Employers must withhold personal income tax (PIT) from their employees' paychecks. Therefore, if an employee has a salary of 30,000 rubles, he will receive only 26,100 rubles in cash minus personal income tax of 13%, if without any difficulties.

In order for some groups of employees to receive more, tax deductions were invented. The deduction works like this: they take the employee’s income, reduce it by the amount of the deduction, and calculate the tax from this amount. That is, they reduce the tax base, and not the tax itself.

Example

Florist Katya has a salary of 30,000 ₽ and a deduction of 1,400 ₽ for her daughter, which means they will deduct from her salary:

- in January: (30,000 - 1,400) × 0.13 = 3,718 ₽

- in February: (60,000 - 2,800) × 0.13 - 3,718 = 3,718 ₽ and so on.

Deductions for personal income tax are different: standard, property, social and professional. Most often, employees come with standard tax deductions: for themselves or for a child.

!

Remember, personal income tax is always considered a cumulative total from the beginning of the year, as in the example

Standard tax deductions reduce income, which is subject to personal income tax at a rate of 13%. Standard deductions are not applied to income at other rates and dividends. Non-residents cannot use deductions either. Let us remind you that a non-resident is an individual who stays on the territory of the Russian Federation for less than 183 days within one year.

Child deduction

Parents are entitled to a deduction for each child under 18 years of age. If the child is a graduate student, resident, intern, student or cadet and is studying full-time, then the age limit is increased to 24 years.

The following may receive a deduction:

- each of the parents - no matter whether they are married, divorced or never married;

- husband or wife of a parent;

- each of the adoptive parents, guardians, trustees, when there are several of them;

- each of the adoptive parents, if there are two of them.

If the only parent or the second parent refused the deduction, you can count on a double deduction. Moreover, only a working parent can refuse the deduction: if the parent does not work, then he does not have the right to the deduction, which means there is nothing to refuse.

Amounts of deductions for children

The deduction amounts are currently as follows:

— for the first and second child — 1,400 ₽

— for the third and each subsequent — 3,000 ₽

Children are counted regardless of age. For example, an employee has three children. Two are already adults: 25 years old and 23 years old, and the third is 16 years old. An employee is entitled to one deduction for a third child - 3,000 rubles.

There are more deductions for disabled children:

— for parents and adoptive parents — 12,000 ₽

— for guardians, trustees, foster parents — 6,000 ₽

It does not matter what type of disabled child is in the family. You can also add general deductions for children. For example, for an only disabled child, the deduction will be 13,400 rubles. After all, parents are entitled to a deduction for their first child - 1,400 rubles and for a disabled child - 12,000 rubles.

!

Provide a standard tax deduction for a child until the month in which the employee’s income from the beginning of the year exceeds 350,000 rubles.

Interesting fact

If a child grows up quickly and gets married, then you can no longer get a deduction for him - now he provides for himself. But if he decides to try his hand at work, then his parents still have the right to a deduction. In general, marriage is a responsible matter :)

If the deduction is greater than income

It may turn out that the personal income tax deduction is greater than the accrued salary. The reasons may be different.

From our VKontakte group we learned that in practice accountants face the following problem.

Here's what one of our subscribers wrote:

Good day everyone! Help with advice. A friend appeared in the organization, whose tax agent for personal income tax we are, and it turns out that the deduction for income exceeds the income itself. That is, for example, in January he had income, he deducted deductions for children and professional deductions, paid personal income tax from the tax base, and in February and March he had income of three kopecks, and no one canceled the deductions. And now it turns out that for the quarter I withheld personal income tax (January) more than I should have. What to do in such situations, submit the 6-personal income tax with an overpayment and then, on a cumulative basis, equalize everything or submit the report as it should be (without overpayment)?

My colleague is right: a deduction must be provided even if there is not enough income. The Ministry of Finance wrote about this in a letter dated March 2, 2022 No. 03-04-06/15364.

The main conclusion is this: if the amount of deductions is greater than taxable income, then the personal income tax base is equal to 0 (clause 3 of Article 210 of the Tax Code). That is, the tax will also be equal to 0. And in accounting, the amount of excess deductions over income can be transferred from one month to another. But only for a year.

This means that excessively withheld personal income tax that appears during the year due to the excess of deductions over current income can be repaid by tax on the following income before the end of the year.

It can also be returned to the employee upon his application, and if the tax cannot be either credited or returned, at the end of the year the employee can himself apply to the tax office for its return (Article 231 of the Tax Code of the Russian Federation). Excess tax deductions are not carried over to the next calendar year (except for property).

How to fill out 6-NDFL?

Documents for child support

First, the employee needs to write a free-form deduction application and attach supporting documents to it: a birth certificate or a certificate from an educational institution.

Deduction application template

If an employee has not been working since the beginning of the year or works part-time in another organization, ask him for a certificate in form 2-NDFL from other places of work. She will confirm that income since the beginning of the year has not exceeded 350,000 rubles.

!

Do not provide an employee with standard tax deductions that he did not receive from his previous employer or did not receive in full.

In some cases, other documents will be needed. For example, from a spouse who is not the child's parent or guardian, ask for a statement from the child's mother or father stating that the spouse is providing for the child.

Some documents need to be updated every year. The general rule: if a document confirms the right to deduction only in one period, then it needs to be updated in the next. For example, request a certificate from the university every year, because the situation may change next year.

Useful video

Learn more about the standard child deduction in the video below:

We can conclude that if the salary is less than the deduction for children, the accounting department at the place of work must calculate the amount of income and benefits for all months of the year before the current one. And based on the results, return the difference in personal income tax “in hand” or together with the salary, or recognize the tax base as zero. Transferring the deduction for children with a low income is possible to other months only within the calendar year. Only property benefits are allowed to be carried over to the next year.

Child benefit period

Provide a deduction from the month in which the employee confirms that he has a child. If the employee submitted an application in the current year, then provide deductions from the beginning of the year. Even if he declared his right to a deduction in the middle or end of the year.

Example

Alice has been working in the organization since the beginning of the year, but she only remembered that she had the right to a deduction in May, and then she submitted an application. Alisa is a mother and has two minor sons. This means that from January to May, deductions amounted to 14,000 rubles (1,400 × 2 × 5).

Alice has a salary of 40,000 ₽, in total, from January to April, Alice was credited 160,000 ₽ (40,000 × 4) and withheld personal income tax - 20,800 ₽.

In May, the accountant will calculate all unaccounted deductions and only personal income tax will be withheld from the salary in the amount of 3,380 ₽ ((200,000 - 14,000) × 0.13 - 20,800), instead of 5,200 ₽ (200,000 × 0.13 - 20,800). This means that Alice will receive 36,620 ₽ (40,000 - 3,380), instead of 34,800 ₽ (40,000 - 5,200).

But if an employee had the right to a deduction last year and forgot to declare it, then he can only receive this deduction on his own through the tax office.

Forgot to apply a personal income tax deduction - how to fix it in 1C: ZUP ed. 3.1?

Published 07/13/2020 13:27 Author: Administrator In the work of an accountant, a situation may often arise when it is necessary to make changes to the right to deductions of employees for calculating personal income tax. Usually, this happens when the salary has already been accrued (and not for one month), and the accountant forgot to reflect the provided certificate of deductions or the employee did not provide it on time. And even more questions arise when the amount of “missed” deductions becomes more than the personal income tax accrued for the current month. What to do in such situations so that the 1C program: ZUP ed. 3.1 correctly calculated personal income tax and correctly reflected the data in reports 6-NDFL and 2-NDFL? We will consider both cases in detail in the article.

Situation No. 1: the deduction provided is less than the calculated personal income tax

First, let's see in which document the deductions are clearly reflected?

When calculating wages, in the document “Accrual of wages and contributions” on the “Personal Income Tax” tab, in addition to the amounts of calculated tax, there is information about the deductions provided - the “Applied deductions” column.

By clicking on the line with the employee of interest, detailed information about the calculated personal income tax, income and applied deductions from the beginning of the year will open.

If deductions are not reflected or reflected incorrectly, they must be entered or the data corrected. When providing documents on the right to deduction, the data is entered into the employee’s card: “Personnel” - “Employees”, in the “Income Tax” section information about deductions is reflected.

Employee Grushevsky S.N. a deduction for two children is taken into account.

In this section you can:

• correct data on deductions; • enter a new statement of deductions; • terminate the right to deduction.

From employee Alferova S.A. The accountant did not take into account the provided certificate of the right to deduction and from the beginning of the year no deductions were provided to her.

Let's fix this situation.

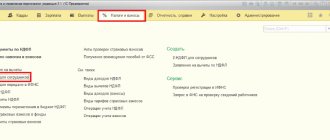

Step 1. Open the “Employees” directory in the “Personnel” section. Let’s select an employee and follow the “Income Tax” hyperlink.

Step 2 . Follow the hyperlink “Enter a new claim for standard deductions.”

Step 3 . Let's fill in the information about the deduction provided.

We indicate:

• date of application; • from what month is it available; • deduction code; • for which month the deduction is provided; • a document confirming the right to apply the deduction.

One little hint: in the “Provided up to (inclusive)” field, the program defaults to December of the current tax period. In this case, at the beginning of the next one, you will need to enter information about the deduction into the program again. But we understand how much work an accountant has at the end and beginning of the year; there is a high probability that you won’t even remember about the deduction during the reporting period. Accordingly, the salary will be calculated without deducting personal income tax, which will subsequently lead to a recalculation of the tax. Therefore, we recommend that you immediately enter the month and year in which the child turns 18 in this field. In this case, you will not have to return to this issue again if no changes occur.

Step 4. Save the document – “Post and close”.

Deduction from employee Alferova S.A. fixed. To make corrections to an existing application, follow the hyperlink “Correct an application for standard deductions.”

Let's move on to calculating wages and calculating personal income tax for the current month. Let's consider how our data change will be reflected.

When accruing the salary of the current month, in order not to affect other employees, right-click on the desired line and select “Recalculate employee” in the context menu.

As a result of the recalculation, the program will take into account the entered data on the deductions provided and recalculate the personal income tax.

Let’s open the personal income tax decoding by double-clicking on the employee’s last name.

The line for the current month shows the amount of deductions provided since the beginning of the year. By clicking the mouse, a window will open with details of the months for which they were provided.

As a result of entering the certificate retroactively, all deductions for the current year are taken into account.

Let's check how the provided deductions are reflected in the reports.

To check, we will generate the following reports:

1. Certificate 2-NDFL; 2. Report 6-NDFL.

Go to the section “Reporting, certificates” - “2-NDFL for employees”.

Step 1. Click “Create”.

Step 2 . We select an employee. The information in the certificate will be filled in automatically.

The certificate reflects the employee’s income, the amount of tax calculated and withheld, as well as the deductions provided.

Step 3 . We will generate a printed form of the certificate – “Certificate of Income (2-NDFL)”.

The printed form shows that the amount of deductions is provided for the entire period specified by us.

Let’s generate a 6-NDFL report and see how the employee’s data is reflected in it.

Step 1 . Go to the section “Reporting, references” - “1C-Reporting”.

Step 2 . Click “Create” and in the “Reporting for individuals” category select “6-NDFL”.

Step 3 . Using the period selection buttons, set the reporting period. In our example, July is included in the 9 month period. Click “Create”.

Step 4 . Let's generate a report - the "Fill" button.

The first section of the report reflects the amounts of income, calculated tax and applied deductions for the organization as a whole.

Once you select a cell in a report, you can decipher it in different ways:

1. Clicking the “Decrypt” button; 2. Right-click on the cell and select the “Decrypt” command; 3. Selecting “Decrypt” in the submenu using the “More” button;

In the detail of the report cell “Amount of tax deductions” you can see the provided deductions for all employees. From employee Alferova S.A. deductions in full are taken into account in the 6-NDFL report.

Situation No. 2: the deduction provided is greater than the calculated personal income tax

Let's consider a frequent case when, as a result of applying the accumulated deduction, its amount is greater than the tax calculated for the current month. After all, nothing scares an accountant more than a red minus in a document or report.

Suppose employee S.A. Alferova a deduction was provided for a disabled child (code 129/117) in the amount of 12,000 rubles. monthly. This code is reflected in the employee’s card in the application for deductions.

Let's recalculate the employee's accruals and analyze the situation.

It is clear from the accrual that Alferova S.A. a deduction was provided for the current month in the amount of 84,000 rubles, based on 12,000 rubles. for the period from January to July. As a result, the personal income tax amount was reflected as a refund with a minus. This can be seen in detail in the transcript of the line. Let’s open the details by double-clicking the mouse in the accrual document on the employee’s line and in the window that appears, click on the “Deductions” cell.

On the “Accruals” tab, we will create a payslip for the employee.

The payslip reflects the amount of personal income tax recalculation and the amount of excessively withheld personal income tax.

Let's see how this correction will be reflected in the 2-NDFL certificate.

Let's return to our certificate in the section “Reporting, certificates” - “2-NDFL for employees”. Click “Fill” to update the data.

The certificate reflects the amount of the deduction provided and the amount of excess tax withheld.

We will generate a 6-NDFL report after correcting the data (“Reporting, certificates” - “1C-Reporting”).

Open the previously saved report and click “Fill”.

The information has changed. In the transcript of the cell “Amount of tax deductions” you can see the changed amount of deductions for employee S.A. Alferova.

Thus, we corrected the shortcomings in providing deductions to employees.

To correctly calculate tax when calculating wages, it is important to monitor the correct application of deductions and, if an error is detected, correct it in a timely manner. Since the application of deductions and the calculation of personal income tax occur on an accrual basis from the beginning of the year, such a correction is permissible.

Author of the article: Olga Kruglova

Did you like the article? Subscribe to the newsletter for new materials

Add a comment

Comments

0 Irina 02/08/2022 01:22 Hello, Olga. We discovered an unapplied deduction in November and the last two months of the year were not enough to offset the over-withheld tax. In January of the new year, the program did not take into account the remaining debt. Is there something wrong with the program? Can I correct it manually? Or does such debt not carry over to the next year?

Quote

0 Irina Plotnikova 01/28/2021 18:49 I quote Larisa:

Hello! Tell me, the employee brought benefits for children. They mistakenly provided benefits for two children from April 2022. But it turned out that one certificate was establishing paternity for the same child. Discovered in Q4 2020. Do you need to submit clarifications for 6-NDFL for six months and 9 months for section 1? Or can everything be done in December?

Larisa, hello.

In your case, the tax agent unlawfully provided a deduction to an individual. Accordingly, he transferred personal income tax to the budget in a smaller amount than necessary. A tax arrears arose in the form of the difference between the amount of personal income tax that was required to be withheld and the amount of personal income tax that was actually withheld. This debt should be withheld from the next payment to the employee (for example, from the next month’s salary). However, the salary will have to be recalculated in all months where the error was made. At the same time, it is necessary to remember the limitation: the total amount of deduction for the current month should not exceed 50 percent of the payment amount (clause 4 of Article 226 of the Tax Code of the Russian Federation). Along with the additional payment of the amount that was not withheld earlier, the tax agent is obliged to pay a penalty for late transfer of personal income tax (Article 75 of the Tax Code of the Russian Federation). Penalties are calculated from the moment when the employer was supposed to withhold and pay personal income tax to the budget until the actual date of fulfillment of this obligation (clause 2 of the resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation dated July 30, 2013 No. 57). In addition, you will have to submit corrective calculations in form 6-NDFL for the corresponding periods (six months and 9 months) Quote 0 Larisa 01/27/2021 16:43 Hello! Tell me, the employee brought benefits for children. They mistakenly provided benefits for two children from April 2022. But it turned out that one certificate was establishing paternity for the same child. Discovered in Q4 2020. Do you need to submit clarifications for 6-NDFL for six months and 9 months for section 1? Or can everything be done in December?

Quote

0 Larisa 01/27/2021 16:40 Hello! Regarding the recalculation of deductions from the beginning of the year according to 6-NDFL Do I need to submit clarifications for previous quarters?

Quote

0 Irina Plotnikova 08/14/2020 05:36 I quote Tatyana:

Good afternoon There was a situation like in example No. 2, also deductions for children from January to June were not provided, they corrected it in July, everything became beautiful, but when calculating for August, the deductions provided are reflected with a minus and the tax is considered more than it was, for example, for one child in In July I recalculated and provided deductions in the amount of 9800, and in August I submitted deductions minus 7300. What can you tell me?

Tatyana, good afternoon.

If the program reverses deductions in red, it means they were used in some document. Perhaps the deduction was used in August documents (vacation, bonus, sick leave, etc.), then a decision was made to apply the deduction in the July payroll. Thus, 2 documents were used where the deduction appears. The program sees this defect and reverses the deduction. I recommend distributing all documents for July and August to each employee and putting everything in chronological order. When distributing documents, use the payslip so as not to miss a single accrual and payment document. Quote 0 Tatyana 08/13/2020 19:37 Good afternoon! There was a situation like in example No. 2, also deductions for children from January to June were not provided, they corrected it in July, everything became beautiful, but when calculating for August, the deductions provided are reflected with a minus and the tax is considered more than it was, for example, for one child in In July I recalculated and provided deductions in the amount of 9800, and in August I submitted deductions minus 7300. What can you tell me?

Quote

0 Irina 07.27.2020 16:38 Super!!!

Quote

Update list of comments

JComments

Deduction for yourself

Some adults are entitled to a deduction of 500 ₽ or 3,000 ₽. The amount depends on which benefit category the employee belongs to. Among them are disabled people who suffered from the Chernobyl disaster, participants in military operations, heroes of Russia and many others. All categories can be viewed in paragraphs. 1 and 2 paragraphs 1 art. 218 Tax Code of the Russian Federation.

To receive a deduction, the employee brings an application and documents confirming his right to the deduction.

Such deductions cannot be added and used at the same time. If an employee is entitled to several standard deductions, provide one of them - the maximum. But there is no income limit - provide deductions for yourself regardless of the amount of income received.