What refers to the income and expenses of an enterprise in accounting

Every commercial company is created for the purpose of making a profit. To derive a financial result, it is necessary to competently organize the correct accounting of the organization’s income and expenses .

The results of the company’s work are of interest not only to its participants, but also to investors, as well as fiscal authorities. At the same time, tax accounting and accounting of income and expenses are somewhat different.

In accounting, the concept and algorithm for accounting for income and expenses are regulated by PBU 9/99 and PBU 10/99, respectively. At the same time, the lists of other income and expenses are open.

The company’s income is an increase in the economic benefits of the organization as a result of the receipt of cash or other assets, as well as the repayment of obligations, resulting in a capital gain (clause 2 of PBU 9/99). There are two types of income: from ordinary activities and others. What applies to each of them can be seen in the table:

| Income | |

| From ordinary activities (clause 5 of PBU 9/99) | Other (clause 7 of PBU 9/99) |

| Revenue from sales of inventory items and services | Proceeds from the sale of OS |

| Other income that is the subject of the main activity of the company | Penalties, penalties and penalties for non-compliance with contractual obligations |

| Assets received as a gift | |

| Income from the lease of company assets | |

| Exchange differences | |

| Overdue creditor | |

| Other income | |

Revenue is shown in accounting if the following conditions are met (clause 12 of PBU 9/99):

- The company has the right to it under an agreement or on the basis of another document.

- The amount of revenue can be determined.

- Ownership of the asset has passed from the seller (performer) to the buyer (customer).

- There is confidence that the company will benefit.

- The costs associated with the operation can be determined.

If the above conditions are not met, a creditor is created in accounting.

The company's expenses are a decrease in the economic benefits of the company resulting from the disposal of cash or other assets of the enterprise, as well as the formation of liabilities that led to a decrease in capital (clause 2 of PBU 10/99).

In accounting, a company's costs are also divided into 2 types: other and from ordinary activities.

| Expenses | |

| From ordinary activities (clause 5 of PBU 10/99) | Other (clause 11 PBU 10/99) |

| Costs associated with production and sales of products | Contributions to valuation reserves |

| Expenses for buying and selling goods | Expenses associated with the disposal of fixed assets |

| Costs associated with the work | Interest transferred by the company under loan agreements |

| Other expenses that are the subject of the company’s activities | Costs associated with the transfer of assets for temporary use |

| Other expenses | |

Clause 16 of PBU 10/99 provides the following factors for accepting costs in accounting:

1. The reasonableness of the costs is confirmed by a certain agreement, legal regulations or business rules.

2. The amount of costs can be identified.

3. The presence of confidence that as a result of this business operation there will be a decrease in the economic benefits of the company.

If at least one of the above conditions is not met, a receivable is recognized in accounting.

There are 2 methods of accounting for income and expenses: cash and accrual methods. The first method is used, as a rule, for simplified taxation.

Find out about the differences in the methods of accounting for income and expenses here.

IMPORTANT! The cash method in accounting can only be used by organizations that use simplified accounting methods and submit simplified accounting reports.

Find out about the nuances of accounting for income and expenses using the cash method in accounting in ConsultantPlus. If you don't have access to the system, get a free trial online.

List of income not taken into account under the simplified tax system

Income that is not taken into account when determining the object of taxation is given in Article 251 of the Tax Code. Here are some of them:

- property received in the form of collateral or deposit. BUT, if the seller withholds payment for the delivered goods from the deposit received, then the corresponding amounts should be included in the tax base according to the simplified tax system on the date of offset (withholding) of funds to pay off the debt for the sold goods (letter of the Ministry of Finance of Russia dated June 22, 2015 No. 03-11-06/2/36071, Federal Tax Service of Russia dated December 30, 2014 No. GD-4-3/ [email protected] );

- property received as a contribution to the authorized capital or a contribution to a joint activity;

- amounts received by the intermediary when fulfilling obligations under a commission agreement, agency agreement or agency agreement (except for intermediary remuneration);

- money and property received under a credit agreement or loan agreement (including under an assignment agreement by a new creditor) in order to repay the principal debt;

- property received by the company as part of targeted financing. In this case, the company must keep separate records of income (expenses) received (produced) within the framework of targeted financing;

- capital investments of the tenant in the form of inseparable improvements to the leased property;

- interest on state and municipal securities subject to corporate income tax (clause 4 of article 284, clause 2 of article 346.11 of the Tax Code of the Russian Federation);

- interest on bank deposits received by individual entrepreneurs;

- income of the founders of trust management of mortgage coverage obtained on the basis of mortgage participation certificates;

- dividends. Note that dividends received by a “simplified” person are not taken into account when determining the maximum amount of income for applying the simplified tax system. This is due to the fact that income in the form of dividends, subject to income tax, is not recognized as income under the simplified tax system (clause 1.1 of article 346.15 of the Tax Code of the Russian Federation).

- income from activities subject to UTII.

EXAMPLE

In the fourth quarter of last year, Passiv LLC, being a UTII payer, was engaged in the provision of household services. This year the company is applying the simplified tax system. In payment for services provided last year, part of the funds was received this year. Since during the period of application of UTII, income from their sale received while working on the simplified tax system is not taken into account when determining the tax base according to the simplified tax system.

The list of “simplified” income also does not include positive exchange rate differences, since they simply do not arise. The fact is that with the cash method, revenue is considered to be exactly the amount that the buyer paid. At the time of shipment of goods (performance of work, provision of services), revenue is not reflected in tax accounting. The same is true with expenses - they cannot be more or less than the amount that the “simplified” person actually transferred to the partner.

Income and expenses from a tax point of view

Tax accounting of income and expenses is carried out for the purpose of calculating taxable profit (and some other types of taxes paid under special regimes) and is regulated by Chapter 25 of the Tax Code of the Russian Federation. And if in accounting it is necessary to display absolutely all the company’s business operations, then in the tax office there is a list of income and expenses that cannot be taken into account.

Income is an economic benefit expressed in cash or in kind (Clause 1, Article 41 of the Tax Code of the Russian Federation). Tax accounting provides for 2 types of income: from sales and non-sales. There is also a list of tax-free income.

| Income | Tax-free receipts | |

| From implementation | Non-operating | |

| Revenue from the sale of goods (works and services) both own production and purchased, reduced by the amount of VAT | Income from rental assets | Contributions of participants to the management company |

| Interest received under loan, credit or bank deposit agreements | Advances received | |

| Assets received free of charge (accounted for at market prices, but limited to the residual value of the transferor) | Credits and loans | |

| Surpluses identified during inventory | Property received under agency agreements | |

| Other income listed in Art. 250 Tax Code of the Russian Federation | Other income listed in Art. 251 Tax Code of the Russian Federation | |

Details are in the materials:

- “How to take into account non-operating income when calculating income tax?”;

- "St. 251 of the Tax Code of the Russian Federation - list of income."

There are special requirements for tax expenses (clause 1 of Article 252 of the Tax Code of the Russian Federation):

- Expenses must be confirmed by a correctly completed primary document.

- It is necessary to justify their economic necessity.

They are divided into costs associated with production and sales and non-sales.

| Expenses | Costs not taken into account when taxing profits | ||||

| Related to production and sales | Non-operating | ||||

| Material (Article 254 of the Tax Code of the Russian Federation) | Salaries (Article 255 of the Tax Code of the Russian Federation) | Depreciation (Articles 256–260 of the Tax Code of the Russian Federation) | Others (Articles 261-264 of the Tax Code of the Russian Federation) | The list consists of 20 types of expenses (Article 265 of the Tax Code of the Russian Federation). These also include those named in Art. 266-267.4 Tax Code of the Russian Federation. | The list of expenses given in Art. 270 Tax Code of the Russian Federation |

Find out how to correctly account for tax expenses in the section “Income Tax Expenses - List”.

To determine tax profit, it is necessary to make a separate calculation, displaying information on income and expenses taken into account in the tax base in special tax registers. The object of taxation is profit, which is calculated by reducing income by the amount of expenses.

If you have access to ConsultantPlus, check whether you correctly account for income and expenses in tax accounting. If you don't have access, get a free trial of online legal access.

What income does Article 249 of the Tax Code of the Russian Federation classify as income from sales?

Chapter 25 of the Tax Code of the Russian Federation classifies income as follows:

- income from sales (Article 249 of the Tax Code of the Russian Federation);

- non-operating income (Article 250 of the Tax Code of the Russian Federation).

Income from sales is revenue, namely receipts from (clause 1 of Article 249 of the Tax Code of the Russian Federation):

- sales of manufactured products;

- resale of purchased goods;

- realization of property rights;

- performance of work;

- provision of services.

It is very important to correctly account for income from sales in tax accounting. Otherwise, disputes with tax authorities are possible. Find out how recent judicial practice is developing on the application of Art. 249 of the Tax Code of the Russian Federation, from an analytical selection from ConsultantPlus. Study the material by getting trial access to the K+ system for free.

To learn how income from sales is reflected in the income statement, read the article.

Principles of accounting for income and expenses of an organization

In accounting, the following basic principles of accounting for a company’s income and expenses are distinguished:

- The principle of objectivity - all business transactions must be reflected in accounting using the continuous entry method in the accounts provided for in the chart of accounts in ruble equivalent.

- The principle of double entry - any movement of the company's assets and liabilities is reflected simultaneously in the debit of one account and in the credit of another based on primary documentation.

- Accrual principle - information is displayed in accounting as it occurs in the reporting period in which it was made, and not upon payment.

- The principle of correspondence - the income of an enterprise must be correlated with expenses.

Tax legislation provides for the following principles for accounting for company income and expenses:

- The principle of continuity - accounting of income and expenses is carried out continuously from the moment of registration of the company until the date of its deregistration.

- The principle of time certainty - allows you to take into account income and expenses both on a cash basis and on an accrual basis.

- The principle of consistency indicates that tax accounting rules and regulations are consistently applied from one tax period to another.

- The principle of validity of recognition of income and expenses implies that the taxpayer makes economically justified and documented expenses and, if necessary, will be able to prove their validity in accordance with legislative norms (or business turnover).

- The principle of uniform recognition of income and expenses helps to distribute expenses evenly if the contract provides for the receipt of income over more than one reporting period, and there is no stage-by-stage delivery of goods (work, services).

Features in the date of recognition of income under Art. 250 Tax Code of the Russian Federation

Also, many difficulties arise from questions regarding the date of recognition of non-operating income. It is especially important to have a clear position on this issue when checking the correctness of tax assessments by fiscal inspectors.

Let's look at a few common cases that can cause difficulties for taxpayers.

So, the amount of insurance compensation should be taken into account as part of gross income as of the date:

- making such a positive decision by the insurer if the taxpayer uses the accrual method in accordance with subparagraph. 4 p. 4 art. 271 Tax Code of the Russian Federation;

- receiving funds from the insurer using the cash method in accordance with clause 2 of Art. 273 Tax Code of the Russian Federation.

A taxpayer using the accrual method when calculating income tax includes as income the amount of rent from leasing out its assets on the last day for reporting (usually this day is specified in the agreement, and it may be the last day of each calendar month) - according to subclause. 3 p. 4 art. 271 Tax Code of the Russian Federation. If the taxpayer considers income taxable as profit using the cash method, then the date of accounting for rent as part of non-operating income is the moment of actual receipt of funds (clause 2 of Article 273 of the Tax Code of the Russian Federation).

You can learn about the fundamental differences in these methods from our article “Accrual method and cash method: main differences” .

Important! At the same time, there is some conflict as to whether rent is included in non-operating income or whether it should be classified as income from the provision of services. Thus, based on the norms of the Tax Code and armed with the explanations of the financial department set out in the letter of the Ministry of Finance dated 02/07/2011 No. 03-03-06/1/74, it is possible to classify rent as income from sales (Article 249 of the Tax Code of the Russian Federation) only in that case if the taxpayer provides such services systematically, and they are the main ones among the company’s activities listed in the Unified State Register of Legal Entities (or for individual entrepreneurs in the Unified State Register of Individual Entrepreneurs).

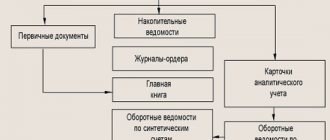

Algorithm for accounting for company income and expenses

Accounting for income and expenses of an organization is carried out on the basis of the Law “On Accounting” dated December 6, 2011 No. 402-FZ, no.

Accounting for income and expenses is carried out using the double entry method using the corresponding accounts approved by order of the Ministry of Finance dated 31.10.2000 No. 94n. Analytics is carried out for each type of income and expense with the ability to identify the financial result for each operation.

To summarize information about income and expenses received from ordinary activities, the chart of accounts provides for account 90 “Sales”, to which the main sub-accounts are opened:

- 90.1 “Revenue” - for accounting for income recognized as revenue;

- 90.2 “Cost” - for cost accounting;

- 90.3 “VAT” - to account for tax due from buyers;

- 90.4 “Excise taxes” - for accounting for amounts of excise taxes (and also applicable when selling excise goods).

To account for other expenses, organizations can open other subaccounts to account 90.

To determine the financial result, which represents the difference between revenue and self-worth, subaccount 90.9 “Profit/loss from sales” is used. At the end of each month, the results of the company’s work are displayed by comparing debit turnover on subaccounts opened for accounting for expenses and other “negative” items (90.2-90.8ٜ), with credit turnover on subaccount 90 ٜ.1ٜ. The identified amount is written off by posting Dt 90.9 Kt 99 in case of excess of income over expenses or Dt 99 Kt 90.9 - in case of a loss. The sum of the subaccounts accumulates during the year, at the end of which they are closed internally:

Dt 90.1 Kt 90ٜ.9 - written off to the “Revenue” subaccount;

Dt 90.9 Kt 90ٜ.2 (90.3, 90.4...) - written off including subaccounts of costs, VAT and other items that reduce revenue.

To account for other income and expenses, account 91 “Other income and expenses” is used, to which the following subaccounts are opened:

- 91.1 “Other income” - for accounting for income not related to the main type of activity;

- 91.2 “Other expenses” - to account for other costs;

- 91.9 “Balance of other income and expenses” - to identify profit/loss from transactions related to other types of activities.

Similar to accounting for income and expenses from ordinary activities, the accountant at the end of the month compares the balance of accounts 91.1 and 91.2 and writes off the resulting result by posting Dt 91.9 Kt 99 - upon receipt of profit or Dt 99 Kt 91.9 - loss at the end of the month. Subaccounts are closed at the end of the year using internal transactions.

Tax accounting of income and expenses, as mentioned earlier, has some differences from accounting.

Example

entered into a car rental agreement with a company employee, according to which the monthly rent is 7,500 rubles. The car's engine capacity is less than 2,000 cm3.

When calculating taxable profit, you can take into account no more than 1,200 rubles. (Subclause 11, Clause 1, Article 264 of the Tax Code of the Russian Federation). That is, in accounting expenses it will be reflected in 6,300 rubles. (7,500 – 1,200) more costs than in the tax office. Tax accounting analytics can be displayed as follows:

| Check | Sum | Analytics |

| NU 91.2 “Other expenses” | 1 200 | Expenses accepted for tax purposes |

| 6 300 | Expenses not taken into account when calculating profit |

In this case, a permanent tax liability is formed, which is reflected in accounting by posting Dt 99 Kt 68 - 6,300 rubles.

Between tax accounting (TA) and accounting (BU), when recording certain incomes and expenses, not only permanent but also temporary differences can arise. This means that the event is displayed in accounting earlier (later) than in tax accounting.

The rules for accounting for permanent and temporary differences are shown in the table below.

| Permanent differences (between NU and BU arise in the same tax period) | ||

| Sign | Profit in BU is higher than in NU | In BU the profit is less than in NU |

| Consequence | Permanent tax liability (PNO) | Permanent tax asset (PTA) |

| Tax nuances | Conditional consumption | Conditional income |

| Wiring | Dt 99 Kt 68 | Dt 68 Kt 99 |

| Temporary differences (between BU and NU arise in different tax periods) | ||

| Sign | In NU profit is recognized earlier than in accounting | In accounting, profit is recognized earlier than in NU |

| Consequence | Deductible Temporary Difference (DTD) | Taxable temporary difference (TDT) |

| Tax nuances | Deferred tax asset (DTA) | Deferred tax liability (DTL) |

| Wiring | Dt 09 Kt 68 - form; Dt 68 Kt 09 - repay | Dt 68 Kt 77 - form; Dt 77 Kt 68 - repay |

More details about the algorithm for accounting for permanent and temporary differences can be found in the material “Differences between accounting and tax accounting.”

Tax accounting can be kept separately from accounting (most often this method is chosen by large companies) or on the basis of accounting data highlighting tax differences (this method is usually chosen by small taxpayers). In any case, correct tax and accounting management according to “double standards” is only possible using automated systems.

Program for accounting income and expenses

Today, the market is replete with a variety of software that allows you to keep track of an organization’s income and expenses. The most popular among them is the 1C-Enterprise program. The latest versions allow you to take into account a large amount of information and work with several users simultaneously. The program has various modules with an intuitive interface. The manufacturer monitors all legislative changes and releases the necessary updates in a timely manner. The disadvantage of this software is its significant cost, as well as the need to pay for the services of service specialists.

As for free programs for recording income and expenses, they can be downloaded on the Internet, but with limited functionality.

Results

The purpose of accounting and tax accounting is to generate complete and reliable information about the financial position of an enterprise to provide it to interested internal and external users. Organization of correct accounting of income and expenses is the most important aspect of the activities of enterprises of any scale.

Fiscal authorities pay close attention to the procedure for accounting for income and expenses by taxpayers. At the same time, tax accounting differs significantly from accounting, and therefore accountants have to develop additional accounting registers.

Sources:

- Tax Code of the Russian Federation

- PBU 10/99, approved. by order of the Ministry of Finance of Russia dated May 6, 1999 N 33n

- PBU 9/99, approved. by order of the Ministry of Finance of Russia dated May 6, 1999 N 32n

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Revenue under the simplified tax system for 2021–2022

One of the main requirements regarding the possibility of using the simplified tax system by a company or individual entrepreneur is the established limit on the level of annual income.

Since 2022, two sets of limits have been in force for simplification, subject to which the payer retains the right to remain in the special regime:

- basic restrictions on income (150 million rubles) and the average number of employees (100 people) - allowing you to pay tax under the simplified tax system at regular rates;

- increased limits on income (RUB 200 million) and headcount (130 people) - making it possible to remain on the simplified tax system, but requiring the use of higher tax rates.

In 2022, the specified income limits apply without indexation, and from 2022 they are indexed. Taking into account the deflator coefficient of 1.096 established for 2022, the marginal incomes are:

- RUB 164.4 million for work at basic rates (150 x 1,096);

- RUB 219.2 million — maximum (200 x 1,096).

The procedure for accounting for income under the simplified tax system is determined by Art. 346.15, 346.17 Tax Code of the Russian Federation. Regarding their composition, paragraph 1 of Art. 346.15 refers to sec. 1 and 2 tbsp. 248 Tax Code of the Russian Federation. According to the text of these paragraphs, the amount of income under the simplified tax system is formed by the sum of income:

- from implementation;

- non-operating;

- from gratuitously received property or rights to it.

Income does not include receipts listed in Art. 251 Tax Code of the Russian Federation.

Revenue consists of sales (subclause 1, clause 1, article 248 of the Tax Code of the Russian Federation):

- manufactured products;

- work or services performed;

- previously purchased goods;

- property rights.

In the case of intermediary activities, income will be a commission or other remuneration (see, for example, letter of the Ministry of Finance of Russia dated April 18, 2018 No. 03-11-11/25816).

For the simplified tax system, income is recorded using the cash method (Article 346.17 of the Tax Code of the Russian Federation), which presupposes the actual receipt of money to the current account/cash, as well as the receipt of other property (work, services) and (or) property rights, repayment of debt (payment) in a different way.

Simplified income should be reflected in KUDIR. Samples from “ConsultantPlus” for the simplified tax system with the object “income” and with the object “income minus expenses” will help you design the book. You can watch materials for free by signing up for a trial access to K+.

For more information about the conditions that allow you to apply the simplified tax system, read the article “Procedure for applying the simplified taxation system” .