should also be equal to 0, i.e.

have no leftovers. Once again, I note that there are small exceptions when it is allowed for Expense Accounts to have a balance after the “closing of the month.” This applies to two common accounts: 20 production and 44 accounts. More on this another time. In the next article we will look at the process of “closing the month” for the company whose SALT we considered.

General stages of the procedure for closing accounts when preparing interim and annual financial statements Stage 1 Write-off of the cost of work (services) from account 23

Ready-made solutions for all areas

Stores

Mobility, accuracy and speed of counting goods on the sales floor and in the warehouse will allow you not to lose days of sales during inventory and when receiving goods.

To learn more

Warehouses

Speed up your warehouse employees' work with mobile automation. Eliminate errors in receiving, shipping, inventory and movement of goods forever.

To learn more

Marking

Mandatory labeling of goods is an opportunity for each organization to 100% exclude the acceptance of counterfeit goods into its warehouse and track the supply chain from the manufacturer.

To learn more

E-commerce

Speed, accuracy of acceptance and shipment of goods in the warehouse is the cornerstone in the E-commerce business. Start using modern, more efficient mobile tools.

To learn more

Institutions

Increase the accuracy of accounting for the organization’s property, the level of control over the safety and movement of each item. Mobile accounting will reduce the likelihood of theft and natural losses.

To learn more

Production

Increase the efficiency of your manufacturing enterprise by introducing mobile automation for inventory accounting.

To learn more

RFID

The first ready-made solution in Russia for tracking goods using RFID tags at each stage of the supply chain.

To learn more

EGAIS

Eliminate errors in comparing and reading excise duty stamps for alcoholic beverages using mobile accounting tools.

To learn more

Certification for partners

Obtaining certified Cleverence partner status will allow your company to reach a new level of problem solving at your clients’ enterprises.

To learn more

Inventory

Use modern mobile tools to carry out product inventory. Increase the speed and accuracy of your business process.

To learn more

Mobile automation

Use modern mobile tools to account for goods and fixed assets in your enterprise. Completely abandon accounting “on paper”.

Learn more Show all automation solutions

Working with cost items

Within the framework of the 1C: Accounting software product, standard processing intended to perform the procedure in question is placed in the “Operations” section and combines several sequentially implemented algorithms. The result of the launch is the financial indicator formed as a result of the operation of the enterprise. At the same time, the third block of the cycle contains a set of integrated regulations that determine which cost accounting accounts are closed monthly.

Registration of account 20 "Main production"

If there are certain factors, such as lack of sales revenue or incomplete production processes, it is considered normal to leave this item unclosed before the end of the month. In cases where the operation is nevertheless implemented, it can correspond both with 90.02 and 90.08 (with a profile focused on the provision of services) and with 43 (if goods are released, ultimately reflected on 90.02 after their actual sale). The distribution directly depends on the settings set for the list of direct expenses, item “Taxes and reports”).

It is worth noting that, within the framework of the legislative provisions enshrined in the Tax Code, there is no accurate expense register that would be universal for any organization. When you first click the link, the system automatically prompts you to fill out the specified section in accordance with the regulations defined in Art. 318 NK. Having completed the necessary actions, you should re-check which accounts should be closed when closing the month for expenses (direct - 90.02, indirect - 90.08), and, if necessary, make current adjustments.

Registration of account 26 “General business expenses”

The article is used to reflect the expenses of an enterprise that are not actually related to production processes and arise in connection with the implementation of administrative and management activities. That is, in this case we are talking about rent, depreciation of office equipment, salaries of accounting department employees, etc. In this case, a prerequisite is compliance with the principle in which, at the end of the period, costs are included in financial results, and the final balance becomes zero.

To close account 26, the already mentioned direct costing method is used in accounting (inclusion in the cost of sales in account 90). It is also allowed to separate into 20, 23 and 29 articles, that is, actual integration into the structure of the primary cost of goods manufactured, work performed or services rendered.

Setting up the method in the software product is located in the “Main” section, “Accounting Policy” item. For businesses that choose not to use a direct costing approach, it is mandatory during the installation process to click on the Allocation Methods link, specifying that indirect costs should be allocated to the manufacturing category.

To understand the specifics of accounting for account 26 within the framework of tax accounting, it is enough to use the “Types” column, available in the “Cost Items” reference section. So, for example, if one of the types is marked as not being included in the general structure, it will also not be reflected in the income tax return. In this case, cost categories related to the “Insurance premiums” type are indicated on page 041 of the second appendix of Sheet 02, and “Material” items increase the final total value of page 040.

Closing the account 44 “Sales expenses”

In this case, we are talking about costs that are somehow related to the sale of the product. These include payment for rent of commercial space, advertising investments, salaries of managers, etc. The 1C: Accounting configuration provides for automatic posting to 90.07, that is, determination as commercial costs.

The software product is configured by default and does not require additional configuration on the part of the user, however, at the end of the period it may turn out that after completing the cycle there is still a balance on the account. Such situations are associated with the presence of regulated expenses - usually of a representative, transport or advertising nature.

Closing the account 25 “General production expenses”

When considering the specifics of account 26, it was already mentioned that it can either be distributed or completely written off according to 90.08. In turn, the cost item used to differentiate losses associated with the maintenance of main and auxiliary production resources provides only for distribution, the order of which is determined based on the criteria of accounting policy. As a rule, its use is determined by the scale of the enterprise structure, that is, the number of divisions and business processes.

Let's look at a clear example of cost allocation, relevant for account 25. Let us assume that the operating activities of the organization in the reporting period led to the formation of the following types of expenses:

- Staff salary is 100 thousand rubles.

- The rent for the use of the production premises is 150 thousand.

- Depreciation charges for equipment - 50 thousand rubles.

Thus, the total general production expenses amount to 200,000 rubles. In a situation where an enterprise has chosen an accounting policy according to which distribution is carried out directly among divisions, the actual indicators of each of them are applied. If department No. 1 had expenses of 75, and No. 2 - 90, that is, the total amount is 165 thousand rubles, the method of calculating the proportional ratio is used. In the first case, it turns out 75/165x100 = 45%, therefore, the second accounts for 55%. Based on this, all that remains is to spread the total expenditure amount, which will be 90 (200 * 45%) and 110 (200 * 55%) thousand rubles, respectively.

Tips for closing the month in Enterprise Accounting 2.0

In this article, we will pay special attention to preparing for the closing of the month, the closing procedure itself, consider the most common errors and ways to solve them, and also get acquainted with the various services and reports provided by the 1C: Enterprise Accounting 8 program, edition 2.0. To begin with, before closing the year or month, we need to make sure that everything in our accounting is correct, all transactions are reflected correctly, and we have not forgotten anything. It would not be amiss at the end of the year, and sometimes even the month (depending on our accounting policies and the specifics of the organization’s activities), to carry out an inventory in order to know for sure what we will have in balance at the beginning of the new year.

Please note that the document inventory of goods in a warehouse carries out an inventory separately for each warehouse.

And if our organization has several warehouses, then there should be several inventory documents, corresponding to the number of warehouses.

The accounting quantity column is filled in based on the balances according to accounting data, i.e. shows the amount that we have left after the transactions are reflected in the system documents. In the actual quantity column, we can indicate the quantity of each item that is physically available in warehouses.

Based on the inventory document, documents for the receipt of goods can be entered if the actual quantity of the item exceeds the accounting quantity. A posting document will be generated automatically based on the excess amount. Any surplus will be charged to other income.

Also, based on the inventory document, the document write-off of goods can be entered; the document will also be filled out automatically if the accounting quantity exceeds the actual one. All shortages will be attributed to 94 “shortages and losses of valuables.”

After we have counted all our property, we can move on to checking the accuracy of the accounting. For these purposes, the 1C program offers us to use an express check of accounting (“Reports – Express check of accounting”).