Employee bonuses are awarded as follows: types and sources

The reason for paying an employee an incentive such as a bonus may be:

- achievements of a labor nature, accomplished both by the work collective as a whole and by a specific employee personally;

- events that are not directly related to work activity, but caused by the intention to further reward the employee (for example, in connection with an anniversary or holiday).

For the reasons of the first group, the employer has the unconditional right to include bonuses in the salary structure (Article 129 of the Labor Code of the Russian Federation), and therefore take them into account as part of the payment for labor, i.e., attributing the accrued amounts of bonuses to the corresponding analytical expenses, which will reduce profit base.

It is quite difficult to include bonuses accrued on the grounds of the second group in your salary. The Ministry of Finance of Russia (letters dated 07/09/2014 No. 03-03-06/1/33167, dated 04/24/2013 No. 03-03-06/1/14283) insists on accounting for expenses on them at the expense of net profit.

Depending on the nature of the payments, bonuses can be:

- systematic (regular), the accrual and payment of which is carried out in compliance with the established frequency (once a month, quarter, year or other period of time);

- one-time (irregular), accrued and paid from time to time when an appropriate reason for payment arises.

Bonuses included in the salary structure may have both frequency patterns. But among them, as a rule, systematically paid incentives predominate. Bonuses not related to work achievements are usually one-time.

ConsultantPlus experts have prepared step-by-step instructions for assigning and processing bonuses to employees:

If you do not have access to the K+ system, get a trial online access for free.

Despite the presence of different sources for paying bonuses, bonuses will in any case constitute the employee’s income. And this income will need to be subject to personal income tax in the usual manner (clause 1 of article 210 of the Tax Code of the Russian Federation) and insurance contributions (clause 1 of article 420 of the Tax Code of the Russian Federation, clause 1 of article 20.1 of the law “On compulsory social insurance against accidents...” dated July 24, 1998 No. 125-FZ). Moreover, expenses for the purpose of calculating income tax can include not only those contributions that are accrued for bonuses included in the salary structure, but also those related to bonuses not related to work activities (subclause 49, clause 1, article 264 of the Tax Code of the Russian Federation, letter of the Ministry of Finance of Russia dated April 2, 2010 No. 03-03-06/1/220).

Read more about the taxation of bonuses in the material “What taxes and contributions are employee bonuses subject to?”

What is a bonus and why is a provision on bonuses for employees needed?

In accordance with Art. 129 of the Labor Code of the Russian Federation, wages are remuneration for work depending on the employee’s qualifications, complexity, quantity, quality and conditions of the work performed. The salary includes various additional payments and allowances of a compensatory nature (for example, for work in special climatic conditions, in areas exposed to radioactive contamination) and incentive payments (additional payments and allowances of an incentive nature, bonuses and other incentive payments). So, a bonus is an incentive payment that is paid for certain successes, results, achievements in work. Note that bonuses can be associated not only with labor results, but also with holidays and anniversaries, and can be one-time (for example, for a holiday) or regular (based on work results).

The employer must take into account that the bonus system must be understandable to employees: when, for what and in what amount they will receive a bonus. The indicators and conditions of bonuses, the size of bonuses, the frequency of their payment and other issues must be fixed in the bonus regulations. If it is compiled correctly, this will avoid:

- claims from tax authorities regarding the inclusion of bonuses in labor costs when calculating income tax;

- disputes with the Social Insurance Fund regarding the calculation of temporary disability benefits.

In addition, the provision on bonuses for employees will allow us to avoid describing the bonus system in the employee’s employment contract: the text simply makes reference to the provision on bonuses for employees and the employee becomes familiar with it before signing the employment contract.

Please note : by using a bonus system, you can save wages and reduce costs.

Bonus remuneration is usually set as a percentage of the employee's salary and in most organizations depends on performance indicators.

Let us highlight the basic principles of bonuses:

- Bonuses are awarded based on predetermined indicators.

- The size of the bonus should be related to the economic benefits that the employee brought to the organization.

- Accrual and payment of bonuses are made on the basis of an order from the head of the organization.

- The indicators, conditions and amount of bonuses are established by the head of the organization (otherwise the bonus indicators may be deformed and not correspond to the real goals of the company).

- The bonus is awarded for achieving each indicator separately.

- If the main bonus condition is not met, the bonus is not paid.

- The basis for calculating the bonus is the data of accounting and statistical reporting, and for indicators for which such reporting is not provided - operational accounting data approved by the relevant official.

- If performance indicators are not taken into account, bonuses based on performance results are not accrued or paid. Responsibility for the reliability of operational accounting data lies with the heads of the relevant departments, services, workshops, etc.

- The manager has the right, in individual cases, to increase the amount of the accrued bonus, but not more than by a certain fixed amount (as a percentage of the accrued bonus).

- The manager has the right to fully or partially deprive individual employees of bonuses for production omissions, a publicly available list of which must be established.

According to which document is the bonus procedure determined?

The employer must develop all aspects of the bonus system used by him himself, establishing them in an internal regulatory act (Article 135 of the Labor Code of the Russian Federation). This act can be created in the form of a separate document devoted only to bonus issues (provisions on bonuses, incentives, incentive payments). But it is also permissible to include the rules for calculating bonuses as an integral part in the texts of other internal documents devoted to issues of labor law:

- wage regulations;

- collective agreement;

- labor agreement.

A specially developed separate document (or part of a document devoted to issues of labor law) is convenient for reflecting the bonus payment procedure applied to the majority of members of the workforce. Its presence makes it possible not to specify in detail the rules for calculating bonuses in the employment agreement with each of the employees, but to provide in this agreement only a reference to the details of the corresponding document on the bonus procedure. Thus, the development of a normative act on bonuses makes it possible to include detailed rules for calculating this incentive in employment contracts only with those persons whose bonuses are paid on an individual basis.

The presence of an internal document on bonuses is mandatory:

- to include bonuses in the salary structure (Article 135 of the Labor Code of the Russian Federation);

- taking into account bonuses when calculating average earnings (Article 139 of the Labor Code of the Russian Federation).

The inclusion of bonuses in the salary structure makes them mandatory for payment when the conditions under which the remuneration should be accrued are met. At the same time, it is allowed to reflect in the bonus document the rules for paying bonuses that are not related to labor achievements.

The regulations on bonuses should cover issues related to:

- all types of remuneration applied by the employer;

- the conditions under which each type of bonus is accrued;

- frequency of accrual of incentive payments;

- the circle of persons entitled to each type of bonus;

- indicators by which the right of a particular employee to the corresponding type of remuneration is assessed;

- grounds that make it impossible to receive a bonus;

- systems for assessing indicators reflecting the right to receive an incentive payment, which makes it possible to convert the assessment of these indicators into ruble equivalent;

- the process of reviewing the results of assessing the labor contribution made by each employee;

- a procedure that allows you to challenge the results of the distribution of the bonus.

Starting from 2022, it is allowed not to develop internal acts devoted to issues of labor law and micro-enterprises (Article 309.2 of the Labor Code of the Russian Federation). However, in such a situation, the employer will have to spell out in detail all the bonus rules in each of the employment agreements, and the employment agreements themselves will have to be drawn up in a certain form. The form that must be used for these purposes is approved by Decree of the Government of the Russian Federation dated August 27, 2016 No. 858.

To learn how information about the accrued bonus can be included in an employment agreement, read the article “How to write a bonus in an employment contract - an example.”

Summary

Since there are no clear criteria in the legislation, when developing bonus regulations, it is necessary to determine how and for what the bonus is paid and how it may change depending on the financial situation and other circumstances.

If it is impossible to use quantitative indicators in the company’s activities, then the employer has the right to use only estimated indicators. Hello Guest! Offer from "Clerk"

Online professional retraining “Chief accountant on the simplified tax system” with a diploma for 250 academic hours . Learn everything new to avoid mistakes. Online training for 2 months, the stream starts on March 1.

Sign up

What can be used to calculate bonuses for employees when calculating salaries?

The process of calculating the bonus amount depends on:

- from the base taken as the basis of calculation;

- from the algorithm that determines the sequence of calculation of the base itself or its constituent parts;

- from the restrictions set for taking into account.

The calculation can be based on:

- fixed amount of remuneration;

- salary;

- actual accrued earnings;

- the sum of bonus indicators expressed in ruble equivalent, used to assess the employee’s contribution to the labor process.

All conditions affecting the calculation must be stipulated in the regulatory act on bonuses.

The accrual of a bonus in a fixed amount can occur in different ways depending on the conditions for recording the time of actual work in the bonus period, fixed in the procedure for calculating the bonus from the accrual base:

- The amount of bonuses does not depend in any way on the actual time worked, i.e., remuneration will always be accrued, even if the employee did not work at all in the period under review.

- When calculating the payment amount, the time of actual work in any of the ways established by the regulatory document is taken into account. For example, this amount is calculated:

- in proportion to the number of days (calendar or working) actually worked in the period;

- without accruing it for that month of the period that turned out to be not fully worked (for a quarterly bonus, for example, in such a situation you will need to apply one of the following coefficients: 1/3 or 2/3).

By setting salary or actual earnings as the calculation base, they immediately determine, expressed as a percentage, the amount of the share that will be the bonus accrued from the corresponding base.

A salary-based remuneration is essentially similar to a fixed-amount bonus and may or may not be dependent in the same way on the amount of time actually worked during the bonus period. It differs from a premium accrued in a fixed amount:

- mandatory application of the regional coefficient to the accrued amount if it occurs in the region of work;

- the need to choose a method for calculating bonuses for periods of salary changes, which could be, for example, establishing the obligation to take into account when calculating bonuses the updated salary amount: from the beginning of the period for which the calculation is made;

- from the period following the salary change;

- in the period of change, taking into account the proportion of the number of days (calendar or working) attributable to each salary.

For more information about the features of a bonus calculated from salary, read the material “How to calculate an employee’s bonus based on salary?”

For a bonus determined as a share of actual earnings, the issue of accounting or not accounting for time actually worked in the period is unimportant, since this time is already taken into account at the time of salary calculation. But the bonus rules will have to reflect the choice of the algorithm used for calculating actual earnings. You can calculate it, for example:

- summing up all actual wages accrued for the period, regardless of which component of the payment for labor it relates to;

- by determining (for a bonus period exceeding a month) the average monthly actual salary, including in its calculation all payments accrued for the period, regardless of their relationship to one or another component of payment for labor, and dividing the amount of these payments by the number of months in bonus period.

For the bonus base, established as the sum of bonus indicators expressed in ruble equivalent, which serve to assess the employee’s contribution to the labor process, the algorithm for calculating this base is itself simple and is determined as the sum of the ruble values of the corresponding indicators. But the calculation of the value corresponding to each of the indicators will depend on the evaluation system for this particular indicator and on the specific formula used to calculate its ruble value. Since both evaluation systems and formulas may turn out to be different, including those involving the use of a system of increasing (or decreasing) coefficients, the calculation of such a base will ultimately turn out to be difficult, although it will most realistically reflect the employee’s contribution to the results of the work of the entire team for the period.

How and by whom incentive payments are formed

How exactly to set wages and determine the size of bonuses in government agencies is regulated by the Labor Code of the Russian Federation, local regulations of a specific budget organization and departmental acts. Within a particular organization, a regulation is issued on the remuneration of employees, which provides for rules regarding bonuses. In particular, the provision must include:

- source of funding for the bonus fund;

- categories of specialists who are awarded;

- criteria for bonuses for employees of a budgetary institution;

- purpose of the bonus.

The provision must be agreed upon with the trade union organization of the budgetary institution (if there is one). After the publication of the regulations, a commission is formed in the institution consisting of the head, his deputy, representatives of the trade union and employees. The commission, through its protocols, makes substantive decisions on bonuses for employees. The procedure for bonuses in the public sector is based on the following principles:

- compliance of the assigned bonus with the employee’s salary, on the one hand, and the amount of work done by him, on the other;

- objectivity: when distributing bonuses, real merits must be taken into account in accordance with the criteria, the person of each employee is subject to a fair assessment;

- transparency: the commission’s conclusions and the criteria on which they are based must be available for review;

- predictability: every employee has the right to understand what bonus he will receive when performing a particular amount of work or criterion;

- timeliness: payments should not be delayed and paid immediately upon achieving the required result of work.

Read more: What to look for when developing a wage policy

IMPORTANT!

Bonuses are awarded to the head of a budgetary institution through the order of a higher organization to which the institution is subordinate.

How to calculate bonuses for additional pay and overtime

Additional payments and overtime are payments designed to compensate for the employee’s performance of labor functions under special working conditions. Their payment in all aspects is regulated by the provisions of the Labor Code of the Russian Federation. They are included in full in the salary, forming its compensation part (Article 129 of the Labor Code of the Russian Federation).

The question of calculating bonuses for additional payments and overtime can only arise if the basis for calculating the amount of bonuses is the actual earnings accrued for the period. Despite the fact that this earnings can, as already indicated above, be determined in different ways, it is calculated by taking into account all amounts accrued during the bonus period that form the salary, including additional payments and overtime.

If the bonus is set to be calculated from the salary, then additional payments and overtime will not be taken into account when calculating bonuses, since the calculation base here, by definition, forms only part of the accrued salary. When a bonus is awarded in a fixed amount or based on the sum of bonus indicators estimated in ruble equivalent, then it is not tied to salary at all and, accordingly, does not depend on it in any way.

To find out whether there are any restrictions on the amount of bonus paid, read the article “What can be the size of an employee’s bonus?”

What can a chief accountant be rewarded for?

The criteria for assessing the performance of accounting employees differ significantly from a similar list relevant for the chief accountant. The fact is that the work of the entire department directly depends on him. A specialist performs more complex tasks. The company's income and expenses directly depend on its activities. Therefore, it is necessary to carefully select criteria. The grounds for bonuses can be:

- timely preparation and submission of reports;

- there are no inaccuracies in the calculation and accrual of payments to employees;

- reducing the amount of accounts receivable;

- absence of errors when filling out reporting documentation or their minimum number;

- there are no monetary penalties from regulatory authorities or a minimum number of fines;

- reducing the organization's costs;

- during the reporting period, clients and contractors did not complain about the specialist’s work;

- positive result of tax optimization.

- The list can also be changed taking into account the personal needs of the company.

How to calculate a bonus taking into account the regional coefficient and northern bonuses

The regional coefficient and the northern bonus are additional payments of a compensatory nature, taking into account the fact of working in special climatic conditions. They also represent part of the salary that must be paid. The difference between them is that the regional coefficient is paid from the first day of work, and the right to receive the northern bonus and its increase depends on the length of work experience in the relevant area. The size of the coefficient and premium for each region is established by the Government of the Russian Federation, but at the regional level it is possible to increase these values (Articles 316, 317 of the Labor Code of the Russian Federation, Articles 10, 11 of the Law of the Russian Federation “On State Guarantees and Compensations...” dated 02/19/1993 No. 4520- 1).

It is necessary to increase the amount of the accrued bonus at the expense of the regional coefficient when bonuses are calculated from the salary and the corresponding coefficient is in force in the region. In all other cases, the issue of applying the coefficient remains unregulated by law. On the one hand, there is no need to charge a premium taking it into account, because:

- it is already taken into account in the earnings actually accrued for the period;

- the accrual of a bonus in a fixed amount or from the sum of bonus indicators estimated in ruble equivalent is not tied to the salary, which requires an increase by the corresponding coefficient.

On the other hand, the current legislation does not establish the procedure for applying the regional coefficient to bonuses. Therefore, the rules for bonuses can provide for their accrual using this coefficient in all situations for calculating incentive payments included in wages. The justification here is that the bonus is included in the salary.

The procedure for calculating northern bonuses is regulated by an instruction approved by Order of the Ministry of Labor of the RSFSR dated November 22, 1990 No. 2. It contains a ban on calculating bonuses for the following bonus payments (clause 19 of the instructions):

- one-time remuneration for length of service;

- remuneration based on the results of work for the year;

- incentives of a one-time nature and not provided for by the remuneration system.

At the same time, the instructions imply the possibility of calculating bonuses based on the results of work for a quarter, season or year, but with the condition that in order to calculate the monthly amount of the bonus, bonuses will be distributed over the months of the corresponding period in proportion to the time worked.

By the decision of the Supreme Court of the Russian Federation dated December 1, 2015 No. AKPI15-1253, the provisions of clause 19 of the instructions prohibiting the accrual of bonuses on remunerations paid for length of service and based on the results of work for the year were declared invalid as contrary to the current Labor Code of the Russian Federation. Thus, the northern bonus should be calculated on all bonus payments provided for in the remuneration system.

Assessment of accounting activities

Employee performance can vary significantly.

If it is easy to evaluate the results of the activities of a sales manager or a builder, then with an accountant the situation is much more complicated. It is not entirely clear how exactly to carry out the procedure. Indicators and criteria for bonuses were identified specifically to evaluate the activities of the accounting department. However, the standard is conditional. It is not enshrined in official documents. You can choose a suitable scheme for yourself. The fact is that accounting in different organizations varies significantly. A person working in a small company will not do the same things as an employee of a large organization. Therefore, it is necessary to select criteria for assessing the activities of accounting employees taking into account personal characteristics. The company Accountant of the Russian Federation is ready to select bonus criteria specifically for the client. Additionally, standards can be developed in accordance with which performance will be assessed.

The procedure for paying bonuses to employees according to current salary rules

After the changes made to the Labor Code of the Russian Federation, from October 3, 2016, the terms of payment of not only vacation pay (Article 136 of the Labor Code of the Russian Federation) and payment upon dismissal (Article 140 of the Labor Code of the Russian Federation), but also wages were legally limited.

The calculation of wages for the past month must now be carried out within 15 calendar days following this month (Article 136 of the Labor Code of the Russian Federation). Accordingly, taking into account the preservation of the wording in the Labor Code of the Russian Federation requiring payment of wages every half month, the timing of advance payments has also become more specific. Now it must be issued in the second half of the month for which it was accrued, maintaining a 2-week interval between the advance and salary.

However, questions remain regarding the payment of bonuses. Although the bonus provided by the wage system is a salary, it is not always calculated at the same frequency as wages. Therefore, the Ministry of Labor of Russia (information dated September 21, 2016, posted on the ministry’s website) recommended that the regulatory act on bonuses reflect an indication of both the month of bonus accrual and the month (or specific date) of bonus payment.

Specifying a payment month means that the premium must be paid no later than the 15th day of the corresponding month. If only the month of accrual is indicated, then the deadline for payment of bonuses will be the 15th day of the month following the month of their accrual (letter of the Ministry of Labor of Russia dated August 23, 2016 No. 14-1/B-800).

For more information about the procedure for paying bonuses under the Labor Code of the Russian Federation, read this article.

Criteria for assessing the performance of accounting employees

In order for the performance assessment of the accounting department to be fair, it is necessary to determine the criteria. It is necessary to take as a basis the processes in which the accountant takes part. The basis for bonuses may be:

- no claims from tax authorities;

- timely provision of reporting;

- minimizing the number of fines or their sizes;

- preparation of primary documentation without errors;

- timely issuance of invoices;

- fast and competent payroll calculation.

The list may seem strange at first. The fact is that an accountant is already obliged to provide reports and correctly determine the amount of taxes and wages. This means that specialists are provided with funds. In fact, it turns out that the business owner is obliged to reward employees if they do their job well and do not make mistakes. However, this is the essence of the work of accountants. Their activity is invisible as long as there are no errors. Therefore, the basis for bonuses is work without violations or complaints.

The transfer of accounting to outsourcing leads to the fact that the criteria that were previously the reason for accruing incentives are standard accounting services. There is no need to pay extra for the absence of errors and fines. The outsourcing company may lose money if it makes a mistake. The fact is that the outsourcer is responsible and pays monetary penalties from its budget.

If there is a need to transfer an organization to outsourcing, use the legal and accounting services of the company Accountant of the Russian Federation. We work in accordance with strictly established regulations. Our specialists comply with reporting deadlines and calculate taxes taking into account legal norms. The entire procedure is agreed upon with the client in advance.

If a company has a full-time employee, but does not want to overpay, it is worth using the standard scheme. To do this, they assign a small salary and a variable part that directly depends on the performance indicators. If a specialist performs the tasks assigned to him well, he will receive a large salary, if poorly, then a small one. An alternative is to provide a bonus during the reporting period. At this point, the load on the accountant increases significantly. The rest of the time, the specialist receives only a salary.

When preparing a list of criteria, it is necessary to exclude from them indicators that a specialist cannot influence. The employee's merits must be assessed according to clear indicators. You cannot install eroded foundations. Otherwise, the established criteria will not be a good incentive for a specialist to perform high-quality work.

There is no need to come up with a large number of indicators. For an employee who does not hold a management position, 5 criteria are sufficient. In practice, the entire department can be awarded a bonus. In this case, it is not necessary to divide the amount into equal parts according to the number of employees. The manager can take into account the participation rate gained in this way. It will demonstrate what contribution each specialist made to the common cause. Based on the data, you can determine the employee’s share of the bonus. The standard list of criteria can be supplemented:

- working outside the standard schedule;

- participation in training newcomers;

- work to correct errors made by representatives of other departments and perform other functions.

The list is not exhaustive. You can supplement it with other indicators. To create the most comprehensive list possible, you should turn to professionals.

Results

The bonus calculation procedure is determined by many factors. First of all, these are bonus rules developed by the employer independently. Among these rules, the description of the features of the applied remuneration and the establishment of algorithms for calculating the base for calculating the amount of bonuses of each type are of primary importance. When calculating bonuses, regional coefficients established in the region and northern bonuses, if the employee is entitled to them, must be taken into account.

Sources: Labor Code of the Russian Federation

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Payments to civil servants

In accordance with Art. 50 of Federal Law No. 79-FZ of July 27, 2004, in addition to the monthly salary paid, a civil servant receives additional payments:

- bonus for length of service, which, depending on the length of service, reaches 30% of the salary;

- allowance for work under special conditions;

- bonus for working with state secrets;

- bonus for completing particularly important or particularly difficult tasks;

- monthly cash incentive;

- annual one-time financial assistance, which is paid for the next vacation.

Why are the provisions being developed?

Nothing encourages employees to perform their duties efficiently and quickly as a variety of allowances and bonuses for special merits in the workplace. In order for these bonuses to be paid fairly and as efficiently as possible for the enterprise, it is necessary to develop a clear motivation system.

As provided in Art. 129 and 135 of the Labor Code of the Russian Federation, wages at an enterprise are formed from several components:

- salary, which takes into account the worker’s qualifications and type of activity;

- compensatory additional payments for special working conditions;

- incentives, allowances, bonuses, additional payments, etc.;

- social benefits for loss of income.

Employers are required to stipulate material rewards for effective work in collective agreements or local regulations of the organization (Part 2 of Article 135 of the Labor Code of the Russian Federation). One way to fix the conditions for assigning incentive payments in the wage regulations is to indicate them in a separate section. Another option is to specify the specifics of remuneration in a separate provision.

It is noteworthy that the right cash reward system is the best way to increase productivity, prevent employee turnover and attract qualified employees. In order for this system to benefit the enterprise, a provision should be developed to determine incentive payments, taking into account the so-called criteria for effective work. It is important not just to note what bonuses are provided in the company, but to clearly calculate and indicate the indicators - to whom, for what and how much it is expected to be paid for the successful solution of production problems.

Usually they pay extra for:

- number of hours;

- workload;

- seniority;

- labor productivity;

- quality work done;

- based on the results of work for the period (for the year, quarter, etc.).

But there are no uniform criteria. The employer independently determines the list of payments and their size, supplementing them with his own indicators, taking into account the specifics of the activity. For example, for the sales department such a criterion is the fulfillment of the sales plan, the number of concluded contracts, etc., in industrial production - exceeding the norm, the quality of manufactured products, in the service sector - the number of satisfied customers, etc.

IMPORTANT!

Incentives and compensation payments should not be confused. The former increase the interest of workers in effective work, the latter are appointed for harmful working conditions.

Most often, performance indicators are prescribed in the regulations on the calculation of incentive payments in a budgetary institution for the following categories:

- teachers of schools, technical schools and universities;

- kindergarten teachers;

- civil servants;

- social and cultural workers;

- workers of health resort treatment institutions.

For additional payments to salaries in government agencies, a separate budget is allocated at the federal and regional levels. For example, teachers are rewarded for introducing new courses and individual educational programs, conducting excursions and open lessons, organizing competitions, olympiads and other events.

Types of compensation and incentive payments

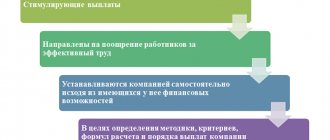

A separate type of monetary incentives are bonuses and additional payments. These payments, unlike one-time bonuses, are included in the remuneration system (Part 2 of Article 135 of the Labor Code of the Russian Federation). There are two types of allowances and surcharges:

- Stimulating.

They are similar in purpose to bonuses and are established to stimulate the employee to improve their professional level and acquire new knowledge. Bonuses and additional payments of an incentive nature include payments for class rank, title, academic degree, high rank, etc.

- Compensatory.

Paid to compensate the employee for costs and expenses associated with the performance of his job duties. Additional payments and allowances of a compensatory nature include payments for combining different professions, working at night or beyond the established work schedule.

Allowances and additional payments are mandatory and set at the discretion of the employer.

How in general the bonus is calculated as a percentage according to Decree No. 27

A bonus is an additional monetary reward received by employees for the results of their work (Bonus (economics) - Wikipedia).

From July 1, 2022, the following funds are allocated for the payment of bonuses to employees of budgetary organizations, provided for in the relevant budgets (clause 3 of Decree No. 27):

Note! 20% of the amount of salaries of such workers and unused extra-budgetary funds provided for wages are also allocated for bonuses to employees whose wages are paid from extra-budgetary funds (clause 2 of the Instruction on the procedure and conditions of wages, approved by Resolution of the Ministry of Labor and Social Protection No. 13).

In addition, it is allowed to use extra-budgetary funds for additional bonuses to employees in terms of the amount of excess income over expenses remaining at the disposal of the budgetary organization (paragraph 6, paragraph 25 of Regulation No. 641).

The size, procedure and conditions for paying bonuses are determined by budgetary organizations independently, taking into account industry specifics and are enshrined in the relevant provisions approved by the heads of budgetary organizations (clause 3 of Decree No. 27 dated January 18, 2019).

Note! The specific amounts of employee bonuses are determined on the basis of the Regulations in accordance with their personal contribution to the overall performance results. In general, the size of the bonus for a specific employee is not limited to the maximum amount.

As a rule, bonuses to employees are set as a percentage of salary and are calculated for the actual time worked. The size of the bonus as a percentage for a specific employee is determined by the Regulations, according to the bonus indicators approved therein and can be summed up.

Note! With the introduction of a new system of remuneration for employees of budgetary organizations, such a term as “list of payments for which bonuses are calculated” is not used in the legislation. In this regard, we recommend that in the bonus regulations being developed, the bonus payment indicators include an increase in the size of the bonus as a percentage for employees who are: - combining the position of employees (professions of workers); - expanding service areas (increasing the volume of work); release from work.

Example 1. Calculation of wages and bonuses as a percentage for a teacher at a college located in a rural area

The teacher has the highest qualification category, 17 years of work experience in budgetary organizations, and an annual teaching load per salary. The teacher is given a bonus for work experience in budgetary organizations - 30% of the salary, a bonus for work under a contract - 30% of the salary, a bonus for the specifics of work in the field of education in the amount of 65% of the salary, a bonus for high achievements in work in the amount of 15% of the salary , allowance for work in rural areas - 20% BS.

In accordance with the qualifications of the teacher, the 11th tariff category is established (subclause 1.4, clause 1 of the table of Appendix 2 to the resolution of 06/03/2019 N 71).

The bonus amount as a percentage for the current month worked according to the Regulations was 20% of the salary. The calculation of bonuses and wages for a full month worked will be as follows:

| Indicator name | Amount, rub. |

| Teacher's salary (195 x 1.91) | 372,45 |

| Bonus for work experience in budgetary organizations - 30% of the BS (195 x 30 / 100) | 58,50 |

| Supplement for contract work - 30% of salary (372.45 x 30 / 100) | 111,74 |

| Allowance for the specifics of work in the field of education in the amount of 65% of the salary (372.45 x 65 / 100) | 242,09 |

| Bonus for high achievements in work in the amount of 15% of the salary (372.45 x 15 / 100) | 55,87 |

| Allowance for work in rural areas - 20% of the BS (195 x 20 / 100) | 39,00 |

| The 20% bonus amount will be (372.45 x 20 / 100) | 74,49 |

| The amount of calculated wages will be (372.45 + 58.50 + 111.74 + 242.09 + 55.87 + 39.00 + 74.49) | 954,14 |

Example 2. Calculation of wages and bonuses as a percentage for an office cleaner who has an additional payment for an expanded service area

The cleaner of office premises (except for bathrooms) at the college has 11 years of work experience in budgetary organizations. This employee is given a bonus for work under a contract - 20% of the salary, a bonus for work experience in budgetary organizations - 20% BS and an additional payment for an expanded service area in the amount of 30% of the salary for the full month worked (part 1, clause 14 of the Instructions on incentives). and compensatory payments No. 13).

A cleaner of office premises (except for bathrooms) corresponds to the 1st category of work and a multiple of the base rate - 1.0.

According to the Regulations, taking into account the increased volume of work in the current month worked, the bonus to the employee is set at 25% of the salary. The calculation of wages and bonuses for a full month worked will be as follows:

| Indicator name | Amount, rub. |

| Salary for office cleaner (195 x 1.0) | 195,00 |

| Bonus for work experience in budgetary organizations - 20% of the BS (195 x 20 / 100) | 39,00 |

| Supplement for contract work - 20% of salary (195 x 20 / 100) | 39,00 |

| Basic additional payment up to minimum wage - (400 - (195 + 39 + 39)) | 127,00 |

| Additional payment for extended service area - 30% of salary (195 x 30 / 100) | 58,50 |

| Prize amount - 25% (195 x 25 / 100) | 48,75 |

| The amount of calculated wages will be (195.00 + 39.00 + 39.00 + 127 + 58.50 + 48.75) | 507,25 |

Read this material in ilex >>*

* following the link you will be taken to the paid content of the ilex service

About incentive payments to employees

This material is an excerpt from a literary transcript of the seminar “Payment: law, accounting, taxes” (lecturer: E.V. Vorobyova), which was conducted by the Glavnaya Kniga publishing house.

In ancient Rome, a stick was called a stimulus, with which they drove cattle, and sometimes beat slaves, forcing them to work. Nowadays, no one beats workers anymore, but they use the “carrot method”, based on the fact that a person will work more and better if incentive payments are established for him.

What are the incentive payments? There are a huge number of them. For example, you can establish an additional payment to an employee for leading a team or for working with information that constitutes a trade secret. By doing this, the employer seems to be telling the employee: “I understand that you have greater responsibility and the work is becoming more complicated, so I will pay you more.” Although, of course, the most famous and widely practiced incentive payments are bonuses.

Unfortunately, some employers and accountants still believe that any bonuses can be considered incentives, as long as they are enshrined in an employment or collective agreement or local regulation. There are awards for birthdays, for City Day, and for the anniversary of the organization. There are awards for active social work and for conscientious work. And the employer sincerely believes that all these bonuses are earned by the employee and they can and even should be included in tax expenses.

After all, he read in the Tax Code of the Russian Federation that labor costs include any accruals to employees provided for by law, labor and collective agreements. But in fact, he loses sight of the fact that labor costs include not any payments specified in the employment contract, but payments specifically and only for work performed within the framework of the employment contract. After all, the wage system is payments specifically for work.

Therefore, I always tell my listeners: when reading the norms of legislation, you should not skip words, even if they seemed unprincipled to you. Otherwise you may make a mistake. So, bonuses are divided into stimulating and incentive. What is the difference between them? Before the amendments to the Labor Code that came into force on October 6, 2006, it was easier to answer this question. Because, according to Article 129 of the Labor Code of the Russian Federation, only incentive payments were included in wages. And incentive bonuses were mentioned only in Article 191 of the Labor Code, in Chapter 30 of the Labor Code of the Russian Federation “Labor Discipline”.

And then it was clear that with such bonuses the employer rewards the most disciplined employees for compliance with the requirements of internal labor regulations. That is, such bonuses did not directly pay the employee’s work.

After the amendments were made, this line became blurred, because in the current version of Article 129 of the Labor Code of the Russian Federation, other incentive payments are classified as incentive payments, among others. Let's try to figure out in which cases bonuses will be stimulating and in which they will be incentive.

Wages are remuneration for work. This means that any payment that is part of the salary, in turn, must also be a reward for labor. The very word “reward” (by the way, has the same root as the word “reward”) suggests that in order to receive it, a certain action must be performed. You cannot reward someone who has done nothing. Therefore, an incentive bonus must be assigned for some kind of labor indicator. And each employer chooses the specific types of labor indicators for which employees are rewarded depending on the industry and the specifics of its activities. For example, a miner can be rewarded for exceeding coal production standards, a seller can be rewarded for the quality of customer service and increased sales.

This means that in order to recognize an incentive payment as an expense for profit tax purposes, it must: - be specified in the employment contract with the employee; - was made for labor.

But then what about the bonuses paid in many organizations on March 8, a professional holiday or on the occasion of an employee’s birthday? These bonuses are paid to the employee by the holiday, regardless of the quality of his work, that is, these are bonuses not for labor achievements. This means that such bonuses cannot be stimulating. These are social payments that are not recognized as tax expenses. And both the Ministry of Finance and tax authorities have written about this repeatedly.

However, there is also another problem - how to qualify bonuses for performing urgent or particularly important work outside the employee’s official duties? In one very interesting, in my opinion, Letter from the Federal Service for Labor and Employment it is said that such bonuses are not included in the remuneration system. This baffles many accountants. After all, payments for work should certainly be wages. And the Letter says that these bonuses are made outside the remuneration system. Why?

To answer this question, we must turn to the definition of an employment contract in the Labor Code of the Russian Federation. An employment contract is an agreement between an employer and an employee. The mandatory conditions of an employment contract include, in particular: - the employee’s labor function, that is, a list of the duties that he must perform; - the amount of payment for performing these duties.

If we assume that the urgent work was performed within the framework of the employee’s duties established by the employment contract, then there will simply be no basis for paying him a bonus - the employee completed ordinary work (even faster than he could), for which he will be paid a regular salary.

Thus, the only basis for an additional bonus payment will be that the employee has performed additional work beyond what is usually performed. But if urgent work was performed outside of official duties, it means that it was not provided for in the employment contract. Therefore, it is outside the wage system. And it cannot be taken into account in tax expenses. After all, any employee benefits other than those specified in the employment contract are not recognized as expenses.

For example, an accountant is asked to register real estate rights. Agree, this is not the responsibility of an accountant.

By the way, the Labor Code prohibits requiring an employee to perform work not stipulated by the employment contract, except for cases specified in law. Such, for example, as situations that are related to ensuring the country’s defense capability, eliminating accidents, natural disasters, catastrophes, and the like.

So, engaging an employee in such additional urgent work is also a violation of labor laws. There is only one way out. If an employer wants to entrust an employee with some urgent or particularly important work that is not part of his job functions, then it is necessary to conclude a separate agreement to the employment contract. It must indicate what the employee must do in addition to his normal duties and what he will receive for this in addition to his regular salary. Then this will be a payment that is included in the wage system and reduces the income tax base.

Obviously, in an additional agreement to an employment contract it is possible to establish not only the type of work entrusted to the employee and the procedure for remuneration for its implementation, but also the validity period of this agreement and any other conditions.

By the way, please note that until 2010 there was such a dependence - payments that were not recognized as expenses that reduce the tax base for income tax were not subject to the Unified Social Tax. Therefore, many employers specifically tried to formulate the basis for paying bonuses in such a way that the bonus was perceived as a payment of a non-productive nature. Thus, they avoided taxation of this UST payment. Since 2010, the situation has changed “exactly the opposite.” The legislator provided in Law N 212-FZ that any bonus, including those not related to production, for example, for March 8, is now subject to contributions. After all, there is no norm similar to paragraph 3 of Article 236 of the Tax Code of the Russian Federation in Law No. 212-FZ.

And only bonuses included in the wage system can still be recognized as expenses in tax accounting. That is, payments for labor directly related to the completion of a specific amount of work. By the way, a typical mistake when assigning bonuses is that when indicating in the order the reason for paying the bonus, two mutually exclusive reasons are written. For example, a prize “on the occasion of the 50th anniversary for many years of conscientious work.” And questions immediately arise. If the employee did not have a birthday, would the employer not pay him a bonus for his work? And if he would have been paid a bonus for many years of conscientious work in any case, why write in the order that it is his birthday?

These are completely different reasons for paying a bonus. Therefore, when deciding to pay a bonus for production performance, you need to indicate such a basis for the bonus so that the bonus is clearly interpreted as payment for work. Otherwise, problems may arise with recognizing this payment as an expense. After all, by indicating that the bonus is paid on the birthday, the employer himself allows the tax authorities to exclude the payment from tax expenses.

Question. Our bonus regulations stipulate that an employee who has worked for the organization for 5 years is given a gift certificate for 3,000 rubles. Will it be an incentive bonus or an incentive in the form of a gift?

Again, it all depends on the wording used in the bonus clause. I think that it is quite possible to consider such a gift certificate as an incentive payment in kind. The employer seems to tell the employee in advance: “If you work for me without a break for 5 years, you will receive a bonus for your length of service.” But for this, the bonus regulations must state that this is an incentive payment, the purpose of which is to interest the employee in working for as long as possible in your organization. And indicate that the employer has the right to give this bonus both in cash and in another form, including in kind. Let me remind you that in this case the requirements of Article 131 of the Labor Code of the Russian Federation must be met.

In this case, the gift certificate can be recognized in tax accounting as part of labor costs as an incentive bonus. And if the condition for issuing a certificate is not specified in the bonus regulations, but is simply given as a gift to an employee who has worked in your organization for 5 years, then this will already be a social benefit. And such a payment does not reduce the income tax base.

Therefore, it is important for the employer to decide in advance what type of payment the bonus will apply to. And when drawing up local regulations and bonus orders, use language that allows you to unambiguously qualify bonus payments. When considering bonuses, I would like to raise another controversial issue - is it necessary to issue an order for bonuses in Form N T-11 “Order (instruction) to reward an employee”?

I believe that it is not necessary, since the form of the order does not change either the essence of the payment or the procedure for its reflection in tax accounting. Firstly, if this is a bonus for labor provided for in an employment contract, related to the performance of job duties, then no matter how it is formalized - by order in Form N T-11 or in any form, it still remains part of the salary. Secondly, let's take a close look at Form N T-11. It is called “Order (instruction) to encourage an employee,” and not about incentives at all. In this form there is a line where you need to indicate the type of incentive, and several possible types of incentives are listed to choose from: gratitude, valuable gift, bonus.

That is, these are the same incentives that are listed in Article 191 of the Labor Code. This means that we mean incentives for those employees who come to work on time, do not violate labor regulations, and the like. And this, in general, has nothing to do with wages. There is also indirect confirmation of this point of view - in the Rules for maintaining work books. According to these Rules, information about the types of incentives provided for by labor legislation is entered into the work book. And this, as we have already discussed, includes incentive bonuses for conscientious performance of labor duties. While the incentive bonuses provided for by the wage system are not reflected in work books.

So, in my opinion, in order to pay an incentive bonus, it is quite enough to issue a bonus order in any form, which will indicate who is being bonused, for what and in what amount. By the way, there is another question that is of great concern to large organizations: is it necessary to ask each employee to sign the bonus order? What to do if there are several thousand employees and monthly bonuses?

In my opinion, the signatures of each employee on the order for the accrual of bonuses that are of a regular nature (monthly, quarterly, etc.) are not required. Let's think about what goal the employer pursues when introducing employees to the bonus order? Bring to the attention of each employee both the fact that a bonus will be awarded and its amount. At the same time, if an employee does not agree with the amount of the bonus, he can seek appropriate clarification both from the employer and from another body whose tasks include resolving labor disputes. But this goal will be fully achieved in another way - by issuing the employee a pay slip, which indicates all accruals, deductions and other information.

In addition, I would like to remind you that neither the Russian Ministry of Finance nor Rosstat currently have the authority to develop and approve forms of primary accounting documents and do not have the authority to provide explanations on their use. And initially, Resolution of the State Statistics Committee of Russia dated January 5, 2004 N 1, according to the conclusion of the Ministry of Justice of Russia, did not require state registration (Letter of the Ministry of Justice of Russia dated March 15, 2004 N 07/2732-UD).

This means that it does not, in principle, contain regulatory requirements that are binding on all organizations. Of course, many employers may object that tax and other regulatory authorities require the submission of certain unified forms during their audits. But this requirement is not conditioned by anything and can be challenged, in particular, in court. The Law “On Accounting”, Article 9 of which is usually referred to to justify the requirement for the availability of unified forms of primary documents, regulates exclusively accounting issues, but not personnel records or even taxation.

The only exceptions are those documents that are necessary to reflect a particular transaction in accounting. We will talk about some of them later, when we touch on the issue of recognizing travel expenses for tax purposes.

First published in the publication “General Book. Conference Hall” 2010, No. 08

Hello Guest! Offer from "Clerk"

Online professional retraining “Chief accountant on the simplified tax system” with a diploma for 250 academic hours . Learn everything new to avoid mistakes. Online training for 2 months, the stream starts on March 1.

Sign up