What are they punished for?

A fine is one of the types of sanctions applied by tax authorities to violators of legislation on taxes and fees. Responsibility for committing tax offenses is established in Chapter 16 of the Tax Code of the Russian Federation. The most frequently applied fines by the inspectorate are shown in the table below:

| Type of violation | Amount of fine | Article of the Tax Code of the Russian Federation |

| Conducting business activities without registration | 10% of income received from illegal business activities, but not less than 40,000 rubles. | 116 p. 2 |

| Submitting an application for registration with the Federal Tax Service in violation of the deadline | 10,000 rub. | 116 paragraph 1 |

| Failure to submit a declaration | 5% of the unpaid tax amount for each month before the date of actual submission of the declaration. The maximum fine is 30% of the above amount, the minimum is 1000 rubles. | 119 |

| Violation of the reporting procedure (submitting a paper report instead of an electronic one) | 200 rub. | 119.1 |

| Gross violation of accounting rules | During one tax period - 10,000 rubles. More than one period - 30,000 rubles. If the violation led to an underestimation of the tax base - 20% of the amount of arrears, but not less than 40,000 rubles. | 120 |

| Non-payment of tax as a result of underestimation of the tax base or other incorrect calculation | By negligence - 20% arrears. Intentionally - 40% of arrears | 122 |

| Failure to fulfill the duties of a tax agent (for example, failure to withhold or transfer personal income tax to the budget) | 20% of the amount to be withheld or transferred | 123 |

| Failure to provide documents or information about taxpayers at the request of the Federal Tax Service | 10,000 rub. | 126 |

New practice of the Armed Forces to reduce penalties

On May 14, 2022, the Supreme Court of the Russian Federation put an end to a long-term discussion about the admissibility of protecting civil rights by filing independent claims to reduce penalties by debtors.

In recent years, unscrupulous creditors, knowing the practice of courts applying the provisions of the Civil Code of the Russian Federation on reducing penalties disproportionate to the consequences of violation of obligations at the request of the defendant in a dispute, have created a new way of abusing the right in the form of charging inflated penalties, without filing corresponding claims in the courts.

The calculation of the creditors with such abuse was that the debtors would not be able to take advantage of Art. 333 of the Civil Code of the Russian Federation, and will be forced to pay such “draconian” penalties.

Some clarity in matters of protecting the rights of debtors was brought by Resolution of the Plenum of the Supreme Court of the Russian Federation dated March 24, 2016 No. 7 “On the application by courts of certain provisions of the Civil Code of the Russian Federation on liability for violation of obligations” (hereinafter referred to as Resolution of the Plenum No. 7), providing for the possibility for the debtor go to court with an independent claim to reduce the penalty (clause 79).

An analysis of numerous judicial practices in this category of disputes has shown polar conclusions of courts in disputes with identical circumstances.

In all the cases examined, before filing independent demands, the debtors did not deposit funds into the creditors’ accounts to pay penalties.

At the same time, on the one hand, the courts believed that filing an independent claim to reduce the penalty at the request of the debtor is an appropriate way to protect the right, since the rules of Article 333 of the Civil Code of the Russian Federation directly provide for the right of the court to reduce the payable penalty in the event of its obvious disproportion to the consequences of violation of the obligation.

In opposite examples, the courts pointed to the need to prove the forced write-off of the penalty or its involuntary payment, and some courts believed that going to court with an independent claim to reduce the penalty is, in principle, not an appropriate way to protect the right, since the application of Art. 333 of the Civil Code of the Russian Federation is possible only at the request of the debtor in the status of a defendant.

The Supreme Court of the Russian Federation considered the cassation appeal of AlexGroup LLC in case A40-293311/2018, where the debtor went to court with a demand to reduce the fine in the amount of the annual rent - 1,258,639.80 rubles, imposed by the Department of City Property of the city of Moscow for placement of a payment terminal per 1 sq.m of rented premises.

The court of first instance reduced the amount of the fine 10 times to 125,863 rubles. The appellate court, citing the choice of an improper method of protecting the right, overturned the decision and dismissed the claim. The Court of Cassation upheld the appeal ruling.

At the court hearing, representatives of the plaintiff - Lyashchevsky B.I. and Medushevskaya T.V., in support of the arguments of the cassation appeal, drew the attention of the Judicial Panel to the fact that from the literal interpretation of Art. 333 of the Civil Code of the Russian Federation it follows that we are talking about the court’s right to reduce a clearly disproportionate penalty.

Provisions of Art. 333 of the Civil Code of the Russian Federation does not make the exercise of the debtor’s right to apply for a reduction of the penalty dependent on its write-off, offset or payment in an involuntary manner due to the dominant position of the creditor.

This norm does not establish requirements for the procedural status of the debtor for an application to reduce the penalty. those. the debtor does not have to be in the status of a defendant.

A systematic analysis of judicial practice shows that the explanations in paragraph 79 do not prevent the court from exercising the right to reduce the penalty.

The debtor's exercise of the right to reduce penalties under an agreement to which the dominant entity is a party before actual payment:

- speaks of the debtor’s intention to fulfill accepted obligations, taking into account the balance of interests of the parties;

— meets the interests of the weaker party to the contract;

— contributes to achieving the goals of the President’s program to support small and medium-sized businesses.

In addition, it eliminates the need to:

— carrying out financial transactions for the debtor to pay the amount of the penalty (until its amount is determined by the court),

— recalculation by the creditor of already credited amounts of the penalty after reducing its amount in court, reconciliation of mutual settlements,

— operations to return overpaid funds.

The essence of the objections of representatives of the Department of City Property boiled down to the position that it was illegal to reduce the penalty when the parties established a condition on the specific amount of the penalty in the contract and to the fact that legal entities are free to enter into an agreement.

Based on the results of consideration of the plaintiff’s cassation appeal, the Supreme Court of the Russian Federation canceled the decisions of the courts of appeal and cassation, and upheld the decision of the Moscow Arbitration Court.

In support of its conclusions, the Supreme Court of the Russian Federation, in a ruling dated May 20, 2022 in case No. A40-293311/2018, indicated that the protection of civil rights is carried out in various ways, the list of which is not exhaustive (Article 12 of the Civil Code of the Russian Federation).

According to the explanations of Plenum No. 7, it is possible for the debtor to independently apply to the court with a request to reduce the amount of the penalty in certain cases, the list of which in the said resolution (as the court of first instance correctly indicated) is not exhaustive, since the law does not contain a direct prohibition on the debtor filing a claim with the creditor such a requirement.

A similar legal position is given in paragraph 17 of the Review of judicial practice in cases related to the protection of the rights of consumers of financial services, approved by the Presidium of the Supreme Court of the Russian Federation on September 27, 2017.

This method of protection is aimed at establishing legal certainty in the relationship between the parties to the obligation regarding the amount of the payable penalty (fine), the initial amount of which the debtor considers excessive.

The Constitutional Court of the Russian Federation, in its ruling dated December 21, 2000 No. 263-O, indicated that the opportunity given to the court to reduce the amount of the penalty if it is excessive compared to the consequences of violation of obligations is one of the legal methods provided for in the law, which are aimed against abuse of the right of free determination the amount of the penalty, that is, in essence, to implement the requirement of Article 17 (Part 3) of the Constitution of the Russian Federation, according to which the exercise of human and civil rights and freedoms should not violate the rights and freedoms of other persons. That is why Part 1 of Article 333 of the Civil Code of the Russian Federation is not about the right of the court, but, in essence, about its obligation to establish a balance between the measure of responsibility applied to the violator and the assessment of the actual (and not possible) amount of damage caused as a result of a specific offense.

The determination by the court of first instance of the specific amount of the penalty in accordance with the provisions of Article 333 of the Civil Code of the Russian Federation is not in itself a violation of substantive law.

It should be noted that disputes over penalties make up a significant percentage in the structure of court cases and uniformity in law enforcement practice is an important condition for maintaining the stability of civil turnover.

According to statistical data of the Supreme Court of the Russian Federation by category of cases for 2022, 188,787 disputes regarding penalties in the amount of 143,743,816,000 rubles were considered. Of these, 164,165 are satisfied.

In this regard, a restrictive interpretation of the freedom of judicial discretion regarding the application of Art. 333 of the Civil Code of the Russian Federation creates extremely negative preconditions for the stability of civil circulation in general.

For this reason, the importance of the dispute under consideration lies in the fact that it was based on its results that the Supreme Court of the Russian Federation for the first time clearly and unambiguously indicated the existence of the debtor’s substantive right to claim.

Thus, the legal position of the Supreme Court of the Russian Federation in case No. A40-293311/2018, which established a tool for protection against unscrupulous creditors, acquires particular significance and indicates a positive shift in judicial practice.

***

Authors of the article:

Sukhov Alexey Vasilievich – Managing partner of the legal

Lyashchevsky Boris Igorevich – Head of the department of judicial and claims work of legal

Types of mitigating circumstances

If the fine is applied lawfully, and the taxpayer agrees that he has violated the legislation on taxes and fees, it will have to be paid to the budget. When deciding whether to prosecute, the Federal Tax Service always applies the maximum possible punishment. But it can be easily reduced if there are mitigating circumstances to reduce the tax fine, which include:

- committing an offense for the first time;

- admission of guilt and repentance;

- absence of malicious intent;

- difficult financial situation of the company (large accounts payable, pre-bankruptcy);

- social significance of the organization’s activities in the field of construction, housing and communal services, healthcare, etc.;

- status of a budgetary institution;

- slight delay in reporting due to technical problems;

- no damage to the budget (for example, the declaration was not submitted on time, but the tax was paid on time and in full);

- independent identification and correction of errors in accounting and tax calculation;

- a significant volume of requested documents, and the taxpayer is forced to take active measures to extend the deadline for submission;

- lack of requested documents as a result of their destruction (for example, in a fire);

- If the punishment is imposed on an individual entrepreneur or another individual, then a serious illness, disability, the presence of dependent children, etc. are recognized as a mitigating circumstance.

Not only the tax office, but also the court can cancel or reduce the fine. Use the free instructions from ConsultantPlus to achieve justice.

Mitigating circumstances (Article 112 of the Tax Code of the Russian Federation)

During the consideration of the audit materials or if other violations are detected, the tax authority must establish the presence of mitigating circumstances (subclause 4, clause 5, article 101, subclause 4, clause 7, article 101.4 of the Tax Code of the Russian Federation) and take them into account when imposing a fine. If there are mitigating circumstances, the amount of the fine may be reduced by at least 2 times compared to the amount provided for in the corresponding article of the Tax Code of the Russian Federation. This is directly indicated in paragraph 3 of Art. 114 Tax Code of the Russian Federation. According to paragraph 1 of Art. 112 of the Tax Code of the Russian Federation the following circumstances are recognized:

- committing an offense due to a combination of difficult personal or family circumstances;

- committing an offense under the influence of threat or coercion or due to financial, official or other dependence;

- difficult financial situation of an individual held accountable for committing a tax offense;

- other circumstances that may be recognized as mitigating by the court or tax authority considering the case.

If the tax authority did not take into account mitigating circumstances in order to reduce the fine in the act or, in the opinion of the taxpayer, they were not taken into account in full, you can apply to take into account mitigating circumstances and reduce the amount of the fine. The application must be submitted to the tax authority within a month from the date of receipt of the on-site or desk audit report (clause 6 of Article 100 of the Tax Code of the Russian Federation) or the report of an identified offense (clause 5 of Article 101.4 of the Tax Code of the Russian Federation).

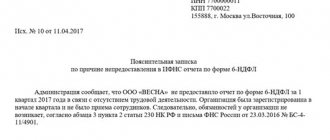

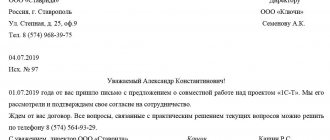

Sample petition to take into account mitigating circumstances and reduce the fine.

IMPORTANT! In paragraph 3 of Art. 114 of the Tax Code of the Russian Federation speaks only of the minimum limit for reducing sanctions. If the taxpayer does not agree with the amount of the fine imposed, he has the right to go to court. The Plenum of the Supreme Arbitration Court of the Russian Federation, in paragraph 16 of Resolution No. 57 of July 30, 2013, indicated that the court has the right to reduce the fine by more than 2 times.

When considering the case, the court will also examine the circumstances that the tax authority has already assessed at the stage of pre-trial appeal. And if he deems it necessary, he will reduce the fine again (letter of the Federal Tax Service of Russia dated August 22, 2014 No. SA-4-7/16692).

This means that in court it makes sense to declare all circumstances that seem to be mitigating, regardless of whether the tax authority took them into account when setting the fine or not.

You can read more about judicial practice on this issue in our material “Will the court reduce the fine by more than half if the tax authorities have already taken into account mitigating circumstances when imposing the punishment?” .

The court will make a decision about what other circumstances can be considered mitigating based on its internal conviction, which is based on an assessment of the evidence presented (Article 71 of the Arbitration Procedure Code of the Russian Federation). Different courts may evaluate the same circumstance differently, but an analysis of arbitration practice allows us to identify frequently occurring mitigating circumstances.

Procedure for drawing up applications

Initially, a petition for mitigating circumstances to the tax office is submitted to the inspectorate that imposed it. A little time is allotted for its submission:

- 30 working days from the date of receipt of the inspection report, if penalties were imposed based on the results of an on-site or desk inspection (clause 6 of Article 100 of the Tax Code of the Russian Federation);

- one month from the date of receipt of the act of discovery of a violation of the law, if it was detected outside the scope of the audit.

The petition should include all mitigating circumstances that the company has. Usually at this stage it is possible to reduce the size of sanctions.

If an organization has submitted a petition to the tax office to reduce the fine for late submission, but the Federal Tax Service Inspectorate has not responded to it in any way, then it should contact the Federal Tax Service. To do this, a complaint is drawn up to a higher authority, which lists all the circumstances that were not taken into account when the inspectorate made a decision, mitigating the company’s guilt. If the Federal Tax Service does not reduce the amount or reduces it slightly, then it is permissible to challenge the amount of sanctions in court.

Regardless of where you decide to apply, look at a few rules on how to write a petition to the tax office to reduce the fine, and a sample of such a document.

When drawing up an application, you must indicate:

- name of the tax authority;

- the person from whom the application is submitted;

- circumstances as a result of which penalties were imposed;

- details of the violation detection report;

- circumstances on the basis of which a request for a reduction in penalties is made.

Example of a petition to the Federal Tax Service:

Deadline for submitting a request to cancel a fine to the tax office

A letter requesting a reduction in tax penalties or their cancellation must be drawn up and sent within the prescribed period. This period is the same, regardless of how the tax offense was detected:

- if a tax audit was carried out (desk or on-site), the period is 1 month from the date of receipt of the audit report by the taxpayer (clause 6 of Article 100 of the Tax Code of the Russian Federation);

- in other cases – 1 month from the date of receipt of the Federal Tax Service Inspectorate’s report on the tax offense (clause 5 of Article 101.4 of the Tax Code of the Russian Federation).

How to cancel a fine

If the taxpayer is sure that the punishment imposed by the regulatory authority is unlawful, he has the right to challenge it by filing an objection to the tax authority’s act within the same time frame as the petition for mitigation of sanctions. If the objections are not taken into account and the decision to collect a fine is nevertheless made, then the taxpayer has the opportunity to contact the Federal Tax Service with a complaint about the actions of the Federal Tax Service or with a petition to review the decision. According to its consideration by the Federal Tax Service:

- or will satisfy the taxpayer’s demands for the lifting of sanctions;

- or refuse to satisfy the taxpayer’s demands and leave the decisions of the Federal Tax Service in force.

If the decision of the Federal Tax Service does not suit you, then your only option is to file a claim with the arbitration court to cancel the decision of the lower body.

When drawing up an objection to an act, you must indicate:

- details of the Federal Tax Service;

- details of the person from whom the application is being submitted;

- details of the violation detection report;

- circumstances on the basis of which the taxpayer considers the imposition of penalties illegal.

To submit such a petition, we recommend using the form provided by the Federal Tax Service on the official website in the section “Submitting objections to tax audit reports.”

An objection to the PFR inspection report is also prepared in a similar way. The only difference: the legislation on personalized accounting does not stipulate mitigating circumstances. Therefore, the Pension Fund does not have the ability to cancel or reduce sanctions already imposed; this will have to be done exclusively through the courts.

Who identifies mitigating circumstances and how?

The head of the inspection must determine for himself whether there are mitigating circumstances when considering the act in which the violation is recorded. But it will be better if the company sends a petition to the tax office and declares mitigating circumstances, because the tax office does not always have such information. For example, the difficult financial situation of the company may become a mitigating circumstance. But, if the inspectorate is not informed about this situation, it itself most likely will not establish this.

We talked about how you can reduce the tax penalty in an episode of the Accountant Live program.