Representation expenses: what is included

Not all types of expenses can be included in a company’s entertainment expenses.

It is important for taxpayers to understand the issue. Otherwise, problems with the Federal Tax Service cannot be avoided. If the company takes into account unauthorized expenses as part of entertainment expenses, the inspectorate will regard the situation as an understatement of the tax base. The result is fines, penalties and arrears. What applies to entertainment expenses:

- The company's expenses for receiving guests from other companies in order to start new cooperation or strengthen old business relationships.

- Costs of receiving members of the management board, board of directors, representatives of the founder or owners.

The definitions are enshrined in paragraph 2 of Art. 264 Tax Code of the Russian Federation. But the concept of “receiving guests” is quite vague. What exactly can be included in this position? Officials have strictly defined the framework for the situation: it is allowed to take into account the following as part of the cost of admission:

- delivery of guests or management representatives to the event (transport services);

- organizing catering during events, for example paying for a buffet;

- translation services, if necessary, for example, if a meeting of foreign guests is organized.

But entertainment, accommodation, recreation and even treatment of guests and board representatives cannot be included in the designated costs. Such enterprise costs cannot be offset when taxing profits.

List of documents

Giving explanations on the issue of registration of this type of expense, officials provided a list of necessary documents (letter of the Ministry of Finance dated November 1, 2010 No. 03-03-06/1/675). Let's list them:

- estimate of entertainment expenses (quarterly, annual, etc.), approved by the founders of the company;

- order of the general director on the implementation of entertainment expenses (for example, an order on entertainment expenses for tea and coffee);

- report on the event related to entertainment expenses;

- act on the implementation of entertainment expenses.

According to the officials, the company must develop these documents independently and approve them, including them in the relevant local act (Article 313 of the Tax Code of the Russian Federation).

In recent clarifications from financiers and tax authorities, the requirements for registration have become less. Companies are required to provide only two documents:

- report on entertainment expenses;

- advance report.

Together with the primary documents attached to them confirming specific expenses, they must fully satisfy the interest of the controllers (letter of the Ministry of Finance dated April 10, 2014 No. 03-03-R3/16288).

However, in practice, tax authorities may not be satisfied with these reports. Therefore, it is safer to draw up documents according to the first list. Including, drawing up an order on entertainment expenses for a management meeting. We present to our readers a ready-made sample that can be downloaded for free on the website.

Principles of rationing

In accordance with paragraph 2 of Art. 264 of the Tax Code of the Russian Federation, the standard for entertainment expenses in 2022 is defined as 4% of labor costs for the same reporting or tax period.

Taxpayers have the right to choose the method of accounting for expenses for events. There are three ways provided by law:

- Quarterly calculation. Costs are calculated quarterly. Moreover, expenses are reflected in the income tax return. The method is convenient for companies that reflect costs on a cash basis. If entertainment costs exceed the established limit, then a deferred tax liability is reflected in accounting, which can be taken into account at the end of the year.

- Annual count. The taxpayer determines the limit of costs for activities for the year in advance. Calculations are approximate, the assessment is carried out based on the company’s estimate or financial and economic activity plan. At the end of the year, it is necessary to make adjustments and bring the planned values to actual indicators.

- Official way. The company approves a list of officials who have the right to organize such events. Moreover, you must comply with the 4% limit and acceptable spending goals.

Report on entertainment expenses: example

The report is also compiled in free form and is a summary of the past event:

- when and where the event was held;

- its results and agreements (or lack thereof);

- who served this event (a third-party organization, or everything was prepared by company employees)

- expenses for the event (they must be documented);

- a list of supporting documents that will be attached to the report.

All supporting documents must be original.

Remuneration: how to calculate the standard

It is possible to correctly calculate the standard only by determining what exactly is included in labor costs. When resolving the issue, you should be guided by Article 255 of the Tax Code of the Russian Federation.

The list of company expenses related to wages is open. That is, it can be any expenses that meet the required conditions:

- accruals in favor of the company's employees are made on the basis of current legislation;

- the conditions and amounts of payment are fixed in employment contracts, the calculation rules are established in the regulations on remuneration and the collective agreement;

- all types of accruals in favor of employees must be documented and have an economic justification (Article 252 of the Tax Code of the Russian Federation).

The company has the right to determine costs either on an accrual basis or on a cash basis. The decision must be fixed in the accounting policy.

Representation expenses and their accounting in 1C: Accounting

Published 12/18/2019 12:12 Author: Administrator First, let's define what we mean by the definition of “representation expenses”. The word “representative” means a person who represents someone’s interests, in our case, the enterprise for which he works. Accordingly, entertainment expenses include business meetings with clients, gathering members of the organization’s board, and receiving foreign representatives of foreign companies. Let's look at the reflection of such expenses in accounting and tax accounting using practical examples in 1C: Accounting.

In accounting, the reflection of entertainment expenses usually does not raise questions, since they are fully debited to expense accounts determined in accordance with the goals of the event. For example, if an expense is directly related to production, then choose the debit of account 20, and if with sales, then 44. You can also assign them to account 26 if these expenses belong to the entire enterprise.

The Tax Code states that entertainment expenses include the following expenses:

- related to the official reception and service of representatives of other companies participating in negotiations in order to establish or maintain mutual cooperation;

- related to organizing the reception of participants who arrived at meetings of the taxpayer’s governing body;

— for transportation of the above-mentioned persons to the venue of the event or meeting and back;

— for buffet service during negotiations;

— to pay for the services of translators who are not on staff.

From the above it follows that entertainment expenses in tax accounting can be divided into 2 types: those listed in paragraph 2 of Art. 264 of the Tax Code of the Russian Federation, and those that cannot be taken into account in tax expenses. For example, visiting a theater with a client to establish a more friendly relationship, in fact, should be treated as entertainment expenses, but not in tax accounting.

To reflect the second type of expenses, it is recommended to select account 91.02 and the item of other expenses that are not accepted for tax accounting.

The first type of entertainment expenses is accepted for tax accounting, but only within the limits of standardization - 4% of the wage fund.

What documents will confirm the presence of entertainment expenses in the organization?

Firstly, an order from the manager, which determines the date and purpose of the event and appoints someone responsible for its implementation.

Secondly, the cost estimate approved by the manager.

Thirdly, a report on the event, indicating the list of guests and the amount of expenses.

And the fourth, most important point is primary documents confirming purchases and payments for services provided. For example, invoices, acts, checks.

Reflection of entertainment expenses in 1C: Accounting can be implemented by entering one or several documents:

— Receipts (acts, invoices) in the “Purchases” section, in case of closing expenses directly from suppliers,

— Advance report (section “Bank and cash desk”), if funds for organizing the event were issued to an employee of the enterprise.

Let's consider both options.

Reflection of entertainment expenses in 1C using the document “Advance report”

In the “Bank and Cash Office” section, select the “Advance reports” item and use the “Create” button to enter a new document.

We set the required date and select the employee who provided the reporting documents. On the “Advances” tab, using the “Add” button, you need to select the document with which the issuance of funds to an accountable person was registered (the issuance of accountable funds must be made before the employee spends them either in cash through the enterprise’s cash desk, or by transfer to the current account of the organization’s employee).

Next, go to the “Other” tab and reflect the entertainment expenses incurred by the employee. Let’s assume that the only type of expense in our case was buffet service for representatives of other companies costing 5,000 rubles when the wage fund for the current month is equal to 100,000 rubles. Let’s add a line on the “Other” tab and indicate the document evidencing the expense, its date, number, content of the transaction, amount, and most importantly, the invoice and expense item.

As an example, we will select expense account 26 and create a new (if not previously entered) cost item with the type “Representation expenses”.

As you remember, entertainment expenses must be rationed, and for the purposes of our example, it was not without reason that the payroll equal to 100,000 rubles was chosen. After all, 4% of 100,000 rubles is 4,000 rubles, and entertainment expenses amounted to 5,000 rubles. Accordingly, it will not be possible to accept representative tickets in full this month.

The standard is calculated at the end of the month.

Let's go to the "Operations" section and select the "Month Closing" item. Let’s start processing by clicking on the “Perform monthly closing” button and analyze the transactions for the operation “Calculation of shares of write-off of indirect expenses”.

Postings for this operation are indicated in shares accepted for tax accounting of expenses. That is, expenses for entertainment events amounted to 5,000 rubles, but we can only accept 4,000 rubles.

We get: 4000/5000 = 0.8.

On the second tab “Calculation of standardization of expenses” you can see both the amount of entertainment expenses and the accepted standard.

Next month, after payroll is calculated, the standard will be increased, and those expenses that we could not accept in the current month will be carried over to the next one. But only within one calendar year.

Reflection of entertainment expenses using the document “Receipts (acts, invoices)”

In the second example, we will consider entertainment expenses for visiting the theater, which we cannot accept for tax accounting.

In the “Purchases” section, select the “Receipts (acts, invoices)” item. Click on the “Receipt” button, from the drop-down menu we are interested in the “Services (act)” item.

Enter the date and number of the primary document, select the service provider. Using the “Add” button, enter the information provided, indicate account 91.02 and select from the directory “Other income and expenses” a line that is not accepted for tax accounting. If the required line does not exist, then it must be created.

The completed document will look like this:

The posted document will create entries for the debit of account 91.02 and credit 60, and will also assign the amount not accepted as expenses in tax accounting to the official off-balance sheet account HE.03.

Author of the article: Alina Kalendzhan

Did you like the article? Subscribe to the newsletter for new materials

Add a comment

Comments

0 Alexander 07.27.2021 14:24 Is it possible, when receiving an advance for entertainment expenses in cash, to submit reporting documents (check) paid by non-cash

Quote

Update list of comments

JComments

Features of documentation

Any company expenses taken into account for taxation must be justified and documented. Entertainment expenses should be properly documented. Moreover, no special forms are provided. Provide templates and a list of supporting documentation in your accounting policies.

It is recommended to use the following documents:

- Order of the head of the organization to hold a representative event. Be sure to indicate in the order the date, place and time of the reception. Also outline the goals of the event.

- Program for hosting guests or board members. Prepare the event program as an appendix to the order. Separately, the paper will not have much weight.

- Cost estimates for events. Indicate in detail all categories of costs that are aimed at hosting guests.

- Report on the event. Compiled in any form by the person responsible for organizing and conducting the reception. It is required to indicate the results of the event.

- Act on write-off of expenses and payment documents. Please note that the write-off act must be signed by the chief accountant. And the manager approves the act.

Documentation is required. During an on-site inspection by the Federal Tax Service, inspectors will definitely request forms.

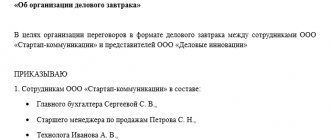

Sample order for entertainment expenses of an enterprise

An order for entertainment expenses is drawn up in the form of an administrative document for the organization, on company letterhead. It contains information about the upcoming event, its goals and expected costs.

An approximate order structure would look like this:

- details of the order (name of organization, date, number, title);

- preamble revealing the purpose of drawing up the order (brief description of the event);

- the administrative part of the order, indicating what needs to be prepared for the upcoming event and identifying the responsible persons;

- manager's signature.

The order may also contain instructions on the need to draw up a report and act for entertainment expenses upon completion of the business event.

Tax accounting

Not all companies can offset entertainment expenses for tax purposes: the 2022 tax accounting standard can only be used by taxpayers using the general taxation system. Other companies and individual entrepreneurs do not have the right to do this.

Even companies that have chosen the simplified tax system “income minus expenses” do not have the right to count entertainment expenses when calculating the simplified tax, since such expenses are not specified in Art. 346.16 Tax Code of the Russian Federation. Consequently, not a single taxpayer who uses lenient encumbrance regimes can take into account representative expenses in tax accounting.

Firms using OSNO can not only reduce their income tax, but also offset input VAT on such costs. But it is important to comply with the limit of 4% of the payroll, document expenses and justify them economically.

On the issue of VAT. You can return the input tax, but only within the established limit of 4% of the cost of paying staff. If during the reporting period expenses exceeded the 4% limit, then they can be transferred to the next reporting period.

Drawing up an estimate: we certify the document

Despite the fact that the estimate, as we noted above, can be certified by the head of the company using the “I approve” column, it is also recommended to additionally certify the information reflected in the document with signatures:

- chief accountant;

- the person responsible for preparing the budget.

Their full names and positions are also indicated.

The estimate for entertainment expenses can be either an independent local regulatory act or part of another act - for example, an internal corporate regulation on entertainment expenses. In the second case, it will have to be drawn up in a form that is approved as an annex to the relevant regulation.

Let's study this aspect of using estimates in more detail.

Example: income tax and entertainment expenses

Vesna LLC uses OSNO. In the 2nd quarter of 2022, the company received business partners to conclude a new contract for the supply of products. A total of 250,000 rubles were spent on the event, including:

- transportation costs for delivering guests to the event venue - 20,000 rubles, including VAT - 4,000 rubles;

- catering (breakfast, coffee break, gala lunch, dinner) - 100,000 rubles, VAT - 20,000 rubles;

- services of buffet staff - 30,000 rubles;

- tickets for the theater premiere - 10,000 rubles, VAT - 2,000 rubles;

- accommodation for guests in a luxury hotel - 40,000 rubles;

- excursion by boat to local attractions - 50,000 rubles.

The amount of VAT on all costs for the event is 26,000 rubles.

The wage fund for the 2nd quarter of 2022 amounted to 7,000,000 rubles. 4% of payroll - 280,000 rubles.

Consequently, the company, according to the established limit, has the right to offset entertainment expenses in the 2nd quarter in the amount of no more than 280,000 rubles. But the entire cost of holding events cannot be taken into account! Since not all expenses are representative.

Vesna LLC can accept for tax accounting only the amount of costs for transport delivery of guests, buffet services and meals - 150,000 rubles. But expenses for theatrical performances, boat excursions and hotel rooms cannot be taken into account. These expenses must be paid from the company's net profit. That is, from the money that will remain in the company after income tax.

Input VAT can only be refunded in the amount of 24,000 rubles. That is, only from hospitality expenses (transportation services and food). But you cannot get a deduction from theater tickets.

Document structure

The order is drawn up on the company's official letterhead. There is no officially approved order structure. However, practice shows that the following must be included as integral elements in the order for entertainment expenses:

- corporate name of the taxpayer;

- name of the order (for example, “Order on organizing an event to conduct business negotiations with AAA LLC,” “Order on organizing a banquet for the board of directors,” etc.);

- document serial number;

- date and place of the order;

- the purpose of the document (should not coincide with its title, for example: “to agree on the terms of contact”, “to develop a business development strategy”, etc.);

- Name and position of employees who are entrusted with representing the interests of the company;

- the name of the event (may coincide with the name of the order) and its location;

- cost limit allocated for this event (in table form);

- deadline for drawing up a report on the amounts spent and other related documentation;

- Full name and position of the person controlling the execution of the order.

An order for entertainment expenses is signed by the head of the organization or a person authorized to issue such orders. The officials responsible for execution sign for familiarization with the order. If there are more than 3 of them, it is advisable to put the signatures on a separate sheet, then a sheet of familiarization with the order is drawn up.

Deadlines for drawing up documents

A costs order is always accompanied by additional supporting documents, which are drawn up both before and after the order is made. It can be:

- cost estimates;

- detailed programs of events;

- documents confirming the amount of expenses (for example, contracts for the provision of transport or catering services, checks, receipts, etc.);

- reports;

- acts of acceptance of costs by the manager.

Often, cost estimates are drawn up in organizations in advance, based on the overall business plan for hosting guest events. To coordinate upcoming expenses, as a rule, at the beginning of the year, a general order is drawn up to approve entertainment expenses (or standardize) expenses for a year, six months or month.

The deadline for issuing an order on representation expenses is not defined in the laws of the Russian Federation. According to the general requirements of personnel records management, it is better to issue relevant orders no later than three working days in advance. However, if more time is needed to organize the event, the order should be signed in advance.

Primary documents that reflect the exact amounts of expenses are drawn up in the process of organizing events. They are attached to the reports that are necessary for the accounting service to account for funds issued to employees for organizing events.

After the relevant meetings and negotiations, the employees responsible for the events and the employer sign a statement of entertainment expenses, which reflects:

- work performed by officials, services provided for organizing events;

- actual costs for each category.

Errors when filling out an order

The most common situations occur when an order for entertainment expenses is drawn up without documents that actually confirm the expenses (checks, receipts, estimates, etc.). In this case, if the company reduces the tax base by the amount of such expenses, the tax authority will make additional mandatory payments. Failure to pay additional taxes will result in penalties and fines being collected from the organization.

An order on representation expenses should not be confused with an order on payment for the services of representatives.

The latter contains the manager’s requirement to make settlements with citizens who are not part of the workforce and who are involved under a civil contract for the provision of services to represent the interests of the company in the courts or authorities.