Options for errors requiring a refund and their consequences

In relations between counterparties, errors in the transfer of funds are possible, associated with:

- with the wrong choice of counterparty when generating a payment order;

- indicating an incorrect payment amount;

- reflection in the purpose of payment of the details of a document that does not exist in the relationship.

Such errors can be identified by any of the parties, but will require a mandatory written expression of the initiative of the payer of funds to take actions carried out in connection with their correction.

In a number of situations, the error can be corrected by adjusting the purpose of the payment if, for example, there is a supplier-buyer relationship between the counterparties, against which an erroneously transferred amount (or a payment with an incorrectly specified purpose) may be taken into account.

You will find a sample letter to the counterparty to clarify or change the purpose of payment in ConsultantPlus. If you do not already have access to this legal system, a full access trial is available for free.

Correction via payment adjustment cannot be applied if there are no current engagement agreements with the payee.

Regardless of the reason for which the payment was considered to have been made without reason, it is recorded by both the payer and the recipient using the same algorithms, taking into account the fact that for these two parties the transactions when returning the erroneously transferred funds will be mirror images.

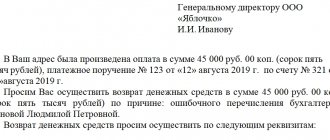

Since erroneous transfers subject to refund have no connection with the calculations performed between suppliers and buyers, VAT on them is not allocated either for payment or as deductions. However, if calculations are carried out in foreign currency, then exchange differences attributable to income/expenses may arise. The recipient of the funds, when returning them, in the purpose of payment in the payment document should reflect information that this payment is used to return the funds erroneously transferred to him, and provide a link to the details of the document in which the payer expressed a request to return the money to him.

If the error is corrected by taking into account the transferred amount as payment under another supply agreement, then it will be taken into account in the usual manner for the supplier-buyer relationship with the implementation of the necessary VAT transactions.

If you need to return money to the buyer from the cash register, first look at what ConsultantPlus experts say about returns:

If you don't have legal access, a full access trial is available for free.

Returning money to a counterparty is a reason for banking control

Is it true that the reason for requesting documents from an organization within the framework of banking control can be such a harmless operation as transferring to a counterparty an amount of money previously received from it?

Yes, true, but only if the following conditions are simultaneously met:

- the money was received from one partner’s account and is returned to his other account;

- both transactions took place within a short period of time.

Rationale .

As an appendix to the Regulations of the Central Bank of the Russian Federation No. 375-P, a Classifier is provided containing signs indicating the unusual nature of the transaction and codes assigned to these signs. In the Classifier, code 1121 refers to the operation “Return by a client (client’s representative) of a credit institution of funds to a counterparty within a short period of time to the account of the specified counterparty, different from the account from which these funds were received to the client.”

What period is recognized as a short period of time is not established in the Regulation of the Central Bank of the Russian Federation No. 375-P, but it is stated that such assessment categories as systematicity, significance, short period, etc., are determined by the bank in each specific situation independently based on the nature , the scale and main activities of clients, the level of risks associated with clients and their operations.

The decision to qualify (non-qualify) a client’s transaction as a suspicious transaction is made by a credit institution independently on the basis of the information and documents at its disposal characterizing the status and activities of the client carrying out the transaction, as well as his representative and (or) beneficiary, beneficial owner (if any). availability).

The bank has the right to use other signs indicating the unusual nature of the transaction, established by the credit institution independently.

According to clause 6.3 of the Regulation of the Central Bank of the Russian Federation No. 375-P, systematic and (or) significant volumes of transactions containing signs indicating the unusual nature of the transaction named in the Classifier, or signs included by the bank in its internal control rules, may allow the bank to accept decision to refuse to execute a client’s order to perform a transaction.

If the transaction is considered suspicious by the bank, information about it must be sent to Rosfinmonitoring.

Thus, if money was received from one partner’s account and returned to his other account and both transactions were completed within a short period of time, the bank may suspend the transaction and require the presentation of documents confirming its compliance with the law. In case of refusal to submit documents, submission of them incompletely, or the bank classifying the operation as doubtful as a result of the analysis as a result of the analysis and refusal to complete it, information about it will be sent to Rosfinmonitoring.

Making two or more decisions during a calendar year to refuse to execute a client’s order to carry out a transaction allows the bank to terminate the bank account (deposit) agreement with the client (clause 5.2 of Article 7 of Law No. 115-FZ).

Hello Guest! Offer from "Clerk"

Online professional retraining “Accountant on the simplified tax system” with a diploma for 250 academic hours . Learn everything new to avoid mistakes. Online training for 2 months, the stream starts on March 15.

Sign up

Incorrectly addressed money arrived in the current account: postings

For the recipient of funds to whose current account money was mistakenly received, a posting reflecting the receipt of unidentifiable funds will be made at the time the payment document is linked to the accounting accounts.

A similar amount is debited to account 76, and this is done by posting Dt 76 Kt 51 (52).

Accordingly, if the erroneous payment is returned to the counterparty's current account, the posting will be reversed: Dt 51 (52) Kt 76. The exchange rate difference when returning currency will be reflected by the posting Dt 91 Kt 76 or Dt 76 Kt 91.

If, in relation to a payment reflected as an error, a decision arises to take it into account as payment for a future or already completed sale of goods (performance of work, provision of services), then on the basis of written information received from the payer, an entry will be made Dt 62 Kt 76 with the ensuing hence the VAT implications.

Features of returning funds to the client in 1C

Returning funds to the client's card

Various trade organizations often return funds to their clients using a regular plastic card. This method is applicable if the buyer previously paid for the item with this card, and then decided to return it back within two weeks. To process a money transfer using an accounting program to a card, you need to go to the “Bank and cash desk” section and click on the “Payment card transactions” link. After this, a window with the operations created earlier will appear in front of the user.

In the window that appears, you need to find and click on the “Create” button. Next, select the “Return to Buyer” option. After this, a special form for returning funds will open in front of the user in the 1C program.

This form requires the following information:

- Name of the organization.

- Counterparty. For example, “Individual (retail)”.

- Refund amount.

- Type of payment. For example, “Payment by card”.

In order to save and post a document, you need to click the following buttons “Record” and “Post”. Next, you need to click on the “DtKt” button to check the accounting records. After this, the window for making transactions will open.

In the posting window, you can see the operation on the debit of account 62.01 “Settlements with buyers and customers” and the credit of account 57.03 “Sales by payment cards” for the amount of the refund. After the financial institution debits funds from the current account, the balance on account 57.03 will become zero.

After some time, the funds will be debited from the current account and transferred to the acquiring bank. Well, or the amount of the refund will simply reduce the receipt of card payments. It must be remembered that all transactions carried out on the current account are usually downloaded from the client bank.

If the refund was reflected as a separate transaction on the current account, then it is recommended to include the correct details in the write-off document. To do this, go to the “Bank and Cash Office” section and click on the “Bank Statements” link. Only after this the window with operations will open.

In this statement you should find the required operation called “Write-off from the current account.” Some changes need to be made to the relevant fields. Namely:

- Type of operation. Here you should indicate “Other write-off”.

- Recipient. You must select “Individual”.

- Expense item. You need to select the appropriate value: for example, “Refund to the buyer.”

- Debit account. You need to put "57.03".

- Counterparty. You need to select an acquiring bank from the directory.

- Contracts. You should specify the details of the agreement with the bank.

The next step is to reflect the operation in accounting, for which it is recommended to click on the following buttons: “Post” and “Record”. To familiarize yourself with the accounting entries, you need to click on the “DtKt” button. After which the posting window will open in front of the user.

In the posting window you can see the debit operation of account 57.03 “Sales by payment cards”. Here you can also familiarize yourself with the transaction on crediting account 51 “Current account” for the transfer amount. From this moment on, the account balance 57.03 will be equal to 0.

How to make a cash refund?

This procedure is simple because it is done using one document. The user is recommended to find the appropriate section “Bank and cash desk”, and then click on the link “Cash documents”. Next, a cash transactions window will appear in front of him.

The next step is to click on the title “Issue” in the window that just opened. Next, the user will be able to familiarize himself with a form in which some data must be entered.

It is recommended to include the following information here:

- Name of the organization.

- The type of operation performed. You should select the “Return to Buyer” option.

- Receiver name.

- Refund amount.

- Agreement concluded with the buyer.

To complete the procedure, press the “Record” button, and then “Perform”. To familiarize yourself with the postings, it is important to click on “DtKt”. After this, a window with postings will open in front of the user.

It should be noted that in the transactions there was an operation on the credit of account 50.01 and the debit of account 62.01. Consequently, a refund was issued.

Refund to the buyer's bank account

To carry out the operation, you only need one document. It is recommended to go to the “Bank and Cash Office” section, and then click on the “Bank Statements” link. Next, the corresponding window for transactions carried out on the bank will open.

Many companies download transactions from the system to the client bank. In this case, to process a refund, you must correct the type of transaction being performed. To do this, you need to enter the required debit from the current account and indicate the desired type of operation “Return to buyer”. Additionally, it is recommended to check the remaining details that were downloaded from the client bank. The next step is to press the “Record” key. Next, you need to click on the “Proceed” button. In order to view the postings, you need to click “DtKt”.

In the postings you can see the operation of debiting the account and crediting the account for the amount of the refund. You can verify that the return has been generated.

Postings when returning an erroneously transferred payment from a counterparty

For the payer, the amount transferred to the wrong counterparty or transferred in a larger volume also goes to account 76: Dt 76 Kt 51 (52) or Dt 76 Kt 60 (if it is no longer possible to correct the posting made on the payment order).

The return of incorrectly transferred funds from the counterparty in the postings will be expressed as Dt 51 (52) Kt 76. For currency payments, here you will also need to take into account the exchange rate difference, the amount of which will be charged either to the debit or credit of account 91 (Dt 91 Kt 76 or Dt 76 Kt 91).

If, in relation to an erroneous payment, a decision is made to offset it against payment for a delivery within the framework of an existing relationship with the counterparty, then the payment recorded on account 60 will simply change the analytics due to internal posting. In this case, it will be possible to take into account VAT in deductions for both advance payment and delivery.

Results

All actions with a payment transferred to a counterparty by mistake are carried out with a written indication of their nature on the part of the payer.

In this case, the funds can be offset against settlements on existing relationships. In the accounting of both the recipient and the payer, the amount of the erroneous payment is reflected in account 76. In correspondence with this account, both parties will show the cash flow for the return: Dt 76 Kt 51 (52) - for the returning party, Dt 51 (52) Kt 76 - at the recipient of the refunded funds. Returning an erroneous payment has no tax consequences. You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.