When you need to send a return of goods from a buyer to a supplier, it is often difficult to figure out what documents to fill out so as not to make mistakes. You should know in which cases this is easy to do and in which it is not documented. And most importantly, remember the rules and nuances of the process and reimbursement of expenses. The Civil Code stipulates that the buying party may not accept and send back the cargo in several cases. This is possible if there is no corresponding clause in the contract. Let's look at what this looks like and what to do.

How to return when the product is of poor quality

There are two articles in the Civil Code that give the opportunity to the person or organization who bought it to send the purchase back to the owner - 518 and 475. Products that do not comply with the contract must have serious deficiencies in:

- types of models, colors;

- configurations;

- quality;

- external signs.

If the violations are small and easily corrected, then sending the order to the seller is allowed only to correct the problems. If part of the kit breaks, then this particular part will be replaced.

But if there are large and noticeable defects, as well as those that cannot be eliminated, the buyer returns the product. He can then choose one of two options:

- get money back;

- exchange for the same new and intact cargo.

This operation is available as long as the product is in good condition and is covered by the manufacturer's warranty. This is also possible within 2 years from the date of purchase if:

- the owner of the product will be able to provide evidence that the defect was identified before the end of the warranty period;

- There was no warranty period specified for the product.

It is important to remember that the articles do not apply to those items that were purchased for further resale. Therefore, if a delivery agreement has been concluded, then you should not count on sending the improper purchase back.

Returning goods to the supplier in 1C: Accounting

Published 01/18/2020 22:06 Author: Administrator Since 2022, the procedure for returning goods has been significantly simplified. According to the innovations, the buyer no longer formalizes this operation as a reverse sale and does not issue an invoice. All the buyer needs to do is issue an invoice or a return certificate from the island. In this way, the return of both defective and high-quality goods is processed, regardless of the date of purchase.

In accordance with the recommendations of the Federal Tax Service (letter dated October 23, 2018 No. SD-4-3 / [email protected] ), upon receipt of the returned goods, the seller issues an adjustment invoice, which the buyer should reflect in the sales book. That is, the restoration of VAT previously accepted for deduction on returned goods is carried out on the basis of an adjustment invoice received from the seller.

Let's look at a practical example in 1C: Enterprise Accounting, processing the return to the supplier of goods purchased and registered in 2022.

This operation will be reflected in the document “Return of goods to the supplier”.

In the “Receipt Document” line, you must select the document that reflected the receipt of goods to be returned.

Particular attention must be paid to the VAT rate. From 2022, the VAT rate is 20%. But if the goods were purchased before 2022, then the VAT rate in the document “Return of goods to the supplier” is indicated as 18%, that is, the VAT rate when returning goods will be the same as when purchasing.

In our example, the purchase of goods was made in 2022, which means that the VAT rate for returning goods will be 20%.

In the printed form of the consignment note (form TORG-12), the line “Base” requires special attention of the buyer. Here, in addition to o, you must manually enter the details of the supply agreement, delivery notes and other documents that are directly related to this business transaction.

Upon receipt of an adjustment invoice from the supplier, the buyer registers it in the same “Return of goods to supplier” document that was used to issue the return of goods and the return invoice.

Please note that the document generates transactions using account 76.02 “Calculations for claims”.

The return of goods to the supplier is reflected in the sales book with transaction type code 18.

In the VAT return, the refund to the supplier is reflected on line 080 of Section 3.

Author of the article: Marina Alenina

Did you like the article? Subscribe to the newsletter for new materials

Add a comment

Comments

0 #10 Anna Kulikova 02.02.2022 13:47 I quote Natalya:

Good afternoon. Tell me, if the product was purchased in 2020 and returned in 2022, how to correctly reflect it in 1C? I reflected the receipt by adjusting it and made additional postings (I mean that there is an inaccuracy in the reflection). The accounting reports were submitted for 2022, I think how correctly it could be corrected.

Natalya, good afternoon.

Your question is not entirely clear. Why was the intake adjusted? Were there any problems with the initial admission? Logically, if you bought a product in 2022, it lay in a warehouse for a year and then you returned it in 2022, then the algorithm of actions from this article is quite suitable for you. What’s in the reconciliation report with the supplier? Was a separate return operation recorded or did they also adjust the primary implementation document? Quote 0 Natalya 02/02/2022 04:25 Good afternoon. Tell me, if the product was purchased in 2022 and returned in 2022, how to correctly reflect it in 1C? I reflected the receipt by adjusting it and made additional postings (I mean that there is an inaccuracy in the reflection). The accounting reports were submitted for 2022, I think how correctly it could be corrected.

Quote

0 Irina 02/29/2020 00:29 I quote PAWS:

Hello! How is the return of goods reflected by the seller?

Hello.

There is an article on the site about this. Return of goods from the buyer in 1C: Accounting. Quote 0 Sergey 02/09/2020 12:39 Quote Irina:

I quote Anna: Don’t be misled. Adjustment only based on a claim for a defective product. If you decide to return a quality product after the transfer of ownership, then this is a reverse sale if the seller agreed to take it back.

You are misleading.

What if the product was purchased in 2022 at a rate of 18%, and then sold back in 2022 at a rate of 20%? And at whose expense is the difference? )) Read the new legislation! Since last year, there is no concept of reverse implementation. Well, you decide what business transaction you want to reflect: return of goods or sell this product to the buyer (reverse sale)? The article talks specifically about returns, so the rate is 18%. Quote 0 PAWS 02/01/2020 02:54 Hello! How is the return of goods reflected by the seller?

Quote

0 Irina 01/27/2020 09:12 I quote Alena Mikhailovna Vostrilova:

Good afternoon Is the scheme the same if sales and returns occur in different quarters?

Same Quote

0 Irina 01/27/2020 09:11 Quote Anna:

Don't be misled. Adjustment only based on a claim for a defective product. If you decide to return a quality product after the transfer of ownership, then this is a reverse sale if the seller agreed to take it back.

You are misleading.

What if the product was purchased in 2022 at a rate of 18%, and then sold back in 2022 at a rate of 20%? And at whose expense is the difference? )) Read the new legislation! Since last year, there is no concept of reverse implementation. Quote 0 Anna 01/26/2020 14:34 Don’t be misleading. Adjustment only based on a claim for a defective product. If you decide to return a quality product after the transfer of ownership, then this is a reverse sale if the seller agreed to take it back.

Quote

0 Irina 01/20/2020 16:39

Quote

0 Alena Mikhailovna Vostrilova 01/20/2020 14:27 Good afternoon! Is the scheme the same if sales and returns occur in different quarters?

Quote

Update list of comments

JComments

Laws

It is possible to return products to the supplier without conflict situations if the documentation is completed correctly. And also if you remember about the legislation that governs the return rules.

Art. 475 of the Civil Code of the Russian Federation. If defects are detected, the buyer-entrepreneur may demand:

- reduce the amount paid or demand that all violations be eliminated within a reasonable time;

- claim a refund for the money spent on fixing the problems yourself;

- if significant or irreparable deficiencies are identified, the buyer can completely withdraw from the contract and receive the finances back;

- is able to claim the right to replace a low-quality product with something that fully complies with what is specified in the contract.

Art. 476 of the Civil Code of the Russian Federation. The supplier is obliged to bear responsibility for defects that appear before the start of sales. There are 4 reasons why he will have to bear responsibility if he cannot prove the occurrence of violations after the transfer of the cargo to the customer.

Among them:

- violation of storage conditions;

- damage by third parties;

- misuse;

- irresistible force.

Quality is checked by a special supply agreement concluded by the parties. If it is not there, then everything is studied according to Art. 474 Civil Code of the Russian Federation.

Art. 477 Civil Code of the Russian Federation. During use of the purchased item, flaws or noticeable defects appeared. This also allows you to send it back at the designated time:

- until the warranty or the period for which the product is designed has expired;

- if this is not established, then within 2 years from the date of purchase.

Refund to the buyer not on the day of purchase

Such situations happen more often. After all, the buyer, as a rule, becomes convinced that the product is not suitable when he returns home, when he examines and checks it properly.

What are the rules for returning money to the buyer in this case?

He must write an application for a refund. The application form is arbitrary, but it must indicate the buyer’s full name, the name of the product in accordance with his passport or document confirming payment for the goods, the reason why the product is being returned, as well as the requirement to replace the purchase or return the money for it. The form and sample application for returning goods can be downloaded on our website.

In addition, the buyer presents a receipt and passport.

Just as in the first case, it is necessary to issue an invoice, which is signed by both the seller and the client.

Refunds to the buyer must be made within three days after the request.

Please note: if you have several cash registers, then the money in this case should be returned not from the operating room, but from the main cash register of the organization. In this case, there is no need to draw up a KM-3 act on the return of money - the money is issued according to a cash receipt order based on the buyer’s passport. After this, the cashier records the RKO in the cash book. The expense order form can also be downloaded for free on our website, and instructions for filling it out are also published there.

Once again we list the documents for returning goods from the buyer not on the day of purchase. A check, passport and application are required from the client. The seller fills out the invoice for the returned goods, for example, according to the TORG-13 form, signs it from the buyer and issues money according to the cash receipt order.

Ready-made solutions for all areas

Stores

Mobility, accuracy and speed of counting goods on the sales floor and in the warehouse will allow you not to lose days of sales during inventory and when receiving goods.

To learn more

Warehouses

Speed up your warehouse employees' work with mobile automation. Eliminate errors in receiving, shipping, inventory and movement of goods forever.

To learn more

Marking

Mandatory labeling of goods is an opportunity for each organization to 100% exclude the acceptance of counterfeit goods into its warehouse and track the supply chain from the manufacturer.

To learn more

E-commerce

Speed, accuracy of acceptance and shipment of goods in the warehouse is the cornerstone in the E-commerce business. Start using modern, more efficient mobile tools.

To learn more

Institutions

Increase the accuracy of accounting for the organization’s property, the level of control over the safety and movement of each item. Mobile accounting will reduce the likelihood of theft and natural losses.

To learn more

Production

Increase the efficiency of your manufacturing enterprise by introducing mobile automation for inventory accounting.

To learn more

RFID

The first ready-made solution in Russia for tracking goods using RFID tags at each stage of the supply chain.

To learn more

EGAIS

Eliminate errors in comparing and reading excise duty stamps for alcoholic beverages using mobile accounting tools.

To learn more

Certification for partners

Obtaining certified Cleverence partner status will allow your company to reach a new level of problem solving at your clients’ enterprises.

To learn more

Inventory

Use modern mobile tools to carry out product inventory. Increase the speed and accuracy of your business process.

To learn more

Mobile automation

Use modern mobile tools to account for goods and fixed assets in your enterprise. Completely abandon accounting “on paper”.

Learn more Show all automation solutions

Registration of goods return in 1C:UNF

The return of goods sold at retail is done in the “Cashier Workplace”. It's in "Sales". The next steps are determined based on whether it is necessary to process the return of retail goods at the checkout during the current or past shift.

Return on an open cash register

Let's go to "Return". Let's find and select a receipt here to accept returned goods from the buyer in the system. To receive the document online, click on “Create a cash register receipt for a refund.”

In the table of the electronic form of the document, go to “Goods and Services”. Here you need to leave the products you are interested in from the list. Then, through “Punch a Receipt”, register the arrival of the goods returned to the warehouse with the accrual of funds to the client. After this, all that remains is to close the document.

Return via closed cash register

When returning what was sold during a previous and already closed shift, we act in a different way. First, let's set up a variation of processing the return of goods for the required cash register shift. To do this, let's go to "Sales". Let's go to “Settings” - “Even more options”. Here we select “Retail Sales”.

In the “Cashier Workplace” section, you need to select a period for searching for a receipt in order to return goods from the client. You have to find the check by number. Next, create a document through the option of creating a KKM receipt for a refund. All subsequent actions are similar to the situation of posting a transaction and a document for the return of goods in an open shift.

Reasons

Return of defects to the supplier is permitted if the defects are not indicated in advance in writing. This applies to both the entire product and individual parts. In reality, you can return it in different situations:

- products that do not meet quality standards, with visible flaws inside, on the container or box;

- differences in the amount of pieces, type, other features;

- the characteristics included in the contract do not work or are missing.

To determine discrepancies based on barcodes, volume and other parameters at the time of acceptance, it is worth installing special equipment. The use of a data collection terminal ensures that possible differences can be quickly identified - just scan the packaging to count it. After confirmation, the data will go into the database and be registered.

The presence of extra boxes, a lack of required packs, a different volume, color or similar appearance will be immediately determined by the technology. To install and configure the correct software and purchase suitable devices, you should contact Cleverence. The company will recommend quality equipment to help minimize costs and expenses due to unscrupulous contractors.

Basic provisions for returning goods

If the question arises of how to process the return of defective goods to a supplier, you first need to determine the main components of this operation.

In essence, a return represents the return sale of goods to the seller, so such a transaction can be reflected in the reporting as a sale. However, this is only one of the options for recording the return of goods in reporting. It is used if the product was originally of high quality, but for some reason it did not suit the buyer.

If the product turns out to be defective, its return is not a separate transaction; the provision on this is fixed in the Civil Code. Chapter 30 details the grounds on which the buyer has the right to refuse a defective purchase and demand a refund from the seller.

Also see “How to write a letter to return goods to a supplier: sample.”

How to properly prepare documents for returning any goods to the supplier

We recommend that you complete the documentation correctly. To understand what papers to prepare and send to the contractor, you should find out whether ownership of the object has been transferred to the acquiring party. If you haven’t already, everything will be as simple as possible.

There are only 3 possible scenarios:

- identified simultaneously with acceptance - there is no need to accept such products;

- the discrepancy was not identified immediately;

- by agreement, the contractor regularly picks up questionable cargo and those that were not sold within the sales deadline.

Sample return invoice to supplier

Each institution independently decides which forms of primary documentation to use in accounting: either unified forms, or developed and approved independently (Federal Law dated December 6, 2011 No. 402).

IMPORTANT!

When developing your sample invoice for returning goods to the supplier, make sure that all the necessary details are indicated in the document form. Otherwise, the document will be considered void.

Registration of correct return of any low-quality goods to the supplier, important documents

The purchaser must notify the contractor immediately of any defective parts found in the lot. If you do not follow this rule established by Art. 483. Civil Code, the seller has the right not to accept the returned property.

For example, if an organization accepted a delivery without checking and did not report any defects, then even the court will not satisfy the requirements.

According to Art. 514, if everything is later sent back, the recipient is obliged to place the entire thing for safekeeping. His job will be to ensure the safety of the boxes until the shipper picks them up. If the manufacturer agrees with the existing defects and exports the batch, then the parties conclude:

- act of identifying inconsistencies (can be drawn up in the TORG-2 form);

- return invoice (TORG-12 is suitable as a basis).

If the purpose of sending products to the seller is to replace non-critical components or eliminate other minor defects, then everything must be done in writing. The days or weeks in which the shipper undertakes to replace defective parts, replenish or exchange parts should be agreed upon and specified in the documentation.

When the seller denies the possibility of violations, does not export and does not agree to change the defect, evidence is drawn up:

- claim;

- protocol according to which samples were taken for examination;

- a written or registered letter offer to participate in the inspection;

- expert opinion.

We must not forget that the statement of defects, written only by the recipient’s enterprise, only in a limited number of cases serves as an evidence base. This works if, when concluding the contract, both parties signed an agreement to apply such instructions. If it was not compiled, then it will not be evidence.

Refund to the buyer on the day of purchase

If a visitor who bought a product from you changes his mind immediately after that, then the procedure for returning the money is as follows. The buyer presents a cash receipt or sales receipt, or another document confirming payment. If the receipts have not been preserved, he, as stated above, can refer to witness testimony confirming the fact of the purchase.

How to properly process the return of goods from the buyer in this case? It is necessary to fill out an invoice, for example, according to the TORG-13 form. In this case, the buyer’s data is indicated in the “Sender” column, and the seller organization’s data is indicated in the “Recipient” column. The document is drawn up in two copies. It is signed by the seller and the buyer. For the seller, the invoice is the basis for adjustment entries, and for the buyer - for a refund (or for exchanging the product for a similar one, if an exchange is made). You can download the TORG-13 form for free on our website.

The buyer must pay the money from the same operating cash register in which the receipt for the purchase of the returned goods was punched. Moreover, they must be given before the shift is closed and the Z-report is taken. When closing a shift, you will need to draw up a statement of return of funds using the unified form KM-3. On our website you can find a free sample of filling out the KM-3 act.

At the end of the shift, the cashier indicates the amount that was paid to the buyer in the cashier-operator's journal. It must also be reflected in the cashier-operator’s certificate-report. If there are several cashiers, then the senior cashier must, along with other data, indicate the amount of refunds to customers in a summary report for all cash registers.

So, once again about the documents for returning goods from the buyer on the day of purchase. The client brings a check, the seller issues an invoice for the returned goods, for example, according to the TORG-13 form, and the KM-3 act.

Grounds for returning quality goods to the supplier

Broken or incomplete shipments are not always returned. Sometimes you have to send fully working equipment or furniture because:

- other people claim these products (according to Article 460);

- the volume does not match - it is more or less than necessary (Article 466);

- incorrect assortment matrix - unordered color, taste, functionality (Article 468);

- incomplete set or refusal to complete the set (Article 480).

The list cannot be called complete. You can agree to change the conditions or supplement them. The contract includes the possibility of re-loading items not sold on time. For this, an additional formal basis is usually prescribed:

- there is no demand for the model;

- the product is expired;

- the season in which the part is sold has ended;

- other agreed justifications.

These are just some of the reasons why you can return a quality product to the supplier: the return procedure here does not differ from the main sequence. But there are also situations when there are no complaints at all, but the delivery is sent back.

To timely check the quantity and range of supplied cargo, you can go in two ways. An employee can look at each box, compare contents and check barcodes manually. But there is a faster way - simply install special software.

To do this, just contact Cleverens. The company will select the right equipment for the business, which will simplify not only acceptance, but also automate many other processes. This will minimize costs and problems with mis-grading and quantity discrepancies, and will make accounting faster.

Reasons for return

Before moving on to the postings, let us clarify that the customer has the right to return purchased products in a number of cases:

- the contractor supplied low-quality or defective products;

- the quantity supplied does not match the contract documentation;

- delivery and acceptance documents are completed with errors or are not provided to the buyer at all;

- the assortment range of the order is disrupted;

- the shipped products are not packaged appropriately;

- the buyer returns unsold remaining goods, etc.

In all of the above cases, the return of the goods to the supplier is issued, the entries are drawn up by both the consumer’s accountant and the seller’s responsible specialist.

How to document return of unrealized

It is important to remember that returning quality products is allowed only if this is agreed in advance in the contract. Otherwise, you won’t be able to send the sofa back just because it’s not for sale.

There is another way. If such a procedure is not documented, but the companies have agreed on the possibility of such outcomes, then it is permissible to simply formalize a reverse sale. For example, if not all bicycles are sold before the end of summer and the manufacturer agrees to take them back.

In fact, this will be the sale of his own packages to the former owner. Created:

- TORG-12;

- invoice.

The name of his own company is entered in the “seller” line, and the buyer is a contractor who removes his former cargo in the cell. There is no need to fill out TORG-2 according to the sample. Documentedly, such castling does not differ from a regular sale.

How it is issued in different cases

What to do if you brought expired milk or a cake for sale - send it back. But the papers must be drawn up correctly. The supplier will not need to document the return of goods if it is a trusted partner who guarantees to replace everything as soon as possible.

If the shipper does not mind picking up the defect that was sent by an inattentive employee, then you don’t even have to write additional documents. It is enough to cross out items from the invoice that will not be accepted onto the company’s balance sheet. The driver will load them back into the car and take them to the warehouse from which they came.

They will not be reflected in accounting. But the representative of the second party must also sign, so he will confirm that the procedure took place with his participation. Within 5 working days, the shipper sends a new document with corrected figures.

If the relationship with the contractor is trusting and cooperation has been going on for many years, a simpler option is also possible. The receiving party signs the invoice without changes, calls the sender and tells about the poor quality of the delivery. He promises to deliver quality products in a short time.

The latter method is good because there is no red tape, no possible inconsistencies, and quick operations through the base. But it is recommended to use it only when working with a trusted counterparty.

What you need to pay attention to when returning goods from a buyer in 1C 8.3

Registration of the operation of returning goods from the buyer in 1C 8.3 Accounting depends on some nuances:

- whether the buyer is a VAT payer;

- whether the goods are registered with the buyer before they are returned;

- the entire batch of goods or only part of it is returned.

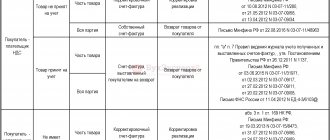

There is a solution for every situation. You can familiarize yourself with processing a return from a buyer in 1C and regulations in the table.

When returning goods by buyers who do not pay VAT, suppliers apply the general procedure for applying and processing deductions provided for in clause 5, clause 13 of Art. 171 Tax Code of the Russian Federation, clause 4, clause 10 art. 172 of the Tax Code of the Russian Federation (Letter of the Federal Tax Service dated May 14, 2013 N ED-4-3/ [email protected] ):

- when part of the goods is returned by the supplier, an adjustment invoice is generated and reflected in the purchase book;

- When returning an entire item, the supplier records the original invoice issued for that item in the purchase ledger.

As for the case of signing an agreement on non-issuance of invoices between a supplier and a buyer who does not pay VAT, this situation is not clearly established in the legislation. In our opinion, the supplier has the right to deduct VAT, calculated earlier upon shipment, on the basis of a primary document (for example, a shipping invoice), which must be registered in the purchase book (clause 1, clause 3, article 169 of the Tax Code of the Russian Federation, Letter of the Federal Tax Service dated 01/27/2015 N ED-4-15/ [email protected] ).

Return of goods to 1C: new rules from 2022 (from the broadcast recording dated February 6, 2022)

Let's look at how to return goods from a buyer in 1C in various circumstances and what postings are generated by 1C Accounting 8.3 in each case.

Registration procedure

There are two types of documents that must be properly prepared in order to make a return:

- claim;

- Act.

The first paper is drawn up on the organization’s letterhead. The signature of an accountant or other person authorized to sign the documentation is required.

Always indicated:

- legal and actual address;

- full title;

- information about the buyer - details, name, other information;

- information about the supply agreement that caused the claim, date, number;

- the reasons for creating the paper are described in full and in detail - discrepancies in quantity, quality, set;

- it is recommended to refer to the law;

- justification for the requirement - return, exchange, complete;

- time limits are established within which the supplying party must review and provide a written response;

- a census of everything invested.

Additionally, a return certificate is drawn up. This is a document that is drawn up by several authorized persons of the receiving company. It is confirmed by the results of the examination and is considered an official document sent from the buyer to the seller.

Here you need to provide information:

- date and place;

- details of both organizations;

- the name of the service or thing that is the basis;

- expert opinion;

- signs how purchased products will be returned to the warehouse;

- indicate invoice details for reverse transfer for low-quality goods;

- if there is compensation - terms and amounts;

- signatures;

- print.

Both parties will sign, but only the manager or other authorized person on each side. His right must be confirmed by a special power of attorney, otherwise the document has no legal force.

What documents should I submit to return goods to the supplier?

Before starting the return shipment procedure to the seller, send him a written notice or simply a letter (Article 483 of the Civil Code of the Russian Federation) to coordinate the shipment. The procedure must be formalized to eliminate controversial situations.

IMPORTANT!

If the contract specifies the conditions for the return of products or the procedure is carried out on legal terms, then there is no need to draw up an additional agreement to the contract. In other cases, it is necessary to change the terms of the contract or conduct a separate transaction that details the conditions for the return of purchased products to the supplier.

The main document confirming the fact of return shipment of purchased products is the product return certificate. For registration, you can approve your own form, taking into account the specifics of the institution, or use the forms approved by Resolution of the State Statistics Committee of December 25, 1998 No. 132:

- TORG-2 (OKUD 0330202);

- TORG-12 (OKUD 0330212).

The act can be drawn up both in written and printed form. When drawing up the document, please indicate the required details:

- Date and place of document preparation.

- Full name of the counterparties participating in the return procedure.

- Detailed list of materials, products, products.

- Reasons for carrying out the return procedure.

- Link to a document confirming the buyer’s legal right to return the product. The results of an independent examination of product quality, a link to violated clauses of the contract, and specifications may be indicated here.

- Terms and conditions for the return transfer of materials (buyer’s requirements).

- Details and signatures of the parties, seals (if any).

Please note the rule: only managers or authorized representatives of the parties can sign the act. You can confirm your authority with a power of attorney of the established form (form M-2). The document is drawn up in the required number of copies, but not less than two (for the supplier and the buyer). Be sure to attach a return invoice, a letter of claim (accompaniment letter), and the results of an independent examination of product quality (if defective material is supplied) to the report.

Ready-made solutions for all areas

Stores

Mobility, accuracy and speed of counting goods on the sales floor and in the warehouse will allow you not to lose days of sales during inventory and when receiving goods.

To learn more

Warehouses

Speed up your warehouse employees' work with mobile automation. Eliminate errors in receiving, shipping, inventory and movement of goods forever.

To learn more

Marking

Mandatory labeling of goods is an opportunity for each organization to 100% exclude the acceptance of counterfeit goods into its warehouse and track the supply chain from the manufacturer.

To learn more

E-commerce

Speed, accuracy of acceptance and shipment of goods in the warehouse is the cornerstone in the E-commerce business. Start using modern, more efficient mobile tools.

To learn more

Institutions

Increase the accuracy of accounting for the organization’s property, the level of control over the safety and movement of each item. Mobile accounting will reduce the likelihood of theft and natural losses.

To learn more

Production

Increase the efficiency of your manufacturing enterprise by introducing mobile automation for inventory accounting.

To learn more

RFID

The first ready-made solution in Russia for tracking goods using RFID tags at each stage of the supply chain.

To learn more

EGAIS

Eliminate errors in comparing and reading excise duty stamps for alcoholic beverages using mobile accounting tools.

To learn more

Certification for partners

Obtaining certified Cleverence partner status will allow your company to reach a new level of problem solving at your clients’ enterprises.

To learn more

Inventory

Use modern mobile tools to carry out product inventory. Increase the speed and accuracy of your business process.

To learn more

Mobile automation

Use modern mobile tools to account for goods and fixed assets in your enterprise. Completely abandon accounting “on paper”.

Learn more Show all automation solutions

What you should know about - tax issues

There are several nuances, knowledge of which will simplify the procedure:

- If the products were not accepted, then a separate operation is not created. In this case, VAT is not paid and the buyer does not issue an invoice. The shipper will send him the corrected papers.

- If everything was accepted at first, but then violations were discovered, separate documentation is drawn up. It's paper and procedure. First, the consignee sends an invoice to the supplier, who will accept VAT for deduction. If necessary, the owner of the outlet restores the tax amount, this is done in the same period with the actual refund.

Sometimes the parties agree that defective items must be disposed of. In this case, the shipper attributes the costs to expenses from defects.

Accounting in accounting and balances

There are only three paths you can take to reflect changes in the program:

- The simplest one, for those who have been collaborating for a long time. Don't make any notes, accept everything on the list, then call the supplier and report any discrepancies. He brings a quality replacement.

- More difficult if the goods have not yet been accepted. Note the differences on the invoice and cross out what is not accepted. Sign, get the driver's signature. Wait for new documents from him in which the information has been corrected.

- If the product was accepted, but then a discrepancy was discovered. A consignment note TORG-12 and an act TORG-2 are drawn up. The seller must agree with the violations.

- If he does not agree, then a claim is drawn up, a protocol on sampling is drawn up, and the shipper is invited for an examination.

Return of goods from the buyer in retail BP 3.0

If goods are returned by the buyer, the amount of VAT paid by the seller is subject to tax deduction no later than one year from the date of return or refusal by the buyer. The Federal Tax Service recommends registering an adjustment document in the purchase book with summary data on return transactions from retail customers. Let's consider the procedure for reflecting a return from a buyer in retail trade in 1C: Enterprise Accounting 3.0. On January 15, 2022, goods were sold to the buyer using the “Retail Sales Report” document ( Sales – Retail Sales Report

).

The following entries have been generated:

An entry was made in the accumulation register “VAT Sales” to create a sales book for the 1st quarter of 2022:

Also, the implementation was carried out on January 29, 2022.

In case of failure to issue invoices for retail sales, it is necessary to create a summary certificate for retail sales transactions ( Sales – Invoices issued – Create – Summary certificate for retail sales

).

In the " from" field:

» the last day of the month for which the certificate will be generated is set. By clicking the “Fill” button, the documents will be automatically selected for the certificate.

When posting, an entry is made in the “Invoice Journal” register to register the document in the sales book. The summary certificate will be registered in the sales book for the 1st quarter of 2021 with the transaction type code “26” “Sales of goods, works, services to VAT evaders, receipt of advances.”

Let's create a sales book and check the data in it (

Reports - Sales Book

).

In February 2022, goods sold in January were returned. The return is registered in the program in the “Retail Sales Report” document in the “Returns” tab (Sales – Retail Sales Report). To correctly reflect the return transaction in VAT accounting, it is important to indicate the date of sale of the returned goods in the tabular part of the document.

When posting a document, the following transactions are generated:

And an entry is made in the accumulation register “VAT Sales” to create a sales book for the 1st quarter of 2022:

The return data is included in the accumulation register “VAT presented”:

And to create a purchase book for the 1st quarter of 2022, an entry was made in the accumulation register “VAT Purchases” for returns:

In February, a Summary Certificate of Retail Sales was also compiled to further fill out the sales book for February 2021 ( Sales – Invoices issued – Create – Summary Certificate of Retail Sales

).

Since this month there was a return of goods from a retail buyer, it is necessary to create an Adjustment Certificate for Retail Sales ( Sales - Invoices issued - Create - Adjustment Certificate for Retail Sales

).

In the window that opens, select the summary certificate for which the adjustment certificate is being prepared (Summary certificate for February in the example).

In the " from" field:

» the last day of the month for which the certificate will be generated is set. By clicking the “Fill” button, the documents will be automatically selected for the certificate.

When the document is posted, a register entry “Invoice Journal” is generated for further filling out the purchase ledger:

Having generated a purchase book for the 1st quarter of 2022 (

Reports – Purchase Book ) of the year, we will see there a record of returned goods from an individual. Transaction type code “17” “Return from an individual buyer.”