Participants, including founders or shareholders, can provide financial assistance to their organization. When necessary, replenish working capital to prevent bankruptcy and cover losses. There are several ways, usually this is:

- loan;

- gratuitous transfer of property, including money, into the ownership of the organization;

- transfer of property for free use, that is, a loan.

If we are talking about an LLC, then its participant can provide assistance in the form of a contribution to property or an additional contribution to the authorized capital.

To quickly understand each registration option, understand the accounting features and restrictions associated with each type of financial assistance, take a look at the table.

Help in kind

The participant can provide financial assistance in non-monetary form. That is, transfer fixed assets, materials, goods, and intangible assets to the organization. The accounting procedure in this case depends on the type of property. For more information, see:

- How to register and record the receipt of fixed assets free of charge;

- How to record the receipt of materials in accounting;

- How to reflect the purchase of goods in accounting;

- How to reflect the acquisition (creation) of a trademark in accounting.

Help with money

If financial assistance from a participant is received in cash, then the accounting procedure depends on the period in which it was received:

- during the reporting year - for any purpose;

- at the end of the reporting year - to cover the loss generated in account 84 “Retained earnings (uncovered loss)”.

Include the money received from the participant during the year as other income. Make a note in your accounting:

Debit 50 (51) Credit 91-1

– reflects the gratuitous receipt of money from the participant.

Do not use Account 98-2 “Gratuitous receipts” when receiving money. It is intended to account for income from gratuitous receipts of non-monetary assets only. This conclusion can be made in the Instructions for the chart of accounts.

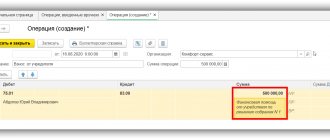

An example of how financial assistance provided by the founder in cash is reflected in accounting

In March of this year, the founder of Alpha LLC A.V. Lvov provided financial assistance to the organization in cash. The purpose of financial assistance is to replenish the organization’s working capital, amount – 500,000 rubles. The money arrived in the organization’s bank account on March 15.

An entry was made in Alpha's accounting records.

March 15th:

Debit 51 Credit 91-1 – 500,000 rub. – financial assistance was received from the founder.

Accounting for receiving financial assistance

According to the instructions for using the standard chart of accounts, passive account 98 (subaccount 2) is used to reflect information on the amounts of gratuitous receipts. In this case, the accounts of the property transferred into possession are debited.

As the allocated funds are used, the amounts are recognized as non-operating income, partially written off to account 91.1. This is necessary according to PBU: assets received free of charge as a result of charity are considered non-operating income and must be reflected in account 91. A decrease in the amount of assistance received occurs when:

- release into production of MPZ;

- calculation of depreciation charges;

- repayment of accounts payable;

- carrying out other operations using targeted financing.

Accounting data must fully reflect the sources of non-operating income and the conditions for their application.

Loss Coverage

If money is received from a participant to repay a loss generated at the end of the reporting year, do not use account 91.

As a rule, the decision of participants, including founders or shareholders, to provide financial assistance to cover losses is made after the end of the reporting year, but before the approval of the annual financial statements. Such a decision is recognized as an event after the reporting date. Financial assistance is immediately charged to account 84 “Retained earnings (uncovered loss).” In this case, no entries are made in the accounting records of the reporting period. This follows from paragraphs 3 and 10 of PBU 7/98.

To account for incoming funds, use account 75 “Settlements with founders”. It is worth opening a subaccount for it “Funds of participants aimed at repaying losses.”

The receipt of financial assistance to cover the loss generated at the end of the reporting year should be reflected in accounting entries.

1. On the date when the decision on financial assistance is documented by the minutes of the general meeting of participants, including shareholders, or by the decision of the sole founder:

Debit 75 subaccount “Funds of participants aimed at repaying losses” Credit 84

– a decision was made to repay the loss at the expense of the participants’ funds.

2. On the date of receipt of money:

Debit 50 (51) Credit 75 subaccount “Funds of participants aimed at repaying losses”

– funds were received from participants to cover losses generated at the end of the reporting year.

This procedure follows from the Instructions for the chart of accounts (account 75).

Tradition

The Tradition Charitable Foundation organizes assistance under the following programs:

- “Special Children” – helping children with central nervous system disorders.

- “The disease will not wait” is a program to help people with serious illnesses.

- “Life on the Palm” and “Good Deed” - support for hospitals and public institutions.

- “One step to life” – purchase of wheelchairs for people with spinal injuries.

- “Neighbors” – helping socially vulnerable families. These include the poor, those caught in unforeseen circumstances, and victims of fire. Construction materials are purchased for them, repairs, household appliances and other necessary things are paid for.

- “Good people” – providing assistance to the homeless.

- “People in Need” is a program designed to support people who have suffered from natural disasters or found themselves in emergency situations.

Basically, “Tradition” provides material assistance and purchases everything necessary for those in need and victims. The organization does not directly hand out funds to applicants. All applications received by the charitable foundation are checked and published on the Internet.

Replenishment of the reserve fund

Situation: how to reflect in accounting the receipt of gratuitous monetary assistance from a participant (founder, shareholder) to replenish the reserve fund (capital)?

The reserve fund can only be replenished from retained earnings. Therefore, first reflect financial assistance as part of other income. At the end of the year, after summing up financial activities, include these amounts in the reserve fund.

There is no other way to form a reserve fund using financial assistance. Therefore, first reflect the funds received from participants in account 91-1 as part of other income.

Turnovers in the debit of account 91-1 “Other income” will increase the organization’s net profit generated on account 99 “Profits and losses”.

At the end of the year, after summing up the results for account 84 “Retained earnings”, form a reserve fund from retained earnings.

In accounting, reflect all this with the following entries:

Debit 50 (51) Credit 91-1

– reflects the gratuitous receipt of money from the participant (founder, shareholder);

Debit 91-1 Credit 99

– profit is reflected at the end of the year;

Debit 99 Credit 84

– reflects net profit at the end of the year;

Debit 84 Credit 82

– contributions have been made to the reserve fund (capital) according to the standards approved by the charter.

This conclusion follows from the Instructions for the chart of accounts (accounts 84, 82).

If, after increasing the reserve capital (fund), its value exceeds the restrictions established in the organization’s charter, amend the charter.

All this follows from paragraph 7 of PBU 9/99, paragraph 1 of Article 35 and Article 12 of the Law of December 26, 1995 No. 208-FZ, paragraph 1 of Article 30, paragraph 4 of Article 12 of the Law of February 8, 1998 No. 14-FZ , Instructions for the chart of accounts (accounts 84, 99) and is confirmed in the letter of the Ministry of Finance of Russia dated August 23, 2002 No. 04-02-06/3/60.

How to write it down in an accounting report - such profit is not taken into account

Disputes among accountants continue to this day on this topic. Some say that gratuitous assistance should be counted as income.

Others deny this position. Where is the truth? To understand it, you need to separate the options when the founder’s help is a contribution to the property and when it is spent on any other purposes:

Contribution

According to the provisions of PBU, income is recognized as any increase in its economic benefits, both through the gratuitous receipt of intangible monetary assets, and through the repayment of obligations, leading to an increase in the total capital of the company, not including voluntary contributions of the participants and owners of the company .

This means that the founder’s monetary assistance is not considered income in accounting, but, according to Article 128 of the Civil Code of the Russian Federation, is the same property of the organization as a laptop transferred into its ownership, for example.

But any increase in the total property base of an enterprise cannot be considered gratuitous within the framework of accounting, since it affects the value expression of the shares of all participants in the company. Moreover, the nominal increase in the share of the participant who made the contribution is often less than the amount of the contribution.

Therefore, the assistance is completely transferred to the organization’s property accounts and credited to the additional capital accounts (account 83, in particular). Confirmation of this can be found in the letter of the Ministry of Finance No. 07-05-06/18 dated January 29, 2008.

When financial assistance is not taken into account when calculating income tax

In some cases, financial assistance does not need to be taken into account as income when calculating income tax. Such situations are named in the table below.

| Type of assistance received | Conditions under which you do not have to reflect income in tax accounting | Restrictions | Reasons |

| Property, including money. In addition to property and non-property rights | The participant, founder or shareholder who provides financial assistance owns more than 50 percent of the authorized capital of the recipient organization | The property or part thereof cannot be transferred to third parties during the year. Otherwise, its cost will have to be taken into account in income. The restriction does not apply to money | Clause 2 of Article 38, clause 8 of Article 250, subclause 11 of clause 1 of Article 251 of the Tax Code of the Russian Federation |

| The organization receiving financial assistance owns more than 50 percent of the authorized capital of the transferring organization. Moreover, on the date of transfer of property, the receiving organization must own this contribution by right of ownership | If the transferor is a foreign company included in the list of states and territories that provide preferential tax treatment, the value of the property received from it must be included in income regardless of the size of the share | ||

| Property and non-property rights, property itself, including money | Financial assistance was provided to increase the net assets of the recipient organization. The size of the shares in the authorized capital does not matter. Including when this is done with a simultaneous reduction or termination of the debt of the recipient organization to the participant, founder or shareholder | The purpose of financial assistance is directly indicated in the decision or provided for in the constituent documents of the recipient organization | Subclause 3.4 of clause 1 of Article 251 of the Tax Code of the Russian Federation |

If financial assistance received from a participant, including a founder or shareholder, does not increase the base for calculating income tax, a permanent difference arises in accounting, with which a permanent tax asset must be calculated (clause 7 of PBU 18/02).

Financial assistance to increase net assets is not taken into account in income. This rule also applies to situations where, at the request of participants, founders or shareholders, the company’s debt to them is reduced or terminated. For example, if a company has not fulfilled its obligations to a participant under a loan agreement, he can transfer the loan to increase net assets. Thus, he terminates the company’s obligations under the agreement (letter of the Federal Tax Service of Russia dated July 20, 2011 No. ED-4-3/11698).

At the same time, interest accrued on such a loan and written off through debt forgiveness is not recognized as property received free of charge in order to increase net assets. In fact, these funds are not transferred to the public. Therefore, the debtor includes them in non-operating income on the basis of paragraph 18 of Article 250 of the Tax Code of the Russian Federation. Such clarifications are given in the letter of the Federal Tax Service of Russia dated May 2, 2012 No. ED-3-3/1581.

An example of reflection in accounting and taxation of fixed assets received free of charge from the founders to increase net assets. The organization applies a general taxation system

Based on the results of 2015, Torgovaya LLC revealed that the amount of net assets is less than the authorized capital.

In March 2016, one of the participants, A.S. Glebova - decided to make a property contribution to the society in order to increase net assets - a Sony VAIO VPC-L22Z1R/B computer worth 78,000 rubles. In the same month, at the general meeting of participants, this decision was approved and enshrined in the minutes. The computer was handed over to Glebova to the company and put into operation the same month.

In March, the following entries were made in the accounting records of Hermes:

Debit 08 Credit 83 subaccount “Glebova’s contribution to increasing net assets” – 78,000 rubles. – fixed assets received from Glebova to increase net assets were taken into account;

Debit 01 subaccount “Fixed asset in operation” Credit 08 – 78,000 rub. – the fixed asset was accepted for accounting and put into operation.

When calculating income tax, the cost of a computer received free of charge is not taken into account (subclause 3.4, clause 1, article 251 of the Tax Code of the Russian Federation).

Situation: is it possible to take into account expenses paid with financial assistance from the founder when calculating income tax? The founder's share in the authorized capital exceeds 50 percent.

Yes, you can.

After the money received free of charge from the founder is capitalized, it becomes the property of the organization. Therefore, they spend them as their own funds. Consequently, costs paid with these funds can be taken into account when calculating income tax. Provided, of course, that the costs are economically justified and documented (clause 1 of Article 252 of the Tax Code of the Russian Federation).

A similar point of view is reflected in letters of the Ministry of Finance of Russia dated March 20, 2012 No. 03-03-06/1/142, dated June 29, 2009 No. 03-03-06/1/431, dated January 21, 2009 No. 03 -03-06/1/27 and confirmed by arbitration practice (see, for example, decisions of the FAS of the North-Western District dated April 12, 2007 No. A56-13199/2006, Volga-Vyatka District dated August 28, 2006 No. A29- 13543/2005a).

An example of how expenses paid from financial financial assistance from the founder are reflected in accounting and taxation. The founder's share in the authorized capital of the organization is 55 percent

In February, the founder of Torgovaya LLC A.V. Lvov provided the organization with free financial assistance in cash. The money was provided to replenish our own working capital. The amount of assistance is 150,000 rubles. In the same month, the money received was used to purchase materials. The cost of purchased materials is 150,000 rubles. (including VAT – RUB 22,881). In March, the materials were released into production.

The organization uses the accrual method. Income tax is paid monthly.

Postings have been made in the organization's accounting.

In February:

Debit 51 Credit 91-1 – 150,000 rubles. – received funds from the founder;

Debit 68 subaccount “Calculations for income tax” Credit 99 – 30,000 rubles. (RUB 150,000 × 20%) – a permanent tax asset is reflected;

Debit 60 Credit 51 – 150,000 rub. – funds were transferred to the materials supplier;

Debit 10 Credit 60 – 127,119 rub. – materials are capitalized;

Debit 19 Credit 60 – 22,881 rub. – input VAT is reflected;

Debit 68 subaccount “Calculations for VAT” Credit 19 – 22,881 rub. – accepted for deduction of input VAT.

In March:

Debit 20 Credit 10 – 127,119 rub. – materials are written off for production.

When calculating income tax in February, the Hermes accountant did not include funds received from the founder as income. When calculating income tax in March, the cost of materials written off for production was taken into account as expenses.

When and how financial assistance should be included in income when calculating income tax

When none of the conditions for exemption from taxation of the received financial assistance are met, take it into account as part of non-operating income (clause 8 of Article 250 of the Tax Code of the Russian Federation).

Recognize income:

- on the day the money is received in the current account or at the cash desk;

- on the date of receipt of the property (for example, execution of the transfer and acceptance certificate).

These rules apply both to the accrual method and to the cash method (subclauses 1 and 2, clause 4, article 271, clause 2, article 273 of the Tax Code of the Russian Federation).

If financial assistance received from a participant (founder, shareholder) increases the base for calculating income tax, but is not reflected in the income in accounting, a permanent difference is formed, with which a permanent tax liability must be calculated. This follows from the provisions of paragraphs 4 and 7 of PBU 18/02. For example, such a situation may arise when receiving money to pay off a loss formed at the end of the reporting year, or when receiving property for free use.

An example of reflection in accounting and taxation of funds received free of charge from the founders to pay off losses at the end of the reporting year. The organization applies a general taxation system

Based on the results of 2015, Torgovaya LLC received a loss of 1,000,000 rubles. The founders of Hermes are A.V. Lvov (share in the authorized capital of Hermes is 51%) and A.S. Glebova (share – 49%).

In March 2016 (before the annual financial statements were approved), the founders decided to cover the resulting loss from their own funds in the following proportions:

- Lviv - in the amount of 510,000 rubles;

- Glebova - in the amount of 490,000 rubles.

In the same month, money from the founders arrived in the Hermes bank account.

In March 2016, the following entries were made in the accounting records of Hermes:

Debit 75 subaccount “Funds from Lvov aimed at repaying the loss” Credit 84 – 510,000 rubles. – a decision was made to repay part of the loss to Lvov;

Debit 75 subaccount “Glebova’s funds aimed at repaying the loss” Credit 84 – 490,000 rubles. – a decision was made to repay part of Glebova’s loss;

Debit 51 Credit 75 subaccount “Funds from Lvov aimed at repaying the loss” – 510,000 rubles. – money was received from Lvov to repay the loss;

Debit 51 Credit 75 subaccount “Glebova’s funds aimed at repaying the loss” - 490,000 rubles. - money was received from Glebova to repay the loss.

In accounting, when receiving funds from the founders to repay a loss, income does not arise. When calculating income tax, income includes funds received from Glebova (since the founder’s share is less than 50%). The result is a permanent difference and a permanent tax liability:

Debit 99 subaccount “Continuous tax liabilities” Credit 68 subaccount “Calculations for income tax” - 98,000 rubles. (RUB 490,000 × 20%) – a permanent tax liability is reflected.

Situation: is it necessary to include gratuitous assistance received from the founding commercial organization in the calculation of income tax? The amount of assistance provided exceeds RUB 3,000.

Yes need. But only if the conditions are not met that allow financial assistance not to be taken into account in income.

The fact is that, regardless of the amount of gratuitous assistance received from the founder, it does not need to be taken into account in income only in strictly defined situations. This follows from the provisions of paragraph 8 of Article 250, subparagraphs 11 and 3.4 of paragraph 1 of Article 251 of the Tax Code of the Russian Federation.

In relation to gratuitous assistance, the amount of which exceeds 3,000 rubles, the possibility of applying this procedure is confirmed by arbitration practice (see, for example, decisions of the Federal Antimonopoly Service of the North-Western District dated December 23, 2005 No. A56-4986/2005, Volga District dated December 6, 2007 No. A65-5602/2007-SA1-7).

Attention: in a situation where gratuitous assistance is provided by the founding organization in the amount of more than 3,000 rubles, there is a risk that the recipient may be forced to take the assistance into account in income when calculating income tax.

Thus, according to Article 575 of the Civil Code of the Russian Federation, a gift between commercial organizations in the amount of more than 3,000 rubles. forbidden. And based on the provisions of the Tax Code, it follows that such transactions are allowed. The concept of property transferred or received free of charge for the purposes of calculating income tax is defined in paragraph 2 of Article 248 of the Tax Code of the Russian Federation. However, no cost restrictions have been established in relation to this property.

In a number of cases, it was proven in the courts that when calculating income tax, amounts over 3,000 rubles. still needs to be taken into account in income. Since assistance from one organization to another, in order to be exempt from taxation, must fulfill not only the conditions defined in the Tax Code, but also those provided for in Article 575 of the Civil Code of the Russian Federation. For example, resolutions of the Federal Antimonopoly Service of the Moscow District dated December 5, 2005 No. KA-A40/11321-05, dated June 30, 2005 No. KA-A40/3222-05.

Therefore, it is safer to formalize the funding received from the founder as an interest-free loan agreement or (if we are talking about an LLC) as a contribution to property.

Financial assistance agreement between legal entities: sample

It is worth mentioning separately about the agreement when assistance is provided by one legal entity to another. In this case, a gift agreement cannot be made - it may be considered void.

This follows from the provisions of Article 575 of the Civil Code of the Russian Federation, which prohibits gift agreements between legal entities if the subject of the agreement (including funds) is valued at more than 3,000 rubles.

In this case, you can use the following methods:

- Conclude a free financing agreement.

- Conclude an agreement on an interest-free loan, and then not claim it and write off overdue payments (Article 415 of the Civil Code of the Russian Federation). Borrowed funds are not taxed, as are interest savings, but the forgiven loan amount, which forms non-operating income for the borrower, is subject to taxation. A tax base is not formed when funds are received from a founder who owns at least 50% of the borrower's authorized capital.

- Contribute funds to increase the authorized capital. In this case, the organization that contributed the money must increase its share in the authorized capital.

The founder has the right to provide financial assistance to his company. The law does not establish a list of purposes for which this money can be spent. In accordance with the law, funds received must be documented. If the founder who contributed the assistance is an individual, then a gift agreement can be concluded with him. In cases where assistance is provided by another organization, it cannot be formalized by donation. In some cases, the amount of money contributed free of charge by the founder is not taxed.

VAT

When calculating VAT, do not take into account funds received from a participant, including a founder or shareholder, as gratuitous assistance. This is explained by the fact that the receipt of money is subject to VAT only if it is associated with payments for goods, works or services sold (subclause 2, clause 1, article 162 of the Tax Code of the Russian Federation).

Providing gratuitous financial assistance in cash is not considered a sale. A similar point of view is reflected in the letter of the Ministry of Finance of Russia dated June 9, 2009 No. 03-03-06/1/380.

Situation: is it possible to deduct VAT on goods, works or services that were purchased using funds received free of charge from a participant (founder, shareholder)?

Yes, you can.

The conditions under which an organization has the right to deduct input VAT are defined in Articles 171 and 172 of the Tax Code of the Russian Federation. The buyer’s right to deduct VAT does not depend on the sources from which goods, works or services were purchased. Therefore, in the situation under consideration, input VAT can be deducted on a general basis.

A similar point of view is reflected in letters of the Ministry of Finance of Russia dated June 29, 2009 No. 03-03-06/1/431, dated June 6, 2007 No. 03-07-11/152 and confirmed by arbitration practice (see, for example, resolutions FAS Volga-Vyatka District dated August 28, 2006 No. A29-13543/2005a, dated November 17, 2005 No. A29-933/2005a, Moscow District dated March 12, 2008 No. KA-A40/1240-08).

Types of gratuitous assistance

Cash is the main way to provide financial support to an enterprise. They can be transferred from other legal entities and individuals, the state or founders for certain purposes.

Free financial assistance can be provided not only in monetary terms, but also through the transfer of property in the form of fixed assets or intangible assets. For example, the ownership of an enterprise can be transferred to:

- property rights;

- work or services without payment;

- intellectual property;

- securities.

Timely financial assistance on a free basis can bring an enterprise out of a difficult situation and even avoid bankruptcy.

simplified tax system

When determining simplified income, the same income is not taken into account as when calculating income tax. This means that financial assistance received from a dependent founder or someone who owns more than 50 percent of the authorized capital of the recipient is also not taken into account when calculating the single tax. As well as assistance to increase net assets. This procedure is established by Article 346.15, paragraph 8 of Article 250, subparagraphs 3.4 and 11 of paragraph 1 of Article 251 of the Tax Code of the Russian Federation and letters of the Ministry of Finance of Russia dated April 18, 2011 No. 03-03-06/1/243, dated June 9, 2009 No. 03-03-06/1/380. Although the above letters are devoted to the procedure for accounting for financial assistance when calculating income tax, their provisions can also be extended to the calculation of a single tax under simplification.

If the specified conditions are not met, then assistance from a participant, including a founder or shareholder, should be taken into account as part of non-operating income (Article 346.15 and Clause 8 of Article 250 of the Tax Code of the Russian Federation).

Recognize income:

- on the day the money is received in the current account or at the cash desk;

- on the date of receipt of the property (for example, execution of the transfer and acceptance certificate).

This follows from the provisions of paragraph 1 of Article 346.17 of the Tax Code of the Russian Federation.

How to apply for financial assistance from the founder

The Federal Law “On Accounting” dated December 6, 2011 No. 402-FZ requires that all receipts to the organization’s current account and cash desk, including gratuitous assistance, be documented.

The most common method of gratuitous assistance is the conclusion of a gift agreement or gratuitous financial assistance between the one who contributes money and the one who receives it.

Also, the founder can use funds to increase the authorized capital, but in this case, his share must be increased (naturally, except in the case when the company has one founder), and the assistance can no longer be considered gratuitous. In this case, registration occurs in the following way:

- An application is drawn up indicating the amount and conditions for its contribution to the authorized capital.

- Other owners express their consent and decide to make amendments to the company's charter.

- All changes (re-registration of shares) must be made within 6 months after the decision is made.

In any case, before providing assistance, the founder must agree on this at a general meeting (or make a decision individually, if there is only one founder).

OSNO and UTII

If financial assistance is received and the conditions for its exemption from taxation are not met, then when calculating income tax, it must be taken into account in non-operating income.

The current tax legislation does not contain a mechanism for distributing non-operating income between different types of activities. If you cannot determine whether non-operating income belongs to a particular type of activity, then its entire amount should be included in the tax base for income tax and tax should be charged at a rate of 20 percent. This position is adhered to by the Russian Ministry of Finance in letter dated March 15, 2005 No. 03-03-01-04/1/116.

Tax accounting of gratuitous assistance

Providing financial support to other legal entities is regulated not only by accounting standards, but also by the instructions of the Tax Code of the Russian Federation. The main tax payments levied on amounts of property assistance are VAT and income tax.

Legislation in force in 2016 requires enterprises that provide gratuitous financial assistance to allocate funds from their net profits. According to the Tax Code of the Russian Federation, expenses associated with charity and targeted contributions are not included in the calculation of the taxable base.