Concept of distributable income

Distribution of dividends is the prerogative of commercial organizations whose purpose of existence is to make a profit.

A dividend is a profit received for a certain period intended for distribution among the participants of this organization. Profit can be distributed in full or in part. In the Russian Federation, commercial firms are usually created in one of 2 forms:

- in the form of a joint-stock company (JSC), guided by the Federal Law “On Joint-Stock Companies” dated December 26, 1995 No. 208-FZ;

- in the form of an LLC, applying the Federal Law “On Limited Liability Companies” dated 02/08/1998 No. 14-FZ.

In the 1st of these laws, the concept of dividends is used in relation to the payment of income (Chapter V), and in the 2nd law there is no such concept, although the issue of profit distribution is discussed in it (Articles 28, 29 of Law No. 14-FZ) .

Both of these concepts (dividend and profit distribution) are united by Art. 43 of the Tax Code of the Russian Federation, which classifies as dividends any income received by a participant or shareholder as a result of the distribution of net profit in proportion to his share of participation.

Restrictions on dividend payments

In order to distribute dividends, the mere fact of profit is not enough. Both of the above laws contain lists of very similar restrictions (Article 43 of Law No. 208-FZ and Article 29 of Law No. 14-FZ), which apply not only to the date of the decision on payment, but also to the date of payment (if the situation has changed by the time of payment ).

Limitations common to both organizational forms:

- The management company must be paid in full.

- Net assets must exceed the sum of the authorized capital and reserve fund even after payment of dividends. For a joint-stock company, the amount of the excess of the value of preferred shares over their par value is also added to the amount of the authorized capital and reserve fund.

- Signs of bankruptcy must not occur or arise as a consequence of the payment of dividends.

A special restriction for an LLC: a decision on payment is not made until the actual value of the share (or part thereof) has been paid to the retiring participant.

According to the AO, a decision cannot arise:

- until the completion of the repurchase from shareholders of shares in respect of which there is a right to demand their repurchase (Clause 1, Article 75 of Law No. 208-FZ);

- without observing the correct sequence of making a decision on the payment of dividends: first in relation to those preferred shares that have special advantages, then on other preferred shares and only then on ordinary shares.

Both laws contain a clause that under an existing payment decision that has not been implemented due to restrictions that arose at the time of payment, the issuance of dividends is mandatory after the disappearance of these restrictions.

How are dividends distributed?

Everything is simple here. For example, I’ll take a joint stock company whose capital consists of 100 ordinary shares. At the General Meeting of Shareholders (GM), it was decided to pay dividends from the undistributed private equity in a total amount equal to 100 rubles, which means that for each security there will be 100/100 = 1 ruble (before taxes).

Using the same formula, you can calculate dividend flows in an LLC, only instead of ordinary shares, a specific % share of the funds of each individual founder invested in the authorized capital of the company will be used (for example, 50%/50%).

However, there are exceptions when payments are distributed not in proportion to shares, but according to specially established formulas (coefficients).

But this must be established by the company’s internal documents and confirmed in the minutes of the meeting, otherwise the distribution of funds will be classified as payments subject to additional deductions, for example, insurance premiums.

As a rule, dividends are accrued in non-cash form, but according to the law, securities or property may also be subject to distribution.

Frequency and methods of payment

In both forms (JSC and LLC), it is allowed to make a decision on the payment of dividends with a frequency of 1 time:

- per quarter;

- half year;

- year.

Quarterly and semi-annual distributions will be considered interim. The payment of such dividends is assessed accordingly.

IMPORTANT! Interim dividends remain dividends even if the profit at the end of the year is less than the amounts already paid in the form of dividends. There is no need to reclassify them as other income. This is important for tax purposes. Read more here.

A legal entity is not necessarily required to make a decision on the payment of income. There may also be a decision on non-distribution of profits, usually made at the end of the year.

Law No. 208-FZ directly lists the methods of paying dividends (in money or property), while Law No. 14-FZ does not indicate either the methods of payment or any restrictions on them. Thus, it is possible to pay dividends regardless of the form of the legal entity:

- cash from the cash register.

- by non-cash transfer to the participant’s bank account;

- property.

From the amount of accrued income, personal income tax (for an individual) or income tax (for a legal entity) must be withheld. For the calculation, a rate of 13% is used for residents (clause 1 of Article 224 and subclause 2 of clause 3 of Article 284 of the Tax Code of the Russian Federation) and 15% for non-residents, as well as for residents in case of payment of dividends in an amount exceeding 5 million rubles . in year. (clause 3 of article 224 and subclause 3 of clause 3 of article 284 of the Tax Code of the Russian Federation). The question of paying tax when paying dividends to a legal entity arises regardless of what taxation regime is applied by the organization that decided to issue them.

To learn how the tax on dividends paid to a legal entity is calculated, read the article “How to correctly calculate the tax on dividends?” .

For information on the taxation of dividends from individuals, see the material “Is personal income tax levied on dividends?”

ConsultantPlus experts explained in detail what tax reporting needs to be submitted on dividends paid. Get trial access to the legal system for free and go to the K+ Guide.

The specified rates are used in relation to dividends paid in 2022, regardless of the year for which they are paid and what rate was in effect in the year for which they were accrued. For an individual, this income is taken into account separately from other income taxed at the same rate. In the case of payment of dividends to a legal entity that owns more than 50% of the capital, the rate may be 0% (subclause 1, clause 3, article 284 of the Tax Code of the Russian Federation).

For information on what needs to be done to apply a 0% rate on dividends, read the article “How to justify a zero tax rate on dividend income”

The situation of issuing dividends with property is regarded as a sale (letter of the Ministry of Finance of Russia dated December 17, 2009 No. 03-11-09/405), entailing the payment of VAT and income tax from the transferring party. At the same time, the obligation to pay tax for the recipient of dividends is not relieved. Taxes are calculated based on the market value of the property. If there is no interdependence, this value is equal to the contractual value of the transfer. The issue of establishing the market value will be significantly complicated in the case of interdependence of persons (participation share of more than 20%) and the presence of constituent entities of the Russian Federation among the participants.

Features when paying dividends to foreign participants

Some residents of other countries may have preferential tax rates. Thus, for tax agents in England or Germany the rate is set at 10%, and for residents of Italy it is half as much and is only 5%.

Another important point is the functional aspect of possible double taxation.

Therefore, before paying part of retained earnings or current period income to a foreign participant, it is necessary to clarify whether an international agreement on this issue has been established between the Russian Federation and the resident country.

How is the payment decision made?

This decision is made by the general meeting:

- shareholders in the joint-stock company (clause 3 of article 42 of law No. 208-FZ).

- participants in an LLC (Clause 1, Article 28 of Law No. 14-FZ).

The financial statements for the relevant period must be ready for the meeting, their data must be analyzed to ensure compliance with the restrictions established for making a decision on payment, and the amount of profit that can be used to pay dividends must be determined.

The result of the meeting is a protocol, which, when executed by the JSC, must contain (clause 2 of Article 63 of Law No. 208-FZ) the following:

- time and place of the meeting;

- the total number of votes and votes of meeting participants;

- information on the election of the chairman and secretary;

- agenda;

- the results of consideration of each of the issues;

- final decision.

The listed data will not be superfluous in the protocol drawn up by the LLC.

With regard to dividends, the meeting of the joint-stock company must decide on the following points:

- for what period they are paid;

- total payment amount and size for each type of shares;

- the date on which the composition of shareholders will be determined;

- form and time of payment.

For LLCs, the following are excluded from this list:

- the amount of dividends for each type of shares;

- the date on which the composition of shareholders will be determined.

The distribution of the total amount between specific persons is carried out:

- in JSC - according to the algorithm laid down in the charter, depending on the types and number of shares;

- in an LLC - in proportion to shares, unless the charter contains a different order.

The general meeting is not held by the sole founder. It is enough for him to make a decision on the payment of dividends, formalizing it as any of his decisions, indicating the date of preparation and the essence of the issue on which the decision is being made.

How often can you make payments?

Accruals from both current income and retained earnings can be made exclusively based on the results of the reporting periods for which accounting is kept.

These are:

- quarter;

- half year;

- 9 months;

- year.

Is it possible to pay dividends using profits from previous years?

Expert opinion

Vladimir Silchenko

Private investor, stock market expert and author of the Capitalist blog

Ask a Question

Previously, the issue of accruals from retained earnings was quite widespread; the Ministry of Finance for some time even introduced restrictions on such actions. But since 2007, all special prohibition directives have been canceled and no further clarifications have been received.

Now I will return to the legislation, and more specifically to the source of the formation of dividends of the organization. And, as I indicated above, their source is the net profit of the company, but the period of its use is not indicated.

This means that the undistributed state of emergency of previous years of the company is legally also a full source for the formation of the dividend base.

For how many years can dividends for previous years be paid?

The urgency of the formation of the undistributed state of emergency of previous years does not play a role.

Dividend flows can be established at the expense of retained earnings, unless there are other legal restrictions related to the financial stability of the enterprise.

Terms of payment of dividends in LLC

For an LLC, the period for issuing dividends is limited to 60 days from the date of the decision (Clause 3, Article 28 of Law No. 14-FZ). A specific period within these 60 days may be established by the charter or a meeting of participants. If such a period is not recorded in the LLC documents, it is equivalent to 60 days.

Important! “ConsultantPlus” warns that if you violate the deadline for paying dividends, as well as if you do not pay them, the consequences may be different depending on whose fault the violation occurred. Read more about the consequences in K+ by getting trial demo access to the system.

Dividend tax 2022

Taxes on dividends to the founder in 2022 are calculated depending on who is paid to: an individual or an organization.

Payment of dividends to the founder - organization is subject to income tax. Moreover, the payer acts as a tax agent, that is, he must withhold and transfer the tax to the budget. As a general rule, the rate is 13% (clause 2, clause 3, Article 284 of the Tax Code of the Russian Federation). But if the owner owns at least half of the authorized capital for at least one year, then the rate is set at 0% (clause 1, clause 3, article 284 of the Tax Code of the Russian Federation).

Income paid to the founder - an individual - is subject to personal income tax at a rate of 13% if he is a resident of the Russian Federation. If the owner is a non-resident, then the transfer of part of the net financial result to him will be taxed at a rate of 15% (paragraph 2, paragraph 3, article 224 of the Tax Code of the Russian Federation).

The tax calculation does not depend on what dividend payment calendar is set for 2022. For each transfer, the tax is calculated separately, and not on an accrual basis from the beginning of the year. To calculate, use the formula:

If your company itself receives income from participation in affiliated companies, then they must be taken into account when calculating the tax on amounts paid to the founders:

Consequences of failure to pay dividends on time

Both laws provide the same procedure for situations of non-payment of dividends on time. They can be claimed by the participant within 3 years (or 5 years if this is stated in the charter) from the date:

- making a decision on payment to the JSC (clause 9 of Article 42 of Law No. 208-FZ).

- completion of the 60-day period in the LLC (Clause 4, Article 28 of Law No. 14-FZ).

If dividends are unclaimed at the end of these periods, they are returned to profit and claims for them are no longer accepted.

The legislation does not provide for any sanctions for exceeding the deadline for paying dividends. The consequences may be that the participants go to court demanding the payment of not only dividends, but also interest for the delay in their transfer. If it is proven that the JSC that accrued the dividends opposes their payment, then a fine is possible under Art. 15.20 of the Code of Administrative Offenses of the Russian Federation in the amount of:

- from 20,000 to 30,000 rub. for officials;

- from 500,000 to 700,000 rubles. for legal entities.

For information on the rules for reporting dividends in the 6-NDFL report, read the material “How to correctly reflect dividends in the 6-NDFL form?”

What to consider when drawing up the founder’s decisions

On December 25, 2019, the judicial practice of the Supreme Court of the Russian Federation was published, which clarified the procedure for confirming the legality of the minutes of meetings of all founders. Key conclusions also apply to decisions of the sole owner:

- any decision must be certified by a notary or other means;

- the notary is present when decisions are made, or the sole participant himself visits the notary to formalize the decision (this option is very expensive);

- another method of identification is prescribed in the Charter and is used without restrictions.

We recommend taking into account current practice and making changes to the Charter. Otherwise, the decision to pay dividends may be declared invalid.

Results

The period for paying dividends in an LLC is 60 days from the date of the decision to pay them, unless a different period is established by the charter or meeting of the company’s participants. In a JSC, the period for paying dividends depends on the recipient: 10 days from the date of the decision for payment to nominee holders and trustees, and 25 days for payment of dividends to other shareholders.

Sources:

- Tax Code of the Russian Federation

- Law of 02/08/1998 N 14-FZ “On Limited Liability Companies”

- Law of December 26, 1995 N 208-FZ “On Joint Stock Companies”

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

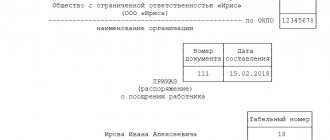

Sample order for payment of dividends to founders

If you are tasked with creating an order for the issuance of dividends that you have never dealt with before, look at the sample below and take into account our recommendations - this way you will easily create the order you need.

- The beginning of the document should not cause any difficulties: indicate here the name of the enterprise (full or abbreviated, it makes no difference), the name and number of the order (according to internal document flow), the date and place where the order was issued.

- Next, add a justification to the order - here you need to enter the reason why dividends are paid (for example, in connection with the end of the calendar year), then the basis, that is, a link to an article of law or an internal regulatory act of the company.

- After this comes the main section. Everything here is purely individual: the number of points and their wording. Be sure to note the period for which the owners of the company are paid their income (it is better to indicate the start and end dates), last names, first names, patronymics of the owners of LLC shares and the amount due to each of them.

- After this, enter the form of payment (cash or non-cash transfer to a bank card), as well as the period within which this must be done. If you consider it necessary, supplement the form with other information that is important in your particular case (for example, information about applications).

- Finally, designate the person responsible for the execution of this order and provide the necessary signatures.