To what tax payments can an overpayment of tax be offset?

You can send overpayments of taxes (clauses 4, 5, Article 78 of the Tax Code of the Russian Federation):

- towards upcoming tax payments;

- to pay off debts on taxes, penalties, and fines.

Overpayments can only be offset against taxes of one type. That is, overpayments on federal taxes can be directed toward federal taxes, overpayments on regional taxes can be directed toward regional taxes, and overpayments on local taxes can be directed toward local taxes (clause 1 of Article 78 of the Tax Code of the Russian Federation).

For example, it is impossible to offset an overpayment of income tax against arrears of transport tax, since transport tax is regional, and the overpayment arose for federal tax.

The exception is personal income tax. Its overpayment cannot be offset against future personal income tax payments. But you can direct such an overpayment towards future payments for other federal taxes (clause 1, 14, article 78, clause 9, article 226 of the Tax Code of the Russian Federation, Letter of the Federal Tax Service of Russia dated 02/06/2017 N GD-4-8/ [ email protected] ).

Note that taxes under special regimes - Unified Agricultural Tax, single tax under the simplified tax system and UTII are recognized as federal (Clause 7, Article 12 of the Tax Code of the Russian Federation).

Using the same principle, a credit can be used to pay off penalties and fines (clause 1, 14, article 78 of the Tax Code of the Russian Federation).

If the inspection carries out the offset itself, then it can also offset the overpayment only against debts for taxes of one type, penalties and fines for them (clauses 5, 14 of Article 78 of the Tax Code of the Russian Federation).

Procedure for tax refund (offset)

Application form for tax refunds and credits

Art. 78, 79 Tax Code of the Russian Federation, Order of the Federal Tax Service of the Russian Federation dated February 14, 2017 N ММВ-7-8/182

- Application for a refund

of the amount of overpaid (collected, subject to reimbursement) tax (fee, insurance premiums, penalties, fines), Appendix No.

8

. - Application for offset of

the amount of overpaid (subject to reimbursement) tax (fee, insurance premiums, penalties, fine), Appendix No.

9

.

Reasons for overpayment

- incorrect calculation of taxes, contributions, fees;

- errors when filling out payments;

- introduction of amendments to the Tax Code of the Russian Federation, the effect of which extends to past periods;

- based on the results of the tax period, the amount of tax to be reduced is calculated;

- change in taxation regime.

How to set up an overpayment

clause 6 art. 6.1 Tax Code of the Russian Federation, clause 3, 14 art. 78 Tax Code of the Russian Federation

- independently (audit, inventory of payments...);

- The Federal Tax Service informs within 10 working hours. days from the date of discovery;

- joint reconciliation.

Types of tax overpayment

Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated April 24, 2012 N 16551/11, Letter of the Federal Tax Service dated December 24, 2013 N SA-4-7/23263

- overpaid

- by the taxpayer himself: refund with % in case of violation of deadlines (clause 10 of article 78 of the Tax Code of the Russian Federation) . - excessively withheld

- accrued and reflected in the decision of the Federal Tax Service: return with % (clause 5 of Article 79 of the Tax Code of the Russian Federation).

What and for what period can be returned (offset)

- taxes, fees, insurance premiums, fines and penalties for them, except FSS NS and PZ

Refund (offset) of overpayments on funds

Distribution of taxes, fees, contributions across budgets

- Federal

VAT, Excise taxes, personal income tax, income tax, mineral extraction tax, water tax, fees for the use of wildlife..., state duty (Article 13 of the Tax Code of the Russian Federation) - Unified agricultural tax, simplified tax system, UTII (clause 7, article 12 of the Tax Code of the Russian Federation)

- insurance premiums (Article 18.1 of the Tax Code of the Russian Federation)

- corporate property tax, gambling tax, transport tax (Article 14 of the Tax Code of the Russian Federation)

- land tax, trade tax, property tax for individuals (Article 15 of the Tax Code of the Russian Federation)

What to do with “overpayment”

Return/credit

A right, not an obligation (clause 6 of Article 78 of the Tax Code of the Russian Federation, Letter of the Ministry of Finance of the Russian Federation dated 04/12/2018 N 03-02-07/1/24222 - in case of liquidation, return to the Organization, not to the participants).

Exceptions:

- amounts already distributed by the Pension Fund per person per person. accounting (clause 6.1, article 78 of the Tax Code of the Russian Federation);

- sanctions under currency legislation (Letter of the Federal Tax Service of the Russian Federation dated March 2, 2018 N GD-4-8/4131);

- debts of other persons (Letter of the Ministry of Finance of the Russian Federation dated June 18, 2018 N 03-02-07/1/41421).

Overpayment refund (offset) scheme

Depends on whether the taxpayer has arrears

(Clause 1, 1.1, 5, 6, 14 of Article 78 of the Tax Code of the Russian Federation).

Application methods

Options

(clauses 4, 6, article 78 of the Tax Code of the Russian Federation, clauses 2, 5, article 79 of the Tax Code of the Russian Federation):

- on paper (in person / valuable letter with a list of attachments);

- in electronic form via TKS with enhanced electronic signature;

- in the legal entity’s personal account on the Federal Tax Service website.

Attach

(clauses 10, 11, 14 of article 78 of the Tax Code of the Russian Federation):

- explanations of how the overpayment occurred;

- confirmation of the date of discovery of the overpayment;

- reminder of the accrual of interest on overcharged amounts;

- primary data (PP, reporting, scans, screenshots, correspondence...).

How to make an “official” screen

Letter of the Federal Tax Service of the Russian Federation dated March 31, 2016 N SA-4-7/5589

“...courts will accept screenshots as valid evidence if they contain certain data.”

“...a screenshot is a page on the Internet (a screenshot showing what the user sees on a monitor screen) confirming the placement of information subject to disclosure.”

Personal account of a legal entity on the Federal Tax Service website

https://lkul.nalog.ru/

Application deadlines

- excessive collection - 3 years from the date when it became known (clause 3, 9, article 79 of the Tax Code of the Russian Federation);

- overpayment - 3 years from the date of payment (clauses 7, 14, article 78 of the Tax Code of the Russian Federation);

- NEW

independent offset by the Federal Tax Service for the amount of overpaid tax - no more than 3 years from the date of payment (clause 5 of Article 78 of the Tax Code of the Russian Federation from August 30, 2018).

Decision on return (offset) / refusal

Return, offset, refusal

- 10 work days from the date of receipt of the application (clause 6 of article 6.1 of the Tax Code of the Russian Federation, clauses 4, 5, 6, 8, 14 of article 78 of the Tax Code of the Russian Federation);

- if offset against other taxes, then submit an application in advance (clause 4, clause 3, article 45 of the Tax Code of the Russian Federation, clause 3, article 75 of the Tax Code of the Russian Federation).

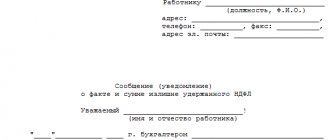

Notification of return (credit) / refusal

- with a message about return (offset), refusal

- 5 working days. days from the date of the decision (clause 6 of article 6.1 of the Tax Code of the Russian Federation, clauses 9, 14 of article 78 of the Tax Code of the Russian Federation). - for refund of funds

- 1 month from the date of receipt of the application (clause 6, 14 of article 78 of the Tax Code of the Russian Federation).

Is it possible to offset tax overpayments between budgets of different levels?

Yes, if the payments relate to the same type of taxes.

There are no restrictions in the Tax Code of the Russian Federation when offsetting overpayments of taxes between budgets of different levels - federal, regional and local (Letter of the Ministry of Finance of Russia dated April 26, 2011 N 03-02-07/1-141).

For example, income tax is credited to the federal and regional budgets, value added tax is credited to the federal budget (Article 50, paragraph 2 of Article 56 of the Budget Code of the Russian Federation). Since both taxes are federal, the overpayment of income tax can be offset against the VAT arrears. In this case, offset is also possible in that part of the overpayment that is credited to the regional budget.

Overpayment of income tax in one budget can be offset against payments for this tax in another budget (federal part against the regional part and vice versa).

Results

To offset overpaid tax amounts, fill out an application. After the inspectors review the application for offset of the amount of overpaid tax, they will make an appropriate decision and inform you about it. The forms of documents involved in the document flow of the offset procedure are approved by the regulations of the tax department.

Sources:

- Tax Code of the Russian Federation

- Order of the Federal Tax Service of Russia dated February 14, 2017 No. ММВ-7-8/ [email protected]

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

To what tax payments can an overpayment of tax be offset?

You can send overpayments of taxes (clauses 4, 5, Article 78 of the Tax Code of the Russian Federation):

- towards upcoming tax payments;

- to pay off debts on taxes, penalties, and fines.

It can be offset against any tax, regardless of whether it is federal, regional or local. It can also be offset against penalties and fines related to any type of tax (Clause 1, Article 78 of the Tax Code of the Russian Federation).

The exception is personal income tax. Its overpayment cannot be offset against future personal income tax payments. But you can apply such an overpayment towards future payments for other taxes. Basis - clause 1, 14 art. 78, paragraph 9 of Art. 226 of the Tax Code of the Russian Federation, Letter of the Federal Tax Service of Russia dated 02/06/2017 N ГД-4-8/ [email protected] (we believe that these clarifications can be used with the amendment that after the repeal of paragraph 2 of clause 1 of Article 78 of the Tax Code of the Russian Federation from 01.10. 2020 for offset it is not required that the type of offset taxes match).

What to do to get a refund

To offset and return the overpayment, you must inform the tax inspectorate about the decision. This must be done by submitting an application in the form approved by order of the Federal Tax Service of Russia dated February 14, 2017 No. ММВ-7-8/ [email protected]

Depending on whether there is arrears on other taxes and how much overpayment there is, the organization and individual entrepreneur can proceed as follows:

1. If the overpayment is greater than the arrears , then you can:

- immediately write an application for a refund of the overpayment. In this case, the tax office will independently pay off all existing arrears of taxes, penalties, fines, and return the balance to the current account,

- write an application for offset of the debt, and for the remaining amount submit an application for offset against future payments of any tax.

2. If the overpayment is less than the arrears , then, obviously, there is no need to ask for the overpayment to be returned to the current account. In this case, you need to write an application to offset the existing debt.

The tax authority will make a decision on offset within 10 working days:

- from the date of signing the act of reconciliation with the tax office (if such an act was signed)

- from the date of receipt of an application from the taxpayer for the offset (if such an application was submitted).

- from the moment the overpayment is discovered, if the taxpayer has not applied to the tax office with an application for a credit against a specific tax.

The tax authority must also make a decision to return the overpayment amount within 10 working days from the date of receipt of the application from the taxpayer or the date of signing the reconciliation report. Tax authorities are given another five working days to inform the taxpayer about the decision made and another month to transfer the money to the current account.

How to offset tax overpayments

To offset the overpayment against future payments, submit an application to the inspectorate in the approved form (clause 4 of article 78 of the Tax Code of the Russian Federation).

Application for offset of tax overpayment sample

We recommend that you check your data with the tax authority before submitting an application to offset the overpayment. To do this, you can request a certificate of the status of settlements with the budget or a reconciliation report. The fact is that if the inspection reveals discrepancies with the amounts that you indicated in the application, it will still offer to carry out a reconciliation first.

If the overpayment arose due to an error in the declaration, then first submit an updated declaration in which the error was corrected (clause 1 of Article 81 of the Tax Code of the Russian Federation). After that, submit an application for credit. The inspectorate will offset the overpayment to pay off arrears of taxes (penalties, fines) independently.

However, you can submit an application for offset in this case yourself (clause 5 of Article 78 of the Tax Code of the Russian Federation).

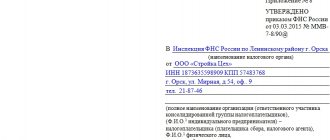

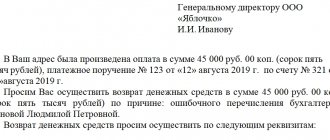

Tax refund application

If the organization has decided to return overpaid amounts for tax liabilities, then another application must be filled out. The application form for refund of overpayments is unified, KND - 1150058.

Let's look at how to fill out an application for a refund of overpaid tax, using the example of Clubtk.ru LLC: in December 2022, the limited liability company erroneously paid the organization's property tax in the amount of 1,723.00 rubles. The organization is exempt from paying property tax. The accountant drew up an application for a refund of the overpaid amount.

Within what period can the inspectorate itself offset the overpayment of taxes to pay off the arrears?

The inspection may carry out offsets within the time limits for forced collection of arrears, penalties, and fines. If these deadlines are missed, the tax authority does not have the right to independently offset the arrears (Determination of the Constitutional Court of the Russian Federation dated 02/08/2007 N 381-O-P, Resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation dated 07/30/2013 N 57 (clause 32), Presidium of the Supreme Arbitration Court of the Russian Federation dated 15.09. 2009 N 6544/09).

If the inspection has missed the deadline for the undisputed collection of arrears, penalties, fines, then it has the right to carry out such an offset only if there is a court decision on this (Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated December 9, 2008 N 8689/08).

How can an organization apply to offset tax overpayments?

You need to submit an application for offset of the overpayment to the inspectorate within a limited time. You can do this in one of the following ways (clauses 4, 5, Article 78 of the Tax Code of the Russian Federation):

- in paper form - in person (through a representative) or by mail;

- in electronic form - via TKS or through the taxpayer’s personal account.

Submit your application to the inspectorate at your place of registration. And if there are separate divisions, you can submit it both at the place of registration of the EP and at the place of registration of the organization. This follows from paragraph 7 of Art. 78, paragraph 1, art. 83 Tax Code of the Russian Federation.

How long does it take for the inspectorate to make a decision to offset tax overpayments?

The time frame for making a decision on offset depends on whether the inspection conducted a desk audit and whether violations were discovered during it.

If the inspection conducted a desk audit and found no violations, the period is 10 working days. They are not counted immediately after completion of the inspection, but after another 10 working days have elapsed from one of the following dates (clause 6 of article 6.1, clauses 4, 5, 8.1 of article 78 of the Tax Code of the Russian Federation):

- the date following the end of the inspection, if the inspection completed it within the prescribed period;

— the date when the inspection must be completed under clause 2 of Art. 88 of the Tax Code of the Russian Federation - if the inspection verified the declaration longer than the required period.

If the inspection conducted a desk audit and revealed violations

, the period is 10 working days from the date following the day the decision came into force based on the results of the desk audit (clause 6 of article 6.1, clauses 4, 5, 8.1 of article 78 of the Tax Code of the Russian Federation).

If a desk audit was not carried out

, the inspection must make a decision to offset the overpayment within 10 working days from the date of receipt of your application or signing of a joint reconciliation report, if such a reconciliation was carried out (clause 6 of article 6.1, clauses 4, 5 of article 78 of the Tax Code of the Russian Federation) . We recommend that you apply for a credit in advance - at least 10 business days before the upcoming tax payment deadline for which you plan to apply the overpayment.

The inspection must inform you about the decision made within five working days after its adoption (clauses 2, 6, article 6.1, clause 9, article 78 of the Tax Code of the Russian Federation). The inspectorate can deliver such a message to you or your representative personally against receipt, by TKS or in another way (Clause 9 of Article 78 of the Tax Code of the Russian Federation).

If the inspectorate itself offsets the overpayment

on account of tax arrears (penalties, fines), then such a decision must be made within 10 working days from the next day after (clause 2, 6, article 6.1, clause 5, article 78 of the Tax Code of the Russian Federation):

— detection of overpayment;

— signing a reconciliation report jointly with you, if one was carried out;

— entry into force of a court decision (for example, if the overpayment was confirmed by the court).

The inspector’s silence about the overpayment does not affect the three-year period for its return

According to the certificate on the status of settlements with the budget dated December 6, 2017, the entrepreneur had an overpayment of taxes in the amount of 434 thousand rubles.

By decisions of the tax authority dated December 15, 2017, the individual entrepreneur was denied a tax refund due to the expiration of the three-year period from the date of payment, provided for in clause 7 of Art. 78 Tax Code of the Russian Federation. The overpayment arose in connection with the submission by the entrepreneur of an updated VAT return for the second quarter of 2011, according to which the taxpayer adjusted the previously accrued tax amounts in the amount of 434 thousand rubles.

The court came to the conclusion that the applicant missed the three-year deadline for applying for a refund of the overpaid tax, since the applicant learned (should have known) about the excessive payment of tax in 2011, at the time of its transfer to the budget.

The norm of paragraph 3 of Art. 78 of the Tax Code of the Russian Federation on the obligation of the inspectorate to report each fact of excessive tax payment within 10 days from the date of its discovery does not apply in this case. The fact is that the taxpayer knew about the overpayment. This confirms the fact that he submitted an initial and updated declaration and voluntarily paid the tax.

Thus, failure to inform the taxpayer by the tax authorities during the three-year period for the return of the overpayment does not affect.

Ruling of the Supreme Court of the Russian Federation dated March 19, 2019 No. 304-ES19-1659

What to do if the inspection refused the test or carried it out late

You can appeal the refusal to offset to a higher tax authority, and then to the court (Article 137, clauses 1, 2 of Article 138 of the Tax Code of the Russian Federation).

As a general rule, the period for appeal is one year from the moment you learned or should have learned about a violation of your rights (Clause 2 of Article 139 of the Tax Code of the Russian Federation).

The period for going to court is three years from the day when you learned or should have learned about a violation of your right to offset (clause 79 of the Resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation dated July 30, 2013 N 57). If the inspection does not carry out the offset in a timely manner, then no interest is accrued on the offset amount. You can only appeal the inaction of the inspectorate in the manner indicated above.