What is a chart of accounts?

Charts of accounts are consolidated documents approved by regulatory legal acts at the federal level.

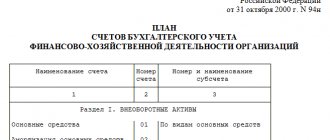

There are several industry-specific types of relevant documents. Thus, the chart of accounts for the commercial sector was approved by order of the Ministry of Finance of Russia dated October 31, 2000 No. 94n. Russian taxpayers must use this document as the basis for creating an internal accounting work plan (paragraph 4 of the Instructions for using the chart of accounts, approved by Order No. 94n).

The accounting plan is a key source for completing the documents that make up the organization's balance sheet. A little later we will look at how their components relate to each other.

In accordance with the internal work plan accounts, firms operating in the Russian Federation carry out standardized accounting of various business transactions related to asset management, fulfillment of obligations, expenditure of funds, extraction of income, etc.

The main elements of the chart of accounts approved by the Ministry of Finance for private companies are as follows:

- numbers and names of main accounts;

- numbers and names of subaccounts.

When forming its own work plan, the organization does not have the right to change the first 2 parameters, but the parameters of subaccounts can. If necessary, the firm can also approve additional subaccounts.

As a rule, to effectively reflect business transactions, the accounts proposed by the Ministry of Finance require further detail. The company can do this by introducing its own analytical accounts, supplementing those recorded in Order No. 94n.

In the Guide to Account Correspondence from ConsultantPlus, you will find typical transactions for any account. If you do not have access to the K+ system, get a trial online access for free.

Let's look at what other accounting plans there are.

Subaccounts or analytical accounts?

The question arises: when is it better to use subaccounts and when to use analytical accounts?

Subaccounts are used to group accounts of the same type and similar in purpose (a bit like groups in directories). For example, account 55 (special bank accounts) is divided into a number of sub-accounts: 55.01 (Letters of Credit), 55.02 (check books), 55.03 (deposit accounts), etc. From this it is clear that there simply cannot be an infinite number of such subaccounts.

But for example, an enterprise may have a lot of counterparties, so it is impractical to allocate its own subaccount for each. It is much easier to use the “Counterparties” analytical account.

From the examples given, it should be clear what the difference is between accounts, their subaccounts, and analytical accounts.

Which legal acts approved the charts of accounts for financial and economic activities?

We noted above that commercial organizations are required to formulate working accounting plans based on the provisions of Order No. 94n. This legal regulation can be supplemented by sources of law that adapt accounting legislation to the activities of certain categories of taxpayers. Among such regulations is Order No. 64n of the Ministry of Finance of Russia dated December 21, 1998, which approved recommendations for accounting for small enterprises.

The need for accounting is also legally established for state and municipal organizations. The main regulatory legal act establishing the accounting plan for such structures is Order of the Ministry of Finance of Russia dated December 1, 2010 No. 157n. There are also complementary sources of law:

- order No. 174n dated December 16, 2010, which approved the accounting plan for budgetary institutions;

- Order No. 183n dated December 23, 2010, which approved the accounting plan for autonomous institutions.

In turn, government organizations are required to work within the framework of budget accounting - a subtype of accounting, adapted mainly for accounting for non-commercial financial transactions. The corresponding chart of accounts is given in the order of the Ministry of Finance of Russia dated December 6, 2010 No. 162n.

A separate accounting plan was approved for banks operating in the Russian Federation by Regulation of the Central Bank of the Russian Federation dated February 27, 2017 No. 579-P.

A separate accounting plan for non-credit financial organizations, approved by the Bank of Russia dated September 2, 2015 No. 486-P. Non-credit financial structures include, in particular, insurance companies. Thus, in the Russian Federation several types of charts of accounts have been established. But the main one for the commercial sphere is traditionally considered to be the one approved by Order No. 94n. Let's study its features, in particular, determine who needs to use it.

Who should use the accounting chart of accounts

The accounting chart of accounts approved by Order No. 94n must be used by organizations that, in accordance with the law, are obliged, firstly, to maintain accounting, and secondly, to use the double entry method in the process of maintaining it. These are all business entities in the Russian Federation, except:

- IP;

- credit and state (municipal) institutions;

- branches and representative offices of foreign companies.

Individual entrepreneurs and branches of foreign companies have the right not to keep accounting records at all. Micro-enterprises and non-profit organizations may not use double entry and therefore not use the accounts recorded in Order No. 94n (clause 2.1 of the information of the Ministry of Finance of Russia No. PZ-3/2015). But in practice, this turns out to be not very convenient, so micro-enterprises, one way or another, still use accounts from those approved by the Ministry of Finance.

For some enterprises, the legislator establishes a preference in the form of the opportunity to maintain a simplified working chart of accounts. Let's consider this aspect in more detail.

Who can use the simplified chart of accounts?

In accordance with information from the Ministry of Finance of Russia No. PZ-3/2015, the preference in question can be used by:

- small businesses;

- NPO;

- companies operating in Skolkovo.

The use of a simplified accounting chart of accounts involves, first of all, reducing the number of synthetic accounts used in the structure of the work plan. Another relaxation is the ability not to use accounting registers in the work (clause 4.1 of information No. PZ-3/2015).

Chart of accounts table with subaccounts: correlation with the balance sheet

So, a significant part of Russian companies are required to work with a standard chart of accounts. The full accounting plan is reflected in order No. 94n in the form of a table. Its structure consists of 8 sections. Let's consider the connection between these sections, including accounts and subaccounts, with sections of the balance sheet.

The accounts of section 1 of the accounting plan are intended to reflect transactions with non-current assets. The balances on these accounts are the source of data for the formation of balance sheet lines in terms of non-current assets.

How to record entries for accounting for fixed assets, read the article “Accounting for fixed assets - accounting entries.”

The accounts of section 2 of the accounting plan are used to reflect business transactions on inventories. The account balance of section 2 is used to fill out the section reflecting current assets in the balance sheet. For a similar purpose, data from sections 3 “Production Costs”, 4 “Finished Products and Goods” and 5 “Cash” of the accounting plan is used.

The working chart of accounts must be fixed in the accounting policies of the organization.

The nuances of forming accounting policies are described in detail in a typical situation from ConsultantPlus. There you will also find an example of a working chart of accounts. If you do not have access to the K+ system, get a trial online access for free.

Read about the reflection of individual transactions in the accounts in our materials:

- “Account 26 in accounting (nuances)”;

- “Accounting for a corporate bank card”;

- “Special equipment in accounting - features and nuances”;

- “Business inventory in accounting is...”.

The indicators reflected in the accounts included in section 6 “Calculations” are used to reflect information about receivables and payables (including long-term ones).

How debt on contributions to the authorized capital is reflected, read the article “Accounting entries on contributions to the authorized capital.”

How to reflect the issuance of imprest amounts, look in the material “Transfer of subaccounts to an employee’s card from a current account.”

Sections 7 “Capital” and 8 “Financial Results” of the chart of accounts contain accounts that reflect data on capital, target financing, and the financial result of the organization.

For entries on accounting for financial results, see the article “Accounting and analysis of financial results.”

The procedure for reflecting retained earnings can be found in the article “Retained earnings in the balance sheet (nuances).”

Synthetic accounting scheme

Each transaction is recorded in the company's accounting using double entry, that is, the debit and credit of two accounts at once. The balance formed as a result of such an entry in one or another account, used according to the chart of accounts to reflect certain actions or events, is an element of synthetic accounting. This is always general information showing the cost equivalent of a specific indicator.

For example, account 10 “Materials” reflects the movement of inventory items owned by the company. The debit balance of this account shows the balance of such valuables as of a certain date. Subaccounts can be used for this account, distributing all materials by type: raw materials and materials, components, fuel, spare parts, equipment, workwear and others. At the same time, all listed inventory items may be located in different warehouses belonging to the same company, and this will also be reflected in the accounting. This detailed information is visible in the account analytics 10.

Another example: for settlements for the purchase of goods, services or works by an organization, synthetic accounting is kept in account 60 “Settlements with suppliers and contractors”. Here, as the name of the account implies, the company reflects its own obligations to the counterparty or, on the contrary, its obligations to the company. Analytical accounting in this case will consist of records in the context of each specific counterparty, a reflection of the listed advances and final payment amounts, as well as the actual facts of receipt of goods, works or services.

New chart of accounts for 2020-2021

Did the 2020-2021 year bring any legislative adjustments to the chart of accounts? The answer to this question depends on the scope of application of the relevant document.

Order of the Ministry of Finance of Russia No. 94n, used by commercial firms, was issued quite a long time ago - about 15 years ago. It can be noted that since that moment, changes have been made to it 3 times:

- by order No. 38n dated 05/07/2003;

- by order of September 18, 2006 No. 115n;

- by order of November 8, 2010 No. 142n.

Thus, the provisions of Order No. 94n have not been adjusted for almost 10 years. So there is no need to say that a new accounting plan for commercial firms has appeared in 2020-2021.

Another thing is state and municipal organizations. The legislator is very active in adjusting the accounting policies of budgetary structures, especially in the main regulatory legal act regulating accounting in budgetary structures - order No. 157n.

Read about changes in the Chart of Accounts for budgetary accounting in this material.

Read more about the structure of the budget accounting account in the article “Typical entries for budget accounting (examples)” .

Where can I download the chart of accounts?

You can download the current chart of accounts for commercial organizations on our website.

This document fully complies with the provisions of Order No. 94n.

Read about what a working chart of accounts for accounting might look like in the article “Working chart of accounts for accounting - sample 2022” .

How is a working chart of accounts formed?

The working chart of accounts is formed on the basis of the Chart of Accounts and with the help of the Instructions for its use. In each organization, from the Chart of Accounts, those work tools are selected that are suitable for a given enterprise to maintain the most convenient and functional accounting. To simplify the preparation of a working chart of accounts, the characteristics of each account are used, which are given in the Instructions and the Chart of Accounts, as well as information about the standard pattern of correspondence of a specific account with other synthetic accounts. Moreover, if standard correspondence is not provided, the organization has the right to supplement it, but in compliance with the uniform approach established by the Instructions.

Certain specifics of some organizations allow them to introduce additional synthetic accounts into the working chart of accounts. But this can only be done in agreement with the Ministry of Finance of the Russian Federation.

The organization's ready-made working chart of accounts is subsequently used as a management accounting tool - a system for collecting, recording and summarizing information about financial and economic activities. This means that it clearly demonstrates to the head of the organization and heads of structural divisions planned, actual information and a possible forecast of the enterprise’s activities, which allows them to make the right management decisions and effectively manage the enterprise’s activities.

When forming a working chart of accounts, the chief accountant of the enterprise determines:

- what synthetic accounts does the company need;

- which analytical accounts should be opened for the selected synthetic accounts.

Results

In the Russian Federation, various charts of accounts are used for budgetary, autonomous, government institutions, credit and non-credit financial organizations, and commercial organizations. For commercial organizations, the chart of accounts was approved by order of the Ministry of Finance of Russia dated October 31, 2000 No. 94n. Small enterprises can use a simplified chart of accounts recommended by the Ministry of Finance in order No. 64n dated December 21, 1998. Each organization must develop a working chart of accounts independently and approve it in its accounting policies.

Sources: order of the Ministry of Finance of the Russian Federation dated October 31, 2000 No. 94n

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

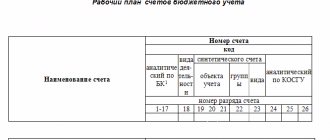

Structure of the working chart of accounts

All accounting operations are reflected in the 26-bit accounts of the working chart of accounts, the structure of which is set depending on the type of institution (state, autonomous, budgetary) and the type of its financial support. The working chart of accounts of any organization has a tree structure and includes:

- Synthetic accounts. They are designed to account for property, liabilities and business processes. They take into account certain types of property, capital, liabilities, as well as financial results.

- Analytical accounts (attached to synthetic accounts). They are used to monitor the safety and movement of accounting objects. In these accounts, calculations are carried out both in physical terms and in monetary terms, detailing information on the contents of the main synthetic account. The enterprise has the right to adjust and clarify the contents of these accounts, and can also completely exclude analytical accounts from its working chart of accounts.

- Subaccounts that detail the main accounts.