Organizations offering insurance services are required to maintain accounting records. Their activities are controlled by the insurance market department that exists under the Central Bank.

Question: How are the costs of insuring property (including leasing and rented property) reflected in accounting and tax accounting? The organization entered into a property insurance contract for a period of 12 months (365 days) and paid a lump sum insurance premium in the amount of 146,000 rubles. The insurance contract is valid from March 1 of the current year (the date of payment of the insurance premium) to February 28 of the next year inclusive. For tax purposes, income and expenses are accounted for on an accrual basis. Reporting periods for income tax are the first quarter, half a year, and nine months of the calendar year. Interim financial statements are prepared on the last day of each quarter. View answer

Primary documents

Primary documentation is the papers on the basis of which accounting is carried out. Primary information for an insurance organization:

- Founding papers: charter, license.

- Insurance contracts.

- Papers confirming the occurrence of the event (application, insurance certificate).

- Papers confirming coverage of losses.

- Tax accounting registers.

The insurance company needs to approve the document flow schedule and document forms that are necessary for accounting needs.

the insurance premium reflected in accounting when terminating a compulsory motor liability insurance contract ?

How to reflect car insurance in accounting

Any company that owns a car, in addition to the costs of maintaining it, also incurs costs for insurance. When we talk about car insurance, we mean 3 types of insurance: OSAGO, DSAGO and CASCO.

With CASCO insurance, insurance companies undertake to reimburse the policyholder for the costs of restoring the car in the event of an accident or to pay the cost of the car in the event of its theft. Moreover, regardless of whose fault the accident occurred in which the car was damaged. This type of insurance is only voluntary. The compulsory type of car insurance is compulsory motor liability insurance. This insurance contract indemnifies damage that may be caused to third parties.

But it happens that the established limit of compensation under compulsory motor liability insurance is not sufficient to cover the losses of the injured party. Therefore, there is another type of voluntary auto insurance - DSAGO. For any type of insurance, a contract is concluded. The organization must keep this type of agreement for 5 years.

Sometimes, to conclude a contract, it is necessary to undergo a technical inspection and obtain a diagnostic card.

The costs of passing a technical inspection are reflected by posting:

- D20 (26) K60 – costs for technical inspection were expensed

The receipt of the policy must be taken into account in an off-balance sheet account, for example account 13 “OSAGO, DSAGO, CASCO policies”, posting:

- D13 – policy taken into account

Calculations for car insurance in the organization’s accounting must be reflected in account 76-1 “Calculations for property and personal insurance.”

Accounting for payments under basic agreements with policyholders

The organization makes insurance payments when insured events occur. They may relate to various areas:

- Property (payments are made in cases of theft, flooding and other damage).

- Medicine (payments in case of illness).

- Auto (payments in case of car theft).

How is accounting carried out when insuring the leased asset by the lessee (sublessee)?

Insurance payments are formed from the totality of all proceeds from people who have entered into an insurance agreement with the organization. Payments are recorded on account 22. Information about them is collected in registers. Analytical accounting is carried out in the context of agreement forms and policyholders. Information is recorded in accounting on the date of occurrence of insurance rights.

How to reflect insurance costs in 1C

It is easier to display insurance costs and payment amounts in the 1C database; an example is the purchase of a CASCO policy. The management of the driving school “Behind the Wheel” issued a CASCO policy on October 23, 2019 for a year at a cost of 5,700 rubles. The payment transaction is displayed in the documentation under the item “Write-off from current accounts.” Select “Other write-offs” with posting D76 as the type for the operation. 01 K51.

Related article: Liability insurance under contract

The premium amount must be written off monthly in equal payments; they are reflected in the “Receipt of services and goods” section with the transaction type “Services”. It is important to indicate the policy and current account number along with the counterparty. The table indicates the account to be written off, the type of service and each amount. Knowing how to properly write off insurance, an accountant will be able to keep records throughout the entire policy period.

Accounting for bonuses

Insurance premiums are payments made by a person to an organization. The insurance agreement comes into force either from the date specified in it or from the date of payment of the first premium.

How is accounting carried out when insuring cargo by the shipper ?

Compensation in the event of an insurance event is paid only when the person has no arrears on premiums. All amounts for the past period must be paid.

The compensation paid to the insured may be counted towards the following insurance premiums.

Let's look at an example. The insured person was awarded compensation in the amount of 50,000 rubles. Additional expenses associated with the insured event were also confirmed. The person decided to use half of this amount towards future insurance payments. In this case, these postings are used:

- DT22/1 KT51. Payment of insurance compensation.

- DT22/1 KT51. Payment of additional expenses.

- DT22/1 KT77/1. Crediting part of the indemnity amount against the following insurance premiums.

The legality of all payments is confirmed by the primary source.

Features of transactions under an insurance contract

Accounting entries in the insurance industry are records in a single computer database. They are needed to display changes in the state of accounting objects - policyholder premiums. Data on the policy can be taken into account and recorded starting from the day when it is considered valid. The legislative framework does not have a uniform accounting procedure for expenses on insurance services; they can be attributed to expenses once or adjusted throughout the entire period of insurance. At the same time, only the actual paid part of the premium is included in expenses. When the amount is paid in part, the premium is calculated not for the entire period, but for the period already paid.

Important! The amount of the insurance premium is present in the insurance policy and is calculated according to tariff rates adopted by the insurer or supervisory authorities. If the contract is terminated early or an insured event occurs, the amount of compensation is displayed in the accounting database.

Postings in accounting and tax accounting are divided into two parts: debit and credit. In the second, subaccount 76-1 is indicated when the policyholder is a legal entity. The debit account includes accounts for basic expenses and other expenses, if it concerns a one-time write-off.

Related article: What documents confirm the conclusion of an insurance contract

With each type of write-off, discrepancies arise between accounting and tax information:

- In accounting, write-offs occur immediately and throughout the full insurance period. In NU, the premium will be written off once only for insurance that is valid within a single reporting period for income tax.

- Costs in BU are taken into account in full; NU contains tariff frameworks for all insurance products.

- In BU, the display of expenses begins from the day when the policy begins to operate according to the law; in NU, it is recorded from the moment the policyholder makes payment.

To insure a car and other vehicles, they use a unified account system with the number 76-1.

Property insurance accounting

Property insurance can be voluntary or mandatory; this insurance product is on the list of the most common. Transactions under a property insurance contract are recorded on a standard account with number 76-1. If the premium amount has already been paid, it is fixed in this way - D76-1 K51. Property insurance costs are calculated from the date the policy comes into force. When it is not provided, the insurance is recognized as valid after payment of the premium. After taking into account all costs, postings of type D20 (26) K97 (76-1) are entered into the database.

Accounting for expenses for OSAGO and CASCO policies

Motor vehicle insurance costs are considered as expenses for standard types of activities. Accounting for CASCO or OSAGO in BU and OSNO is carried out using account number 76-1, as for policies for property type of insurance. For MTPL policies for a car with a period of more than 1 month, wiring numbered D20 (26) K76-1 is used, less than a month - D20 (26) K76-1. In the event of termination of a CASCO or MTPL policy before expiration, the insurer is obliged to return part of the amount to the policyholder, and the accounting entry will look like this: D51 K76-1. After the auto insurance policy is written off, it is recorded in the database using the K13 posting.

Article on the topic: Termination of an insurance contract and return of money to IC "Rosgosstrakh"

Reflection in accounting of insurance for employees

Employees of different companies most often receive medical insurance from their employer. This insurance is regarded as a voluntary type; the costs of such contracts can be recorded on account number 76-1. At the time of payment of the premium amount, a posting numbered D76-1 K51 is added. For contracts with a term of more than a month and expense data included in the list of costs, posting of the type D20 (26) K76-1 is used. If we are talking about a policy with a term of no more than a month, then the payment amount is taken into account in the list of costs by another entry D20 (26) K76-1.

Accounting for reinsurance

Reinsurance is the transfer of obligations to protect against risks. It is assumed that these obligations are transferred from one organization to another. That is, a person enters into an agreement with one organization. She will be considered the primary insured. It is she who is responsible to clients. She also accepts various insurance claims.

If reinsurance is carried out, these transactions become relevant:

- DT92/4 KT77/4. Premium aimed at reinsurance.

- DT77/4 KT91/1. Money received from the reinsurer.

- DT77/4 KT77/6. Money deposited under agreements submitted to reinsurance.

The reinsurance agreement is a separate contract. The reinsurer makes payments only in the amounts established by the contract. Amounts above the limit are paid by the primary insurer.

Voluntary property insurance

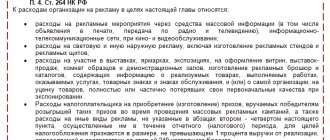

A specific list of expenses classified as expenses for voluntary property insurance is given in Article 263 of the Tax Code of the Russian Federation.

Expenses for the listed types of voluntary insurance are included in other expenses when calculating income tax in the amount of actual expenses.

EXAMPLE 3. WE INSURANCE “PRO STOCK”

LLC “Pagoda” carried out voluntary insurance of inventory. The costs for this type of insurance amounted to 38,500 rubles. Since the costs for voluntary insurance of inventory are listed in Article 263 of the Tax Code of the Russian Federation, these costs are taken in full when calculating income tax.

The letter of the Ministry of Finance of Russia dated December 8, 2017 No. 03-03-06/1/81913 states that if insurance of business and financial risks is a prerequisite for the taxpayer to carry out its activities, provided for by the legislation of the Russian Federation, then such expenses can be included in the tax base when calculating corporate income tax.

And a very interesting additional clarification can be provided by the letter of the Federal Tax Service of the Russian Federation dated October 15, 2009 No. 3-2-09 / [email protected] “On accounting for insurance premiums for profit tax purposes.”

Thus, it states that if the customer or authorized body has established a requirement to ensure the execution of a state or municipal contract, then insurance premiums under a liability insurance agreement under the above contract can be taken into account as expenses for profit tax purposes on the basis of subparagraph 10 of paragraph 1 of Article 263 of the Tax Code of the Russian Federation provided that the tender documentation does not exclude this type of contract security.

That is, it turns out that formally the taxpayer can carry out any type of insurance voluntarily, the main thing is that this condition is prescribed by the counterparty as mandatory for the execution of the contract.

If the type of insurance is not named in the list given in the Tax Code of the Russian Federation, then it will not be possible to accept expenses for tax accounting.

EXAMPLE 4. WE INSURE “RESPONSIBLY”

LLC “Amazon” decided to insure the civil liability of the owner of a dangerous facility for causing harm not to victims, but to the environment as a result of an accident at a dangerous facility. The expenses incurred will not be accepted for the purpose of calculating income tax, since this type insurance is not mentioned in Article 263 of the Tax Code of the Russian Federation (letter of the Ministry of Finance of Russia dated January 18, 2016 No. 03-03-06/1/1119, etc.).

Accounting for payments under coinsurance agreements

A person may enter into insurance agreements with several organizations. In this case, the companies will be jointly and severally liable to the person in the event of an insured event. That is, each organization contributes a certain share. There are 2 options for drawing up an agreement:

- The person enters into separate agreements with each company. Calculations are carried out by each organization separately.

- All operations are carried out by one organization, which acts on behalf of others.

If agreements are concluded with each organization separately, these postings are used:

- DT77/1 KT92/1. Calculation of insurance premium.

- DT51 KT77/1. Payment of the premium.

- DT22/1 KT77/1. Calculation of payment upon the occurrence of an insured event.

- DT77/1 KT51. Transfer of payment.

If settlements are carried out by one organization, accounting is carried out by each insurance company. Accounting reflects amounts proportional to the organization's share.

How to reflect property insurance in accounting

The most common forms of insurance are insurance against the risk of loss or damage to specific property. After concluding a property insurance contract, an insurance policy is issued. In this case, property insurance is carried out at the actual insurable value, but not higher than the sale price, or based on the prices in force at the time of acquisition of this property.

Property insurance can be either voluntary or mandatory. However, in general, this type of insurance is not included in the list of compulsory types of insurance, except for cases provided for by law. Calculations for property insurance, as well as car insurance, are reflected in account 76-1.

On the date of payment of the insurance premium, the following must be recorded in accounting:

- D76-1 K51 – insurance premium paid

Insurance costs are recognized on the date on which the contract becomes effective. If the date is not provided, then it comes into effect from the moment the insurance premium is paid. When an insurance contract is concluded for a period of more than 1 month, costs are written off monthly throughout the entire insurance period.

Accounting for liability insurance

Liability insurance involves compensation for damage caused by the insurer to a third party. For example, a person received insurance in case of apartment flooding. And then he flooded his neighbor's apartment. In this case, the insurance company compensates for the damage caused to this neighbor. Let's look at other common cases of liability insurance:

- Damage caused to someone else's vehicle during its operation.

- Damage caused to the environment or people due to potentially hazardous activities.

- Damage caused to third parties in connection with the performance of legal or medical activities.

Let's look at the entries made for liability insurance (example):

- DT22/1 KT51. Payment of damages to a person injured in a car accident.

- DT91/2 KT22/1. The payment is included in the spending structure.

- DT50 KT91/1. Receipt of money from a person found guilty of an accident.

FOR YOUR INFORMATION! You can insure business risks. In this case, the insurance agreement ends early upon termination of business activity.

How to reflect employee insurance in accounting

Providing health insurance for employees of an organization is one of the ways to show concern for staff. Moreover, such concern is encouraged at the legislative level by providing such companies with various tax breaks. At the initiative of the employer, health insurance contracts can be issued for employees. In this case, insurance is considered voluntary.

Settlements for such insurance are also carried out on account 76-1. On the date of payment of the insurance premium, the following entry is made:

- D76-1 K51 – insurance premium paid.

At the same time, also, in the case when the contract is concluded for a period of more than one month, costs are written off monthly during the entire term of the contract:

- D20(26) K76-1 – insurance costs are included in costs.

If the contract is concluded for a period of no more than one month, expenses are taken into account as expenses in the month when the contract was concluded or the insurance was paid:

- D20(26) K76-1 – insurance costs are included in costs.

Example of insurance reflection

decided to insure its employees and entered into a contract of voluntary medical insurance for employees from 05/25/2017 to 05/24/2022 (period of 365 days), paying an insurance premium of 25,000.00 rubles. On the day the insurance is issued, the following is posted:

| date | Business transaction | Debit | Credit | Amount, rubles |

| 05/24/2017 | Payment of insurance premium | 76-1 | 51 | 25000,00 |

| 05/31/2017 | Insurance expenses written off | 26 | 76-1 | 25000.00/365days*7days = 479.45 |

And then at the end of each month, insurance costs are written off until the end of the contract.

Features of VHI accounting

VHI is one of the types of personal insurance. As a rule, it is included in the “social package” provided by the employer. Contributions for voluntary health insurance are included in expenses if there are circumstances specified in subparagraph 16 of article 255 of the Tax Code of the Russian Federation. Consider these circumstances:

- The VHI agreement is signed for a period of more than a year.

- The insurance company has a license to conduct insurance activities.

- Expenses are fixed at no more than 6% of total labor costs.

In accounting, expenses for voluntary health insurance relate to the period in which they arose. Insurance payments are recorded on the DT of expense accounts (for example, account 20, 26, 44). The company may make insurance payments for persons with whom labor relations have not been formalized. Related expenses will be recorded on DT 91. A subaccount 02 will be opened for it.

Accounting for transactions under voluntary insurance contracts

To summarize information on calculations for voluntary insurance of employees of an organization by the Chart of Accounts of financial and economic activities of organizations and the Instructions for its application, approved by Order of the Ministry of Finance of the Russian Federation dated October 31, 2000 No. 94n “On approval of the chart of accounts for financial and economic activities of organizations and instructions for its application" is intended for account 76 "Settlements with various debtors and creditors", subaccount 76-1 "Settlements for property and personal insurance".

Payment of insurance premiums to the insurance company is reflected in the debit of account 76 “Settlements with various debtors and creditors”, subaccount 76-1 “Settlements for property and personal insurance” in correspondence with cash accounts.

Based on paragraphs 7, 8 of PBU 10/99, approved by Order of the Ministry of Finance of the Russian Federation dated May 6, 1999 No. 33n “On approval of the accounting regulations “Organization expenses” PBU 10/99” (hereinafter referred to as PBU 10/99), expenses for voluntary insurance of employees may be related to expenses for ordinary activities and are included in the cost of products (works, services) or as part of sales expenses. At the same time, according to paragraph 18 of PBU 10/99, the organization’s expenses are recognized in the reporting period in which they occurred, regardless of the time of actual payment of funds and other form of implementation (assuming the temporary certainty of the facts of economic activity). The traditional period for concluding a voluntary insurance contract is 1 year. If a voluntary insurance agreement is concluded for a period of 12 months, expenses for it are recognized monthly in the amount of 1/12 of the amount of the insurance premium.

Information on expenses incurred in a given reporting period, but relating to future reporting periods, is summarized on account 97 “Future expenses”. Expenses recorded on account 97 “Deferred expenses” are written off by organizations as a debit to cost accounts.

The accrual of the amount of insurance compensation due under an insurance contract to an employee of an organization in the event of an insured event is reflected in accounting according to the Chart of Accounts:

Debit of account 76 “Settlements with various debtors and creditors” subaccount 76-1 “Settlements for property and personal insurance”

Credit to account 73 “Settlements with personnel for other operations”

The amounts of insurance compensation received by the organization from insurance organizations, in accordance with insurance contracts, are reflected:

Debit account 51 “Current accounts”

Credit account 76 “Settlements with various debtors and creditors” subaccount 76-1 “Settlements for property and personal insurance”

In practice, in most cases, payments of insurance compensation to the victim are made without the participation of the policyholder, and the insurance amount is paid by the insurer directly to the insured.

Example 1.

In January, a production organization entered into an agreement with an insurance company for voluntary accident insurance for its employees for a period of one year. The insurance premium, in accordance with the terms of the contract, is paid by the organization at a time in the amount of 54,000 rubles. In July, as a result of an insured event, one of the employees received an insurance payment in the amount of 6,800 rubles. The specified amount is transferred by the insurance organization to the organization's current account and issued to the insured employee from the organization's cash desk.

Let's consider the reflection of transactions in the accounting records of an organization:

Accounting entries for January.

| Account correspondence | Amount, rubles | Contents of operation | |

| Debit | Credit | ||

| 76-1 | 51 | 54 000 | The amount of the insurance premium was transferred to the insurer |

| 97 | 76-1 | 54 000 | The amount of the insurance premium is reflected in deferred expenses |

| 20 | 97 | 4 500 | Reflected as part of insurance expenses related to the current month (RUB 54,000: 12) |

| 76-1 | 73 | 6 800 | The amount of insurance compensation has been calculated |

| 51 | 76-1 | 6 800 | Received funds from the insurance company to pay the insured person |

| 73 | 50 | 6800 | Insurance compensation was paid to an employee of the organization |

End of the example.

Example 2.

On January 6, the organization entered into a voluntary health insurance agreement for 1 year (366 days). The insurance premium for the year amounted to 20,000 rubles for each of the 15 employees. Insurance premiums were paid in a one-time payment on January 6.

To legally write off insurance premiums, the organization must calculate their amount for January.

It amounted to 21,369.86 rubles (20,000 rubles x 15 people / 365 days) x (31 days - 5 days)).

Let's calculate the amount for the remaining months of the current year.

It amounted to 24,956.41 rubles (20,000 rubles x 15 people / 365 days) x (365 days -31 days) / 11.

| Account correspondence | Amount, rubles | Contents of operation | |

| Debit | Credit | ||

| 76-1 | 51 | 300 000 | The insurance premium was transferred to the insurer (20,000 rubles x 15 people) |

| 97 | 76-1 | 300 000 | The insurance premium is charged to deferred expenses |

| 44 | 97 | 21 369,86 | Insurance premiums for January of the current year have been accepted for accounting |

| 44 | 97 | 24 956,41 | Insurance premiums for February of the current year have been accepted for accounting |

| 44 | 97 | 24 956,41 | Insurance premiums for March of the current year have been accepted for accounting |

| 44 | 97 | 24 956,41 | Insurance premiums for April of the current year have been accepted for accounting |

| 44 | 97 | 24 956,41 | Insurance premiums for May of the current year have been accepted for accounting |

| 44 | 97 | 24 956,41 | Insurance premiums for June of the current year have been accepted for accounting |

| 44 | 97 | 24 956,41 | Insurance premiums for July of the current year have been accepted for accounting |

| 44 | 97 | 24 956,41 | Insurance premiums for August of the current year have been accepted for accounting |

| 44 | 97 | 24 956,41 | Insurance premiums for September of the current year have been accepted for accounting |

| 44 | 97 | 24 956,41 | Insurance premiums for October of the current year have been accepted for accounting |

| 44 | 97 | 24 956,41 | Insurance premiums for November of the current year have been accepted for accounting |

| 44 | 97 | 24 956,41 | Insurance premiums for December of the current year have been accepted for accounting |

| 44 | 97 | 4 109,63 | Insurance premiums for January of the following year have been accepted for accounting |

End of the example.

For more detailed information on issues related to deferred expenses, you can read the book by the authors of BKR-INTERCOM-AUDIT JSC “Deferred Expenses”.

Accounting for transactions under a voluntary cargo insurance agreement

In accordance with paragraph 2 of PBU 5/01, approved by Order of the Ministry of Finance of the Russian Federation dated June 9, 2001 No. 44n “On approval of the accounting regulations “Accounting for inventories” PBU 5/01” (hereinafter referred to as PBU 5/01), goods are part of inventories acquired or received from other legal entities or individuals and intended for sale.

According to paragraph 5 of PBU 5/01, inventories are taken into account at actual cost. In accordance with paragraph 6 of PBU 5/01, the actual cost of inventories purchased for a fee is recognized as the amount of the organization's actual costs for the acquisition, with the exception of value added tax and other refundable taxes.

Actual costs include:

— amounts paid in accordance with the contract to the supplier (seller);

- amounts paid to organizations for information and consulting services related to the acquisition of inventories;

- customs duties;

- non-refundable taxes paid in connection with the acquisition of a unit of inventory;

- remunerations paid to the intermediary organization through which inventories were acquired;

— costs of procurement and delivery of inventories to the place of their use, including insurance costs . In our case, these are the costs of cargo insurance.

Example 1.

An organization whose main activity is wholesale trade purchased a consignment of goods worth 120,000 rubles (including VAT). For the delivery of goods, a contract for transport and forwarding services was concluded. One of the terms of the contract is to insure the customer’s goods at his expense by concluding an agreement with an insurance organization. The cost of services of a transport organization for the delivery of goods is 4,800 rubles (including VAT), Insurance costs are 7,000 rubles. The insurance policy issued by the insurance organization states that the insured is the transport organization, and the beneficiary is the organization that purchased the goods. The debt to the supplier of goods and the transport organization is repaid from the organization's current account.

This transaction will be reflected in the accounting accounts as follows.

| Account correspondence | Amount, rubles | Contents of operation | |

| Debit | Credit | ||

| 41-1 | 60 | 101 694,92 | The received goods have been received |

| 19-3 | 60 | 18305,08 | VAT is reflected on goods received |

| 41-1 | 76 | 4 067,80 | Transportation costs are included in the price of the goods |

| 19-3 | 76 | 732,20 | VAT reflected on transport costs |

| 41-1 | 76 | 7 000 | Insurance costs are included in the price of the goods |

| 60 | 51 | 120 000 | Payment has been made to the supplier of the goods. |

| 76 | 51 | 11 800 | Payment has been made to the transport organization for delivery and insurance of the goods. |

| 68 | 19-3 | 19037,28 | Accepted for VAT crediting on goods and transport services |

In the example under consideration, the cost of the goods will be 112,762.20 rubles (101,694.92 + 4,067.80 + 7,000).

End of the example.

As for fixed assets, based on paragraph 12 of PBU 6/01 “Accounting for fixed assets”, approved by Order of the Ministry of Finance of Russia dated March 30, 2001 No. 26n, their initial cost includes the actual costs of the organization for delivery and bringing the fixed asset into use for use condition. According to paragraph 8 of PBU 6/01, the cost of fixed assets is allowed to include other costs associated with their production and acquisition. Based on these points of the PBU, we can say that the costs may also include the costs of cargo insurance.

In the chart of accounts for the financial and economic activities of organizations, approved by Order of the Ministry of Finance of Russia dated October 31, 2000 No. 94n, for insurance settlements, account 76, subaccount 1 “Calculations for property and personal insurance” is provided.

Example 2.

The organization purchased a refrigerated cabinet on November 10 at a price of 410,000 rubles. (excluding VAT) and insured it for the period of transportation. An insurance premium of 900 rubles was paid to the insurance company on November 11. The cabinet was delivered to the site and put into operation on November 17. Transportation cost the organization 15,000 rubles.

The following entries were made in the organization's accounting:

| Account correspondence | Amount, rubles | Contents of operation | |

| Debit | Credit | ||

| 08 | 60 | 410000 | The cost of the refrigerator is reflected |

| 08 | 76 | 900 | The amount of the insurance premium is reflected |

| 76/1 | 51 | 900 | Insurance premium paid |

| 08 | 60 | 15000 | The cost of transportation is reflected |

| 01 | 08 | 425900 | The refrigerator has been put into operation |

The cost of the refrigerator was (410000+900+15000) = 425900 rubles.

End of the example.

Accounting for voluntary vehicle insurance transactions

In accounting, according to paragraph 5 of PBU 10/99, expenses the implementation of which is associated with the performance of work or provision of services are expenses for ordinary activities. Consequently, the organization's expenses for vehicle insurance are classified as expenses for ordinary activities.

According to paragraph 18 of PBU 10/99, expenses are recognized in the reporting period in which they occurred, regardless of the time of actual payment of funds and other form of implementation (assuming the temporary certainty of the facts of economic activity). In this case, the conditions specified in paragraph 16 of PBU 10/99 must be met.

In accordance with paragraph 65 of the Regulations on maintaining accounting and reporting, approved by Order of the Ministry of Finance of the Russian Federation dated July 29, 1998 No. 34n “On approval of the regulations on maintaining accounting and financial reporting in the Russian Federation,” expenses incurred by the organization in the reporting period, but relating to the following reporting periods are reflected in the balance sheet as a separate item as deferred expenses and are subject to write-off in the manner established by the organization (uniformly, in proportion to the volume of production) during the period to which they relate.

Therefore, if the insurance contract is concluded for a period that exceeds 12 months, the amount of the insurance premium should be taken into account as deferred expenses. They should then be written off monthly in equal installments to cost accounts.

Example 3.

On April 15, the organization voluntarily insured its own VAZ-2107 car against theft. The contract period is 12 months (from April 15 of the current year to April 15 of the next year inclusive). The amount of the insurance payment under the voluntary insurance agreement is 15,000 rubles, which was transferred on April 15 of this year.

Reflection of transactions in accounting that were carried out on April 15 of the current year:

| Account correspondence | Amount, rubles | Contents of operation | |

| Debit | Credit | ||

| 76-1 | 51 | 15000 | Insurance premium transferred |

| 97 | 76-1 | 15000 | The insurance premium is taken into account as part of future periods |

Let's calculate the partial costs of car insurance on April 30 of the current year:

| Account correspondence | Amount, rubles | Contents of operation | |

| Debit | Credit | ||

| 26 | 97 | 666,66 | Voluntary insurance expenses were partially written off (15,000 rubles/12 months x 16 days/30 days) |

Monthly from May of the current year to March of the next year inclusive:

| Account correspondence | Amount, rubles | Contents of operation | |

| Debit | Credit | ||

| 26 | 97 | 1250 | Vehicle insurance costs written off |

On April 14 of the following year, an accounting entry was made in the accounting records:

| Account correspondence | Amount, rubles | Contents of operation | |

| Debit | Credit | ||

| 26 | 97 | 583,34 | The costs of voluntary insurance of the vehicle were partially written off (15,000 rubles/12 months x 14 days/30 days) |

End of the example.

Note!

If the vehicle is stolen or the like, then the voluntary insurance contract is terminated. In accounting, a transaction is reflected in the amount of insurance payments that were reflected in account 76 or 97 and are not included in expenses:

Debit account 99 “Profits and losses” subaccount “Extraordinary expenses”

Credit to accounts 76 “Settlements with various debtors and creditors”, 97 “Deferred expenses” - the amount of insurance premiums not included in expenses on the date when the car was stolen is written off.

ACCOUNTING OF OPERATIONS FOR VOLUNTARY INSURANCE OF RISKS ASSOCIATED WITH CONSTRUCTION AND INSTALLATION WORK

Based on clause 11 of the Accounting Regulations “Accounting for Agreements (Contracts) for Capital Construction” (PBU 2/94), approved by Order of the Ministry of Finance of the Russian Federation dated December 20, 1994 No. 167, the contractor’s costs consist of all expenses associated with the performance of contract work on agreement. In this regard, if construction and installation risks are insured, then such costs will be expenses for ordinary activities. On the basis of these expenses, the cost of construction work performed is formed, in accordance with paragraph 9 of PBU 10/99.

Moreover, according to paragraph 18 of PBU 10/99, expenses are recognized in the reporting period in which they occurred, regardless of the time of actual payment of funds. According to the tax authorities, if an organization transfers money to an insurance company under an agreement concluded, for example, for one year, then the expenses under such an agreement should first be reflected as deferred expenses, and then written off as expenses during the entire term of the agreement.

Based on paragraph 1 of Article 318 of the Tax Code of the Russian Federation (hereinafter referred to as the Tax Code of the Russian Federation), insurance expenses recognized in tax accounting in the reporting period are indirect expenses, that is, such expenses are fully attributed to the decrease in income of the reporting period, and they are not need to be distributed by type of work in progress.

Example 4.

The Contracting Organization entered into an insurance contract for construction and installation risks with an insurance company. The agreement was concluded on June 25 of the current year and is valid until June 24 of the next year inclusive.

Insurance premium in the amount of 48,000 rubles. paid in a lump sum on June 25 of the current year.

In June of the current year, the accountant should make the following entries in the Organization’s accounting:

| Account correspondence | Amount, rubles | Contents of operation | |

| Debit | Credit | ||

| 97 | 76/1 | 48000 | Insurance company debt accrued |

| 76/1 | 51 | 48000 | Insurance premium transferred to the insurance company |

| 20 | 97 | 800 | (48,000 rubles/12 months/30 days*6 days) expenses related to June of the current year are reflected. |

| 20 | 97 | 4000 | (RUB 48,000/12 months) part of the insurance costs relating to each subsequent reporting month was written off. |

| 20 | 97 | 3200 | (48,000 rubles/12 months/30 days*24 days) expenses related to June of the next year are reflected. |

End of the example.

If an insured event occurs, the organization must conduct an inventory of its property. The fact of the occurrence of an insured event is recorded in the insurance act.

Based on paragraph 9 of the Accounting Regulations “Income of the Organization” PBU 9/99, approved by Order of the Ministry of Finance of Russia dated May 6, 1999 No. 32n, income that arises as a consequence of emergency circumstances is considered extraordinary income. Such income may include:

· insurance compensation;

· the cost of materials remaining from the write-off of property unsuitable for restoration and use.

The expenses incurred in this case are reflected as part of extraordinary expenses (clause 13 of PBU 10/99).

Extraordinary income and expenses are written off to the profit and loss account (clause 11 of PBU 9/99, clause 15 of PBU 10/99.

If the organization has entered into an insurance agreement, then all losses from the occurrence of an insured event are reflected in account 76 “Settlements with various debtors and creditors” (subaccount 1 “Settlements for property and personal insurance”). It also reflects the amount of compensation received from the insurer. And only the balance on account 76 (subaccount 1 “Calculations for property and personal insurance”), and these are losses from insured events that are not covered by insurance compensation, are written off to account 99 “Profits and losses”.

The organization also needs to restore the “input” VAT on materials that were damaged as a result of an insured event (if the VAT on them was not reimbursed from the budget). The amount of this tax will be covered by insurance compensation.

Example 5.

The organization insured construction and installation risks, for which it paid the insurance company an insurance premium in the amount of 48,000 rubles.

As a result of the natural disaster, the construction site was flooded and construction materials worth RUB 600,000 were damaged. (VAT amount of 120,000 rubles on these materials was previously accepted for deduction).

When eliminating the consequences of a natural disaster, the costs amounted to 900,000 rubles, including:

— 400,000 rub. (VAT in the amount of 80,000 rubles was previously accepted for deduction) - use of various materials;

— 500,000 rub. — paid for the work of workers involved in eliminating the consequences of a natural disaster, including insurance contributions.

Insurance compensation was received from the insurance company - 1,400,000 rubles.

In the accounting records of the Organization, this operation is reflected in the following entries:

| Account correspondence | Amount, rubles | Contents of operation | |

| Debit | Credit | ||

| 76/1 | 10 | 600000 | The cost of damaged materials has been written off |

| 76/1 | 68/1 | 120000 | VAT on damaged building materials has been restored |

| 76/1 | 10 | 400000 | The cost of materials used in the liquidation of a natural disaster has been written off |

| 76/1 | 68/1 | 80000 | VAT has been restored on materials used in the liquidation of a natural disaster. |

| 76/1 | 70 | 500000 | The costs of remuneration of workers involved in liquidation are reflected |

| 51 | 76/1 | 1400000 | Insurance compensation received from the insurance company |

| 99 | 76/1 | 300000 | (1400000-600000-120000-400000-80000-500000) – the amount of loss from a natural disaster not covered by insurance compensation is written off. |

End of the example.

Hello Guest! Offer from "Clerk"

Online professional retraining “Chief accountant on the simplified tax system” with a diploma for 250 academic hours . Learn everything new to avoid mistakes. Online training for 2 months, the stream starts on March 1.

Sign up

Features of creating insurance reserves

The formation of insurance reserves is an event considered mandatory for an insurance company. The mandatory creation of such reserves is stipulated in Article 26 of Federal Law No. 4015-1 “On the Insurance Business” of November 27, 1992. The sequence of formation of reserves is specified in the order of the Ministry of Finance No. 51 n dated June 11, 2002.

Let's consider the sequence of formation of reserves:

- Establishing the required type of reserve. Orders of the Ministry of Finance 32n and 51n will help with this. You also need to focus on the local regulations of the company.

- Establishing a method for determining the reserve.

- Determination of the reserve for each insurance agreement.

The reserve is needed to ensure that the organization always has the amount of funds that is needed in the event of an insured event.