About the salary insurance premium calculator

The payroll insurance premium calculator is designed largely to make the work of accountants easier. The calculator will significantly reduce the time spent on calculating insurance premiums and will allow the accountant to avoid mistakes, which, in turn, can lead to the accrual of penalties, penalties and the need to correct statements.

Calculating insurance premiums is a painstaking task that takes into account many variables.

It will be necessary to take into account the total amount of remuneration, the taxable base, and periods of incapacity for work.

The calculator will be equally useful for employees who want to check the correctness of deductions from their salaries.

Employers pay four types of insurance contributions for their employees:

- In the Pension Fund of Russia;

- to the health insurance fund;

- to the social insurance fund. Contributions to the Social Insurance Fund are divided into contributions in case of disability and contributions for industrial accidents and occupational diseases.

The transfer occurs by deducting the amounts of contributions from the salaries of employees. So, in accordance with Art. 419 Tax Code of the Russian Federation:

- employer - organization or individual entrepreneur, deduct insurance premiums from employees' wages or from remuneration under civil contracts);

- individual entrepreneurs, notaries, lawyers, appraisers and other individuals transfer insurance premiums for themselves.

The amount of insurance premiums is determined based on the taxable base, that is, the totality of all remunerations received by the employee, including remunerations for work performed under civil contracts.

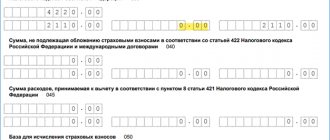

In accordance with Art. 422 of the Tax Code of the Russian Federation, the totality of remuneration, that is, the taxable base, can be reduced by excluding from it:

- benefits for certificates of incapacity for work;

- maternity benefits;

- benefits assigned to care for a child up to one and a half years old;

- provided material assistance in the amount of up to 4 thousand rubles;

- payments upon dismissal, with the exception of the amount of compensation for unused vacation.

By Decree No. 1378 of the Government of the Russian Federation of November 15, 2022, the following maximum base values for calculating insurance premiums were established for payers of insurance premiums:

- 912,000 rubles when calculating contributions for compulsory social insurance;

- 1,292,000 rubles for compulsory pension insurance.

The maximum base for health insurance contributions has been abolished since 2015.

If the employee's total remuneration exceeds the base limit, then:

- the employee is not accrued contributions to OSS in the event of temporary disability and in connection with maternity;

- Contributions to the Pension Fund are charged at a rate of 10%.

In accordance with Art. 426 of the Tax Code of the Russian Federation, employers calculate insurance premiums at the following rates:

- 22% within the established base value;

- 10% – if the amount of remuneration exceeds the limit;

- 2.9% in the Social Insurance Fund in case of temporary disability and in connection with maternity, if the total remuneration is less than or equal to the maximum base value;

- 5.1% for compulsory medical insurance.

In total, the amount of insurance payments for most payers is 30% of the total compensation.

Reducing insurance premiums - rate values

The total rate of insurance premiums regulated by the Tax Code of the Russian Federation is 30%. At the same time, it is divided:

- by 22% - for contributions to compulsory pension insurance (OPI);

- 5.1% - for contributions to compulsory health insurance (CHI);

- 2.9% - for contributions in case of temporary disability and in connection with maternity (VNiM).

Note! Contributions for accident insurance are subject to the provisions of Federal Law dated July 24, 1998 No. 125-FZ. The changes currently being adopted do not affect this normative act.

The reduction of insurance premiums to 15% is expressed at the following rates:

- 10% - for OPS;

- 5% - for compulsory medical insurance;

- 0% - at VNiM.

Reduced rates may not apply to the entire amount of income accrued in favor of an individual. For the amount of remuneration for the month within the established minimum wage, contributions will have to be calculated in the same manner, i.e. at rates of 22%, 5.1% and 2.9%. Reduced rates apply to the amount of excess of the monthly remuneration over the minimum wage.

Note! For 2022, the minimum wage established at the federal level is 12,130 rubles. The regional minimum wage does not affect the calculation of contributions.

For contributions to mandatory pension insurance and VNiM, maximum annual bases have been determined in the amount of 1,292,000 and 912,000 rubles, if exceeded, the calculation of amounts for pension insurance is carried out at a preferential rate of 10%, and contributions to VNiM cease to be accrued. That is, in these cases, comparing monthly income with the minimum wage for the purpose of calculating insurance premiums no longer makes sense. There is no base limit for health insurance.

Regarding the reduced rate

In accordance with Art. 427 of the Tax Code of the Russian Federation, reduced insurance rates are determined for some payers, namely:

- for business entities in the field of IT technologies;

- for enterprises paying wages and other remunerations to crew members of ships listed in the international register of ships of the Russian Federation;

- non-profit organizations (except for state/municipal institutions), using the simplified tax system, whose activities are included in the list of clause 1 of Art. 427 Tax Code of the Russian Federation;

- charitable organizations on the simplified tax system;

- other organizations and business entities named in Art. 427 Tax Code of the Russian Federation.

According to Federal Law No. 102-FZ dated 04/01/2020, small and medium-sized businesses can pay insurance premiums at a reduced rate from April 1, 2022, provided that they were included in the appropriate register before April 1, 2022.

How the reduced rate works:

- Up to a salary of 1 federal minimum wage, the usual rate of 30% is applied;

- Above the salary of 1 federal minimum wage, a reduced rate of 15% is applied (10% for compulsory health insurance, 5% for compulsory medical insurance, 0% for compulsory social insurance).

Calculation of personal income tax based on the minimum wage

Article 210 of the Tax Code establishes that the tax base is calculated taking into account all income, and does not make an exception for the case of wages at the minimum wage level.

Thus, the employer is obliged to withhold 13% from any salary and transfer it to the budget. And if an employee receives a salary in the amount of the minimum wage, then after withholding personal income tax he will receive a “net” amount less than the established minimum wage.

Let's consider the case of working part-time if the full-time wage is equal to the minimum wage. In 2022, the minimum wage is 13,890 rubles, so half the rate is 6,945 rubles. Personal income tax will be 13% of 6945 rubles, that is, 903 rubles. The employee will receive 6945 minus 903, i.e. 6042 rub.

Document

Resolution of the Constitutional Court of the Russian Federation No. 40-P dated December 16, 2019

Regarding the rate relative to risk

The rate depending on the class of professional risk:

| Occupational risk class | Bet size |

| I | 0,2% |

| II | 0,3% |

| III | 0,4% |

| IV | 0,5% |

| V | 0,6% |

| VI | 0,7% |

| VII | 0,8% |

| VIII | 0,9% |

| IX | 1% |

| X | 1,1% |

| XI | 1,2% |

| XII | 1,3% |

| XIII | 1,4% |

| XIV | 1,5% |

| XV | 1,7% |

| XVI | 1,9% |

| XVII | 2,1% |

| XVIII | 2,3% |

| XIX | 2,5% |

| XX | 2,8% |

| XXI | 3,1% |

| XXII | 3,4% |

| XXIII | 3,7% |

| XXIV | 4,1% |

| XXV | 4,5% |

| XXVI | 5% |

| XXVII | 5,5% |

| XXVIII | 6,1% |

| XXIX | 6,7% |

| XXX | 7,4% |

| XXXI | 8,1% |

| XXXII | 8,5% |

Changes in personal income tax from 2022

1. A new social deduction has appeared - for physical education and health services. You can buy a subscription to a fitness club, gym or sports club, or order a training plan from specialists. You can receive a refund on expenses for yourself and children under 18 years of age. There are two conditions:

- the paid service must be included in the list approved by the Government (Order of the Government of the Russian Federation dated September 6, 2021 N 2466-r);

- the organization or individual entrepreneur that provides the service must be included in the list of the Ministry of Sports.

The total amount of social deduction has not been changed; it remains 120,000 rubles. It includes expenses for charity, education, treatment, pensions, etc. (except for the education of children and expensive treatment).

Federal Law No. 8-FZ dated 17.02.2021

2. We approved a simplified procedure for obtaining personal income tax deductions. This applies to property and investment deductions. Now individuals will not need to submit 3-NDFL declarations and collect certificates from the employer; they just need to sign a pre-filled application posted in their personal account. The inspectorate will now send confirmation of the right to the deduction to employers directly, bypassing the employee.

Federal Law of April 20, 2021 No. 100-FZ

3.

More compensation that employers pay to employees to pay for travel vouchers is exempt from personal income tax. Now they will not withhold personal income tax from voucher compensation for employee’s children who have not reached 18 years of age or 24 years of age when studying full-time.

In addition, vouchers that were purchased once in a calendar year were exempted from tax.

The exemption no longer requires that the cost of the trip be taken into account when calculating income tax.

Federal Law No. 8-FZ dated 17.02.2021

4. Families with children are now exempt from paying personal income tax on sold real estate, but only if the following conditions are met:

- children under 18 years old (24 years old if studying full-time);

- cadastral value of sold residential real estate is less than 50 million rubles;

- the area or cadastral value of the purchased residential premises is greater than that of the sold one;

- on the date of sale of real estate, the taxpayer and his family members own no more than 50% of the ownership of another residential premises with a total area exceeding the total area of the old residential premises purchased to replace them.

This exemption applies to income received in 2021. However, to do this, you need to purchase new housing or pay the full cost of the apartment under a shared construction agreement by April 30, 2022.

Federal Law of November 29, 2021 No. 382-FZ

5. The minimum maximum period of ownership of a real estate property purchased under a DDU agreement is counted from the moment of full payment of the cost of the object under such an agreement.

Federal Law dated July 2, 2021 No. 305-FZ.

Calculation of wages and insurance premiums

Regulatory regulation

Accrued wages are displayed according to Dt of the labor cost account and Kt 70 “Settlements with personnel for wages” (chart of accounts 1C).

Learn more Determination of methods of accounting for salaries (main transactions)

Calculation of personal income tax amounts is carried out by tax agents on the date of actual receipt of income on an accrual basis from the beginning of the tax period (clause 3 of Article 226 of the Tax Code of the Russian Federation). The date of actual receipt of income in the form of wages is the last day of the month indicated in the Salary field for Payroll document (clause 2 of Article 223 of the Tax Code of the Russian Federation). It will be reflected on page 100 of Section 2 of form 6-NDFL.

Learn more Formation of form 6-NDFL

Personal income tax is calculated in full rubles. Amount over 50 kopecks. rounded to the nearest ruble, less than 50 kopecks. - discarded (clause 6 of article 52 of the Tax Code of the Russian Federation).

Insurance premiums are calculated based on the results of each calendar month based on the accrued amount and tariffs of insurance premiums. (Clause 1 of Article 431 of the Tax Code of the Russian Federation). The amount of insurance premiums is determined in rubles and kopecks (Clause 5 of Article 431 of the Tax Code of the Russian Federation).

Accounting in 1C

Payroll is reflected in the Payroll document in the Salaries and Personnel section – Salary – All accruals – Create button – Payroll.

The header of the document states:

- Salary for - May : month for which wages are calculated.

- Division - not filled in, since in our example payroll is calculated for several divisions at once.

By clicking the Fill , the table section automatically displays all employees for whom there is data for payroll with already calculated data.

What actions must be taken if an employee was not included in the document during automatic completion or the amounts were not reflected correctly?

If a document is filled out incorrectly when automatically filled in, you need to check:

- From what period the employee was employed: look in the Employees directory Hiring date field . PDF

- Field Division . If it is filled out in the document, then we check: according to the documents in 1C, the employee is employed in this department, and whether there have been personnel movements. We look in the Employees the Division field and personnel movements using the link Personnel documents . PDF

- Whether wages were previously calculated using another document (the Payroll was created earlier). This can be checked using the Salary Analysis by Employees (Monthly) in the Salaries and Personnel – Salaries – Salary Reports section.

If, in addition to automatic calculation, it is necessary to enter additional accrual or deduction, then you must use the Accrue PDF and Withhold PDF buttons.

Learn more:

- Additional charges

- Additional deductions

Table part:

- Employee - an employee for whom wages are calculated. Selected from the Employees .

- Days - the number of days according to the Production calendar .

- Hours - the number of hours worked according to the Production calendar .

- Accrued - the total amount of accruals for the employee. The link in the Accrued in the additional form displays a detailed description of all accruals for the employee.

In our example, only Payment by salary , but if there are other charges, they will also be displayed. If necessary, the Days , Hours and Accrued can be adjusted manually.

In May 2022, with a five-day working week (40 hours), there are 20 working days, 159 hours.

Staff Komarov V.S. and Mashuk K.V. were employed before May 1st.

Employee Gordeev N.V. was hired on May 23, 2022, so he has 7 working days and 56 hours according to the production calendar.

Salary of employee Gordeev N.V. — 35,000 rub.

Accrued for May - 35,000 rubles / 20 days * 7 days = 12,250 rubles.

For the rest of the employees, the salary was accrued in full: they have fulfilled all the daily quotas.

- Personal income tax - the total amount of personal income tax withheld from wages. The link in the personal income tax in an additional form displays the calculation of personal income tax on an accrual basis for the employee for the current tax period, and also indicates the deductions provided.

Employee Gordeev N.V. a deduction was provided for children in the amount of 1,400 rubles.

Personal income tax = (12,250 – 1,400) * 13% = 1,410.50 (rounded to 1,411 rubles).

The amount we calculated corresponds to that indicated in 1C.

- Contributions - the total amount of calculated contributions for the employee. The link in the Contributions in the additional form displays the calculation of contributions for an employee by each type of contribution.

Let's consider the calculation of contributions according to Gordeev N.V. (income - 12,250 rubles):

The calculation we presented corresponds to the calculation performed in 1C. This means that the calculation of contributions in the program is correct.

Learn more Insurance premium settings

If, in addition to personal income tax, employees have other deductions in the tabular section, for example, according to a writ of execution, then the document displays the Deductions . In our example, there are no deductions, so this column is hidden in the tabular section by default.

Postings according to the document

The document generates transactions:

- Dt (20.01) Kt - payroll.

- Dt Kt 68.01 - calculation of personal income tax and its deduction from wages.

- Dt (20.01) Kt 69.01 - calculation of contributions to the Social Insurance Fund.

- Dt (20.01) Kt 69.03.1 - calculation of contributions to the FFOMS.

- Dt (20.01) Kt 69.02.7 - calculation of contributions to the Pension Fund.

- Dt (20.01) Kt 69.11 - calculation of contributions for NS and PZ.

Learn more:

- Setting up the main method for reflecting accrued salary

- Determining salary accounting methods (main postings)

- Setting up cost items to reflect insurance premiums

You can check accrued tax contributions using the Taxes and contributions report (briefly) in the section Salaries and personnel – Salary – Salary reports – Taxes and contributions (briefly). PDF

Documenting

Payslips for employees can be printed using the Payslip in the Salaries and Personnel – Salary – Payroll Reports – Payslip section. PDF

The payslip in form T-51 can be printed using the Payslip (T-51) in the section Salaries and Personnel – Salaries – Salary Reports – Payslip (T-51). PDF

6-NDFL

In Form 6-NDFL, payroll is reflected in:

Section 1 “Generalized indicators”:

- line 020 - 107,250 , amount of accrued income;

- line 030 - 1,400 , the amount of deductions provided;

- pp. 040 - 13,761 , amount of calculated tax.

Section 2 “Dates and amounts of income actually received and withheld personal income tax”:

- page 100 - 05/31/2018 , date of actual receipt of income;

- pp. 130 - 107,250 , the amount of income actually received.

Section 2 of form 6-NDFL will be filled out only after the actual payment to the employee, i.e. after creating the document Write-off from the current account .

For the continuation of the example, see the publication:

- Payment of wages

See also:

- Salary settings: 1C

- Accounting policy for NU: Insurance premiums

- Method of reflecting wages in accounting

- Changing payroll data

- Sick leave benefit

- Accrual of vacation pay

- Payment of wages

- Transfer of personal income tax and contributions

Did the article help?

Get another secret bonus and full access to the BukhExpert8 help system for 14 days free of charge